Tutorial 5 answer

•Download as DOCX, PDF•

1 like•2,390 views

This document contains solutions to accounting problems involving the dissolution of partnerships. Question 1 involves calculating partners' capital balances after the realization of partnership assets and distribution of profits. Question 2 involves accounting for the dissolution of a partnership between three partners, including recording the realization of assets and distribution of profits and capital balances to partners.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Similar to Tutorial 5 answer

Similar to Tutorial 5 answer (20)

More from kim rae KI

Recently uploaded

Recently uploaded (20)

Tutorial 5 answer

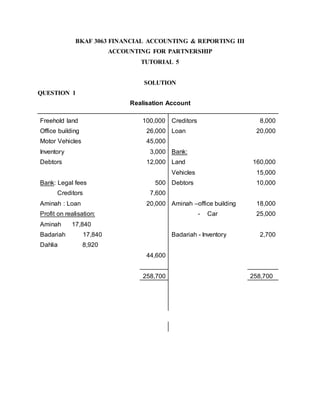

- 1. BKAF 3063 FINANCIAL ACCOUNTING & REPORTING III ACCOUNTING FOR PARTNERSHIP TUTORIAL 5 SOLUTION QUESTION 1 Realisation Account Freehold land 100,000 Creditors 8,000 Office building Motor Vehicles 26,000 45,000 Loan 20,000 Inventory Debtors 3,000 12,000 Bank: Land Vehicles 160,000 15,000 Bank: Legal fees Creditors 500 7,600 Debtors 10,000 Aminah : Loan 20,000 Aminah –office building 18,000 Profit on realisation: Aminah 17,840 - Car 25,000 Badariah 17,840 Badariah - Inventory 2,700 Dahlia 8,920 44,600 258,700 258,700

- 2. Bank Account Land Vehicle Debtors Capital: Dahlia 160,000 15,000 10,000 1,000 Balance Creditors Realisation: Legal fees Capital: Aminah Badariah 12,000 7,600 500 86,794 79,106 186,000 186,000 Account Capital Aminah Badariah Dahlia Aminah Badariah Dahlia Currentac 40,000 Balance b/d 60,000 45,000 16,000 Currentac 40,000 25,000 Realisation: Realisation: Build.taken 18,000 Loan 20,000 Car taken 25,000 Profit 17,840 17,840 8,920 Inv.Taken 2,700 Dahlia 8,046 6,034 Bank 1,000 Bank 86,794 79,106 Aminah 8,046 Badariah 6,034 137,840 87,840 40,000 137,840 87,840 40,000 Calculation: Dahliacapital - Dr balance 40,000 Cr Balance 24,920 (16,000 = 8,920) 15,080 Pay (1,000) Balance 14,080 Aminah: 60,000/(60,000 + 45,000) x 14,080 = 8,046 Badariah: 45,000 / (60,000 + 45,000) x 14,080 = 6,034

- 3. QUESTION 2 (a) Realisation Account RM RM Premises 80,000 Loan: Bedin 8,000 Equipment 50,000 Finance Co. 20,000 Vehicles 30,000 Creditors 42,000 Inventories 40,000 Bank o/draft 32,000 Debtors 50,000 Bank: Bank: Premises 115,000 Creditors [42,000 - 2,000] 40,000 Equipment [50,000 – 10,000] 40,000 Dissolution expenses 1,500 Debtors [50,000 – 1,500] 48,500 Bank o/draft 32,000 Bedin: Vehicles [80% x 30,000]] 24,000 Finance Co. 20,000 Deris: Invent. [90% x 40,000] 36,000 Loan: Bedin 8,000 Profit on Realisation: Bedin [0.5x14,000] 7,000 Ceyla[0.3x14,000] 4,200 Deris[0.2 x 14,000] 2,800 14,000 365,500 365,500 (b) Bank Account RM RM Balance b/d 112,000 Creditors 40,000 Realisaton: Realisaton: Premises 115,000 Bank o/draft 32,000 Equipment [50,000 – 10,000] 40,000 Dissolution expenses 1,500 Debtors [50,000 – 1,500] 48,500 Loan: Finance Co. 20,000 Capital: Bedin 16,000 Capital: Bedin 174,964 Deris 4,400 Ceyla 67,436 335,900 335,900

- 4. (c) Capital Account Bedin Ceyla Deris Bedin Ceyla Deris RM RM RM RM RM RM Realisation: Balance b/d 160,000 60,000 20,000 Inventory Taken Over 36,000/ Current a/c 10,000 4,000 6,000 Vehicles Taken Over 24,000 Realisation: Deris 2,036 764 Profit 7,000 4,200 2,800 Bank 174,964 67,436 Loan 8,000 Bank 16,000 4,400 Bedin 2,036* Ceyla 764** 201,000 68,200 36,000 201,000 68,200 36,000 * Amount paid by Bedin: Deris’s capital a/c balance is a debit = 36,000 – [20,000 + 6,000 + 2,800] = 7,200 But Deris could only pay the business (4,400) So Bedin & Ceyla would have to pay the balance of 2,800 as follows: Bedin: 2,800 x 160,000/[160,000 + 60,000] = 2,036 Ceyla: 2,800 x 60,000/[160,000 + 60,000] = 764**