Tutorial 5 partnership

•Download as DOCX, PDF•

0 likes•2,601 views

The document contains two questions regarding the dissolution of partnerships. Question 1 involves the dissolution of a partnership between Aminah, Badariah, and Dahlia. Upon dissolution, various partnership assets were sold or transferred to the partners. Dahlia was insolvent and unable to fully pay her capital account deficiency. Question 2 involves the dissolution of a partnership between Bedin, Ceyla, and Deris. Upon dissolution, partnership assets were sold or transferred to the partners. Deris was unable to fully pay his capital account deficiency based on the Garner vs Murray rule for distributing deficiencies.

More Related Content

What's hot

What's hot (20)

Viewers also liked

Similar to Tutorial 5 partnership

Similar to Tutorial 5 partnership (20)

More from kim rae KI

Recently uploaded

Recently uploaded (20)

Tutorial 5 partnership

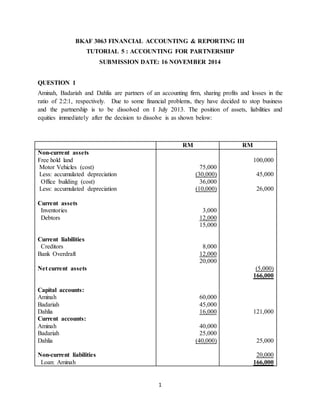

- 1. 1 BKAF 3063 FINANCIAL ACCOUNTING & REPORTING III TUTORIAL 5 : ACCOUNTING FOR PARTNERSHIP SUBMISSION DATE: 16 NOVEMBER 2014 QUESTION 1 Aminah, Badariah and Dahlia are partners of an accounting firm, sharing profits and losses in the ratio of 2:2:1, respectively. Due to some financial problems, they have decided to stop business and the partnership is to be dissolved on I July 2013. The position of assets, liabilities and equities immediately after the decision to dissolve is as shown below: RM RM Non-current assets Free hold land Motor Vehicles (cost) Less: accumulated depreciation Office building (cost) Less: accumulated depreciation Current assets Inventories Debtors Current liabilities Creditors Bank Overdraft Net current assets Capital accounts: Aminah Badariah Dahlia Current accounts: Aminah Badariah Dahlia Non-current liabilities Loan: Aminah 75,000 (30,000) 36,000 (10,000) 3,000 12,000 15,000 8,000 12,000 20,000 60,000 45,000 16,000 40,000 25,000 (40,000) 100,000 45,000 26,000 (5,000) 166,000 121,000 25,000 20,000 166,000

- 2. 2 Upon dissolution, the following took place: (i) Land was sold for RM160,000 (market value). Aminah took over the office building for RM18,000. (ii) The partnership owned two cars, one car was taken over by Aminah at RM25,000 (net book value RM30,000) and the other one was sold at RM15,000. Badariah took over the stock in hand at a discount of 10%. (iii) All debtors settled their debts except for RM2,000 which the partners considered as bad debts. (iv) They paid RM500 in legal fees arising from the dissolution. (v) The creditors agreed to accept RM7,600 as full payment for the amount due to them and the loan from Aminah was fully settled. (vi) All receipts and payments were made through the bank account and all the partners settled their accounts except for Dahlia who was declared insolvent. She only managed to pay RM1,000 and the deficiency in her capital account was borne by the other solvent partners. REQUIRED: Prepare the following: (a) Realisation account. (b) Bank account (c) Partners’ capital accounts.

- 3. 3 QUESTION 2 Bedin, Ceyla and Deris have been in a partnership for a number of years, sharing profits in the ratio of 5:3:2, respectively. The statement of financial position of the business as at 31 December 2013 is as follows: Statement of Financial Position As at 31 December 2013 RM RM ASSETS Non-Current Assets Premises 80,000 Equipment 50,000 Vehicles 30,000 160,000 Current Assets Inventories 40,000 Debtors 50,000 Bank 112,000 202,000 TOTAL ASSETS 362,000 LIABILITIES & OWNERS EQUITY Non-Current Liabilities Loan from Bedin 8,000 Loan from Finance Company 20,000 28,000 Current Liabilities Creditors 42,000 Bank Overdraft 32,000 74,000 Owners Equity Capital Accounts Bedin 160,000 Ceyla 60,000 Deris 20,000 240,000 Current Accounts Bedin 10,000 Ceyla 4,000 Deris 6,000 20,000 TOTAL LIABILITIES & OWNERS EQUITY 362,000

- 4. 4 On 1 January 2014, the partnership was dissolved due to a disagreement between the partners. Upon dissolution, the following transactions took place: 1. Premises were sold for RM115,000. The proceeds were then used to settle the bank overdraft. Equipment was realised at a loss of RM10,000. 2. Bedin agreed to take over the vehicles at 20% below book value. The loan from Bedin to the partnership was used as part of the settlement for the vehicles and the balance was paid by cheque. 3. Deris took over the inventories at a discount of 10%. 4. All debtors paid their debts in full except for an amount of RM1,500 which was unrecoverable and was therefore written off as bad debt. 5. The amounts owing to the creditors were paid in full at a discount of RM2,000. 6. Dissolution expenses amounting to RM1,500 were fully paid. 7. All payments and receipts were made through the bank account. 8. Deris had a debit balance in his capital account but only managed to pay RM4,400 to the partnership business. The deficiency is to be borne between Bedin and Ceyla based on the Garner vs. Murray rule. REQUIRED: (a) Prepare the realisation account to close the books of the partnership. (b) Prepare the bank account to close the books of the partnership. (c) Prepare the partners’ capital account to close the books of the partnership.