Download to read offline

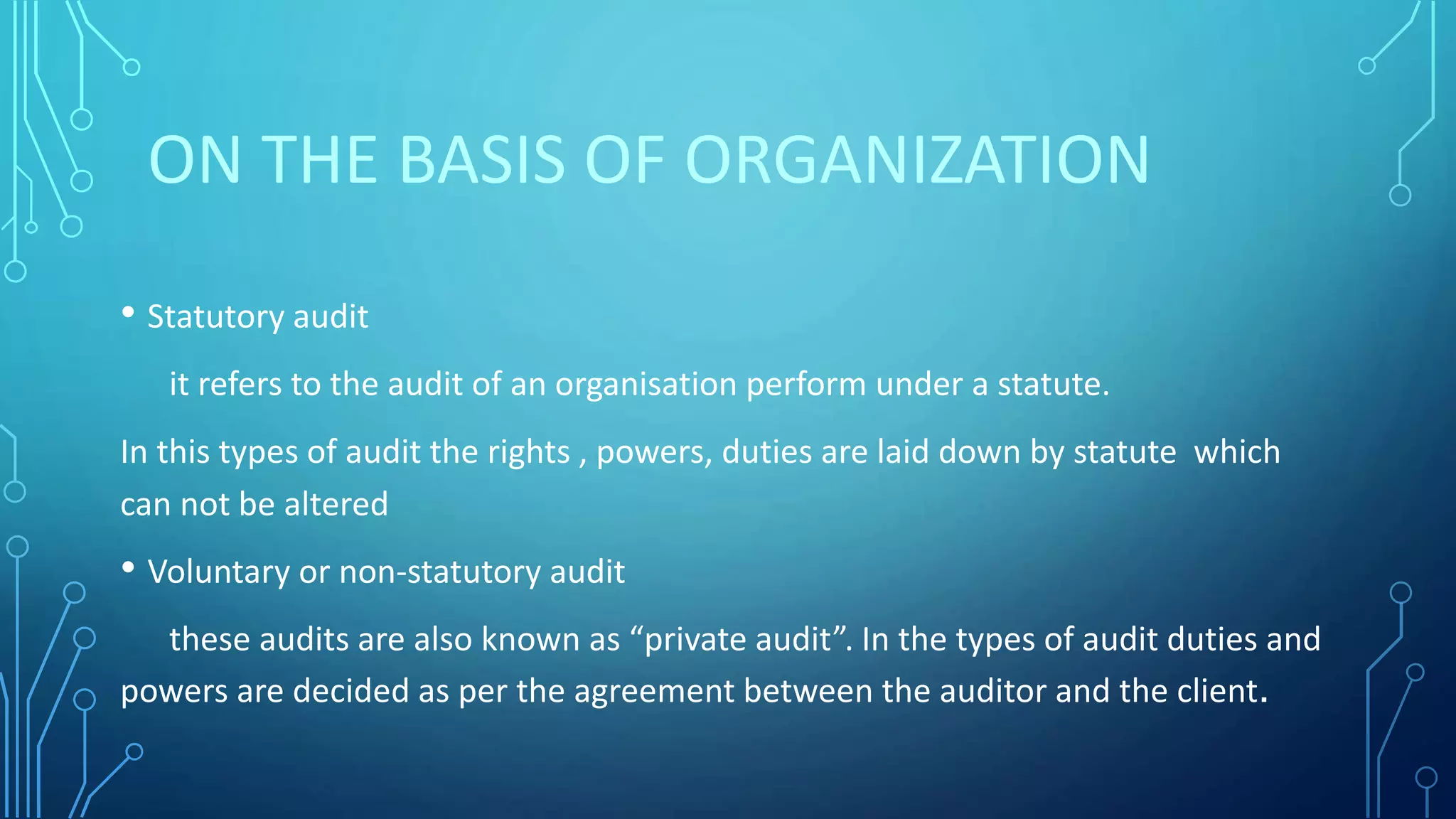

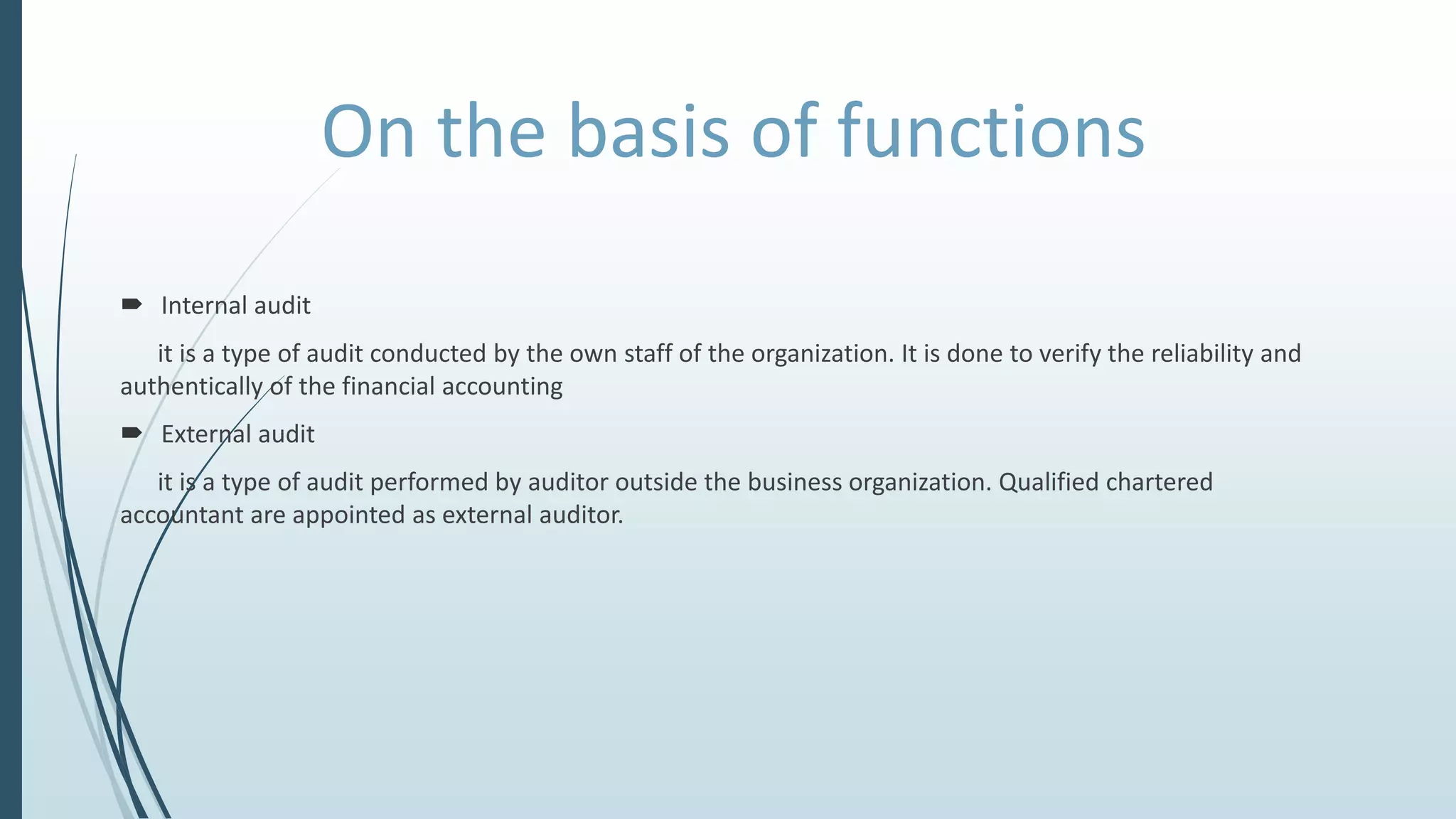

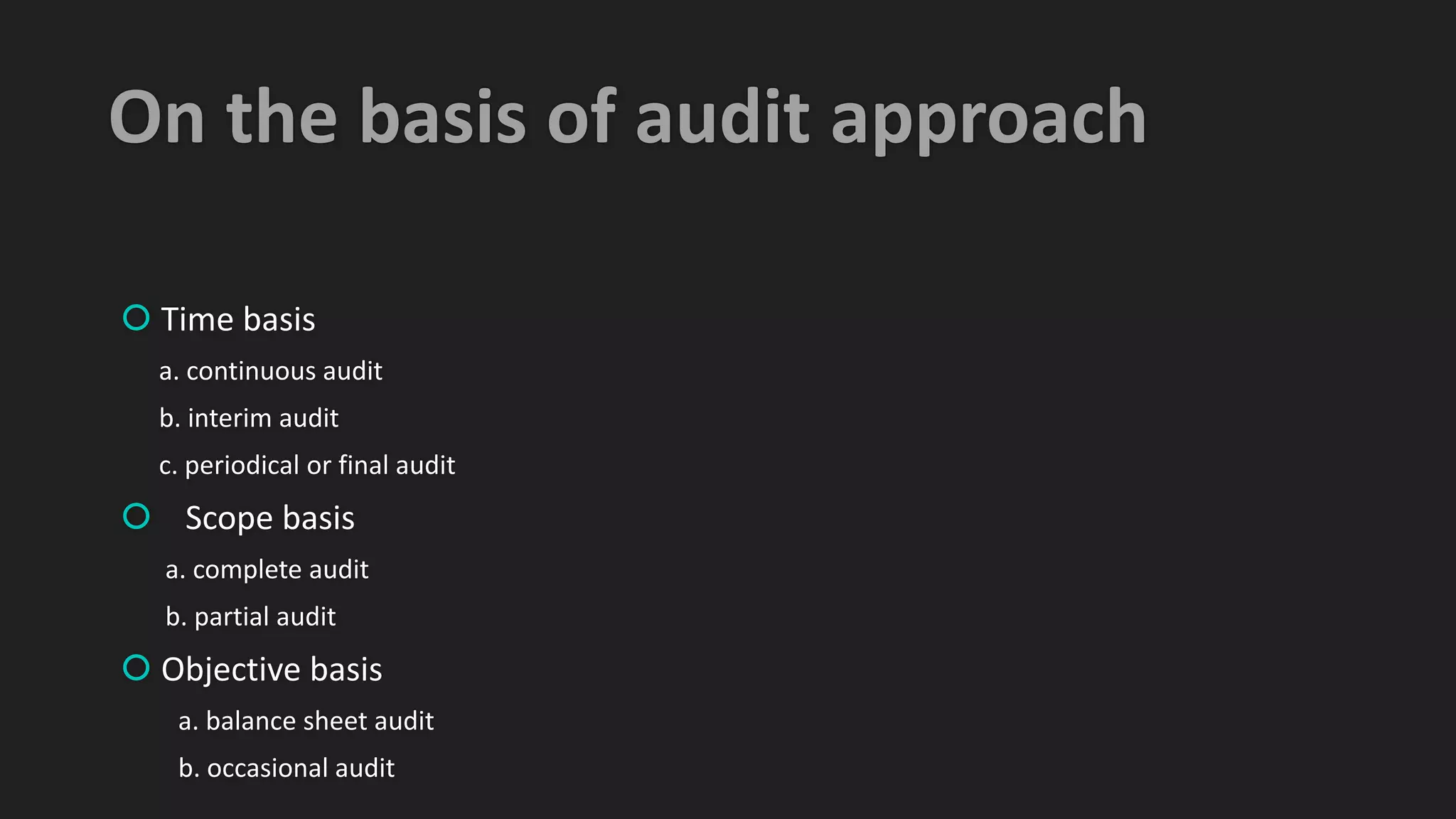

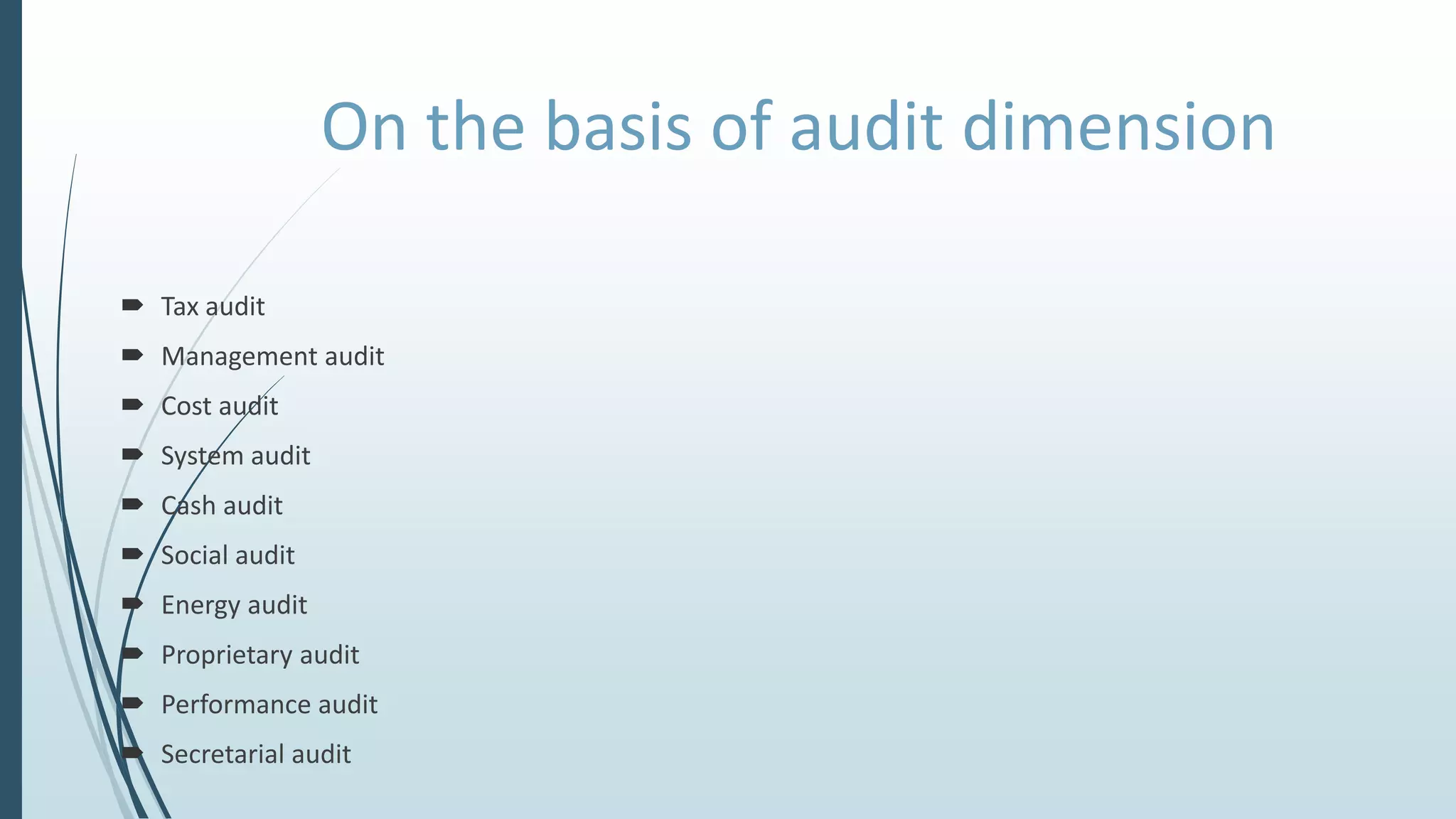

The document discusses various types of auditing, emphasizing the importance of ensuring proper maintenance of accounts as required by law. It categorizes audits based on organization (statutory and voluntary), functions (internal and external), approach (time, scope, and objective), and dimensions (tax, management, cost, etc.). Each type of audit has specific characteristics and objectives tailored to the needs of the organization or the requirements set forth by law.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)