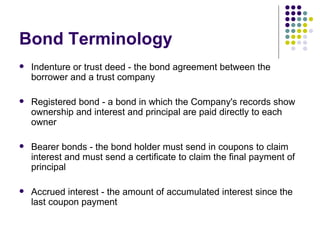

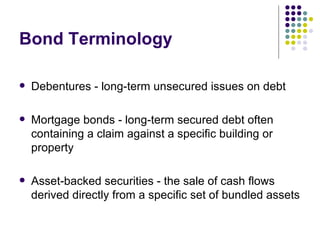

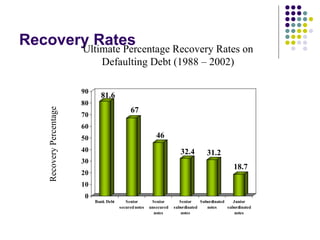

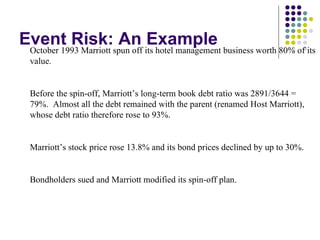

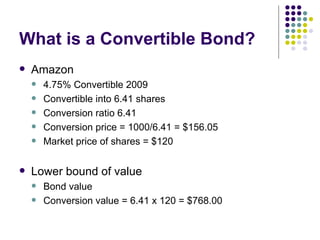

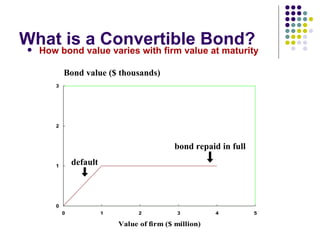

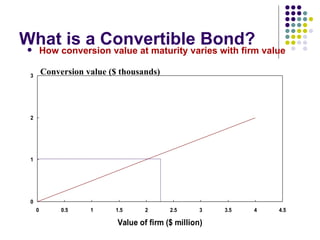

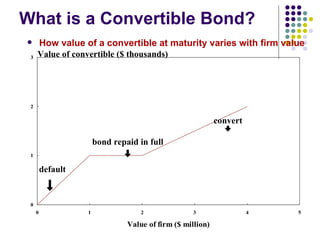

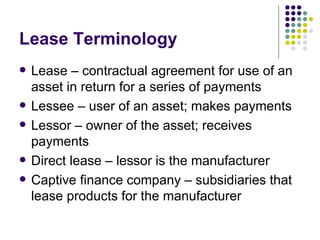

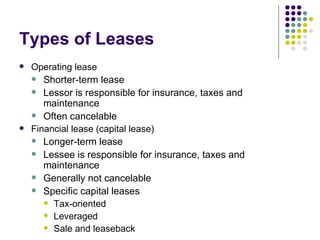

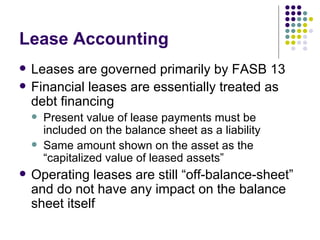

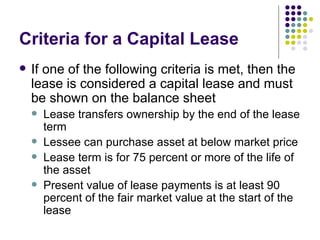

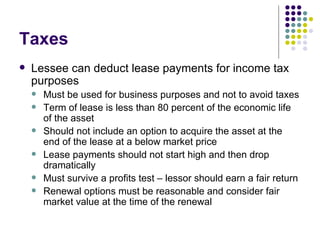

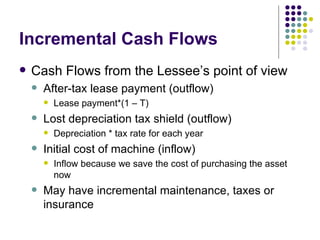

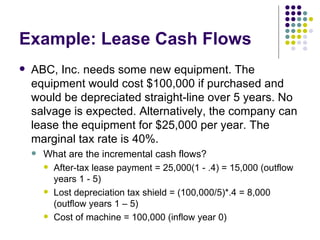

The document discusses various topics related to business borrowing and leasing, including different types of bonds, bond terminology, lease types and accounting, tax treatment of leases, and reasons for leasing versus buying. It provides information on domestic and foreign bonds, convertible bonds, bond covenants, and bond innovations. Key lease concepts covered include the distinction between lessees and lessors, operating versus capital/financial leases, and incremental cash flows from leasing. Reasons for leasing include potential tax benefits and avoiding restrictive covenants, while dubious reasons include balance sheet manipulation.