Downloaded 75 times

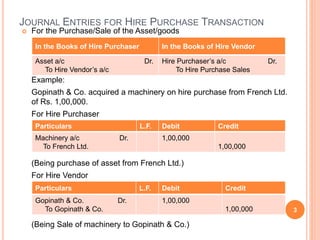

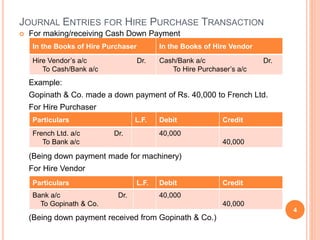

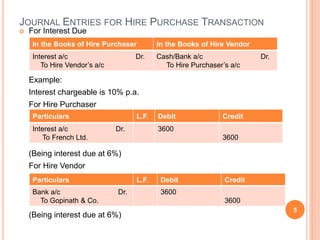

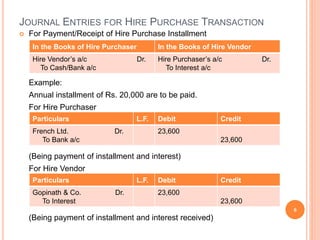

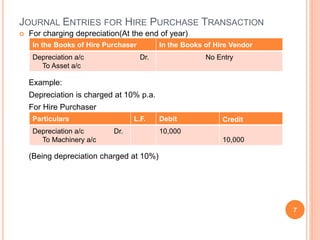

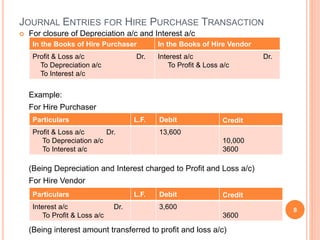

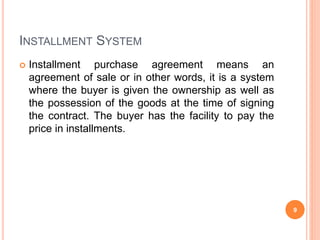

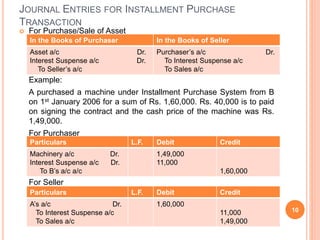

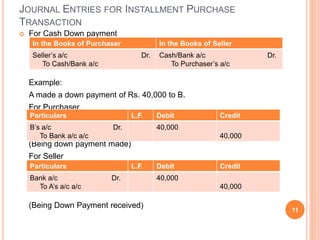

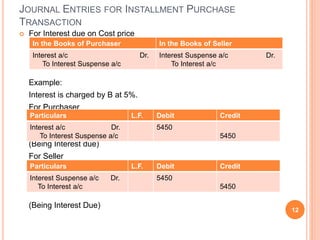

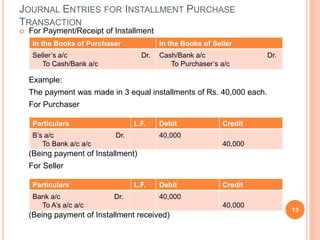

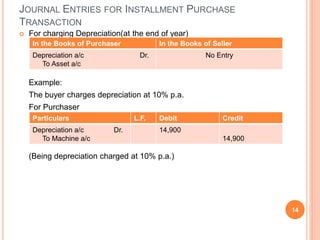

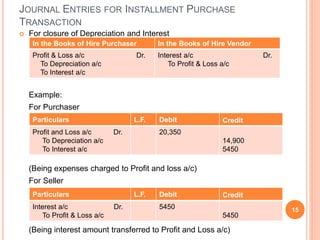

This document discusses accounting for hire purchase and installment purchase transactions. It provides journal entries for the purchase of an asset under hire purchase, including entries for down payment, interest due, installment payments, depreciation, and closing entries. It then discusses installment purchase agreements and provides similar journal entries for purchasing an asset under an installment system, including entries for the purchase price, down payment, interest due, installment payments, depreciation, and closing entries.