Downloaded 45 times

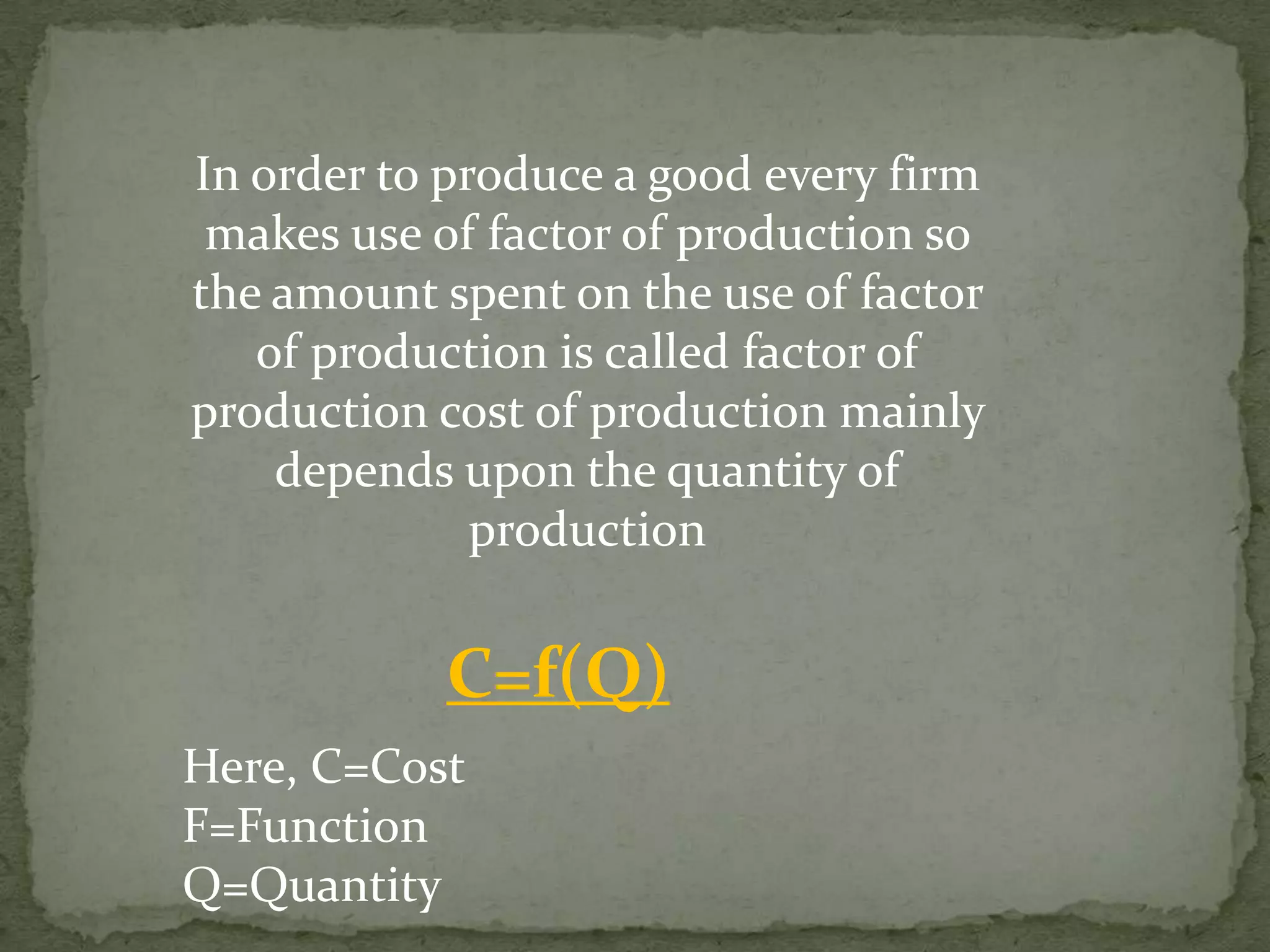

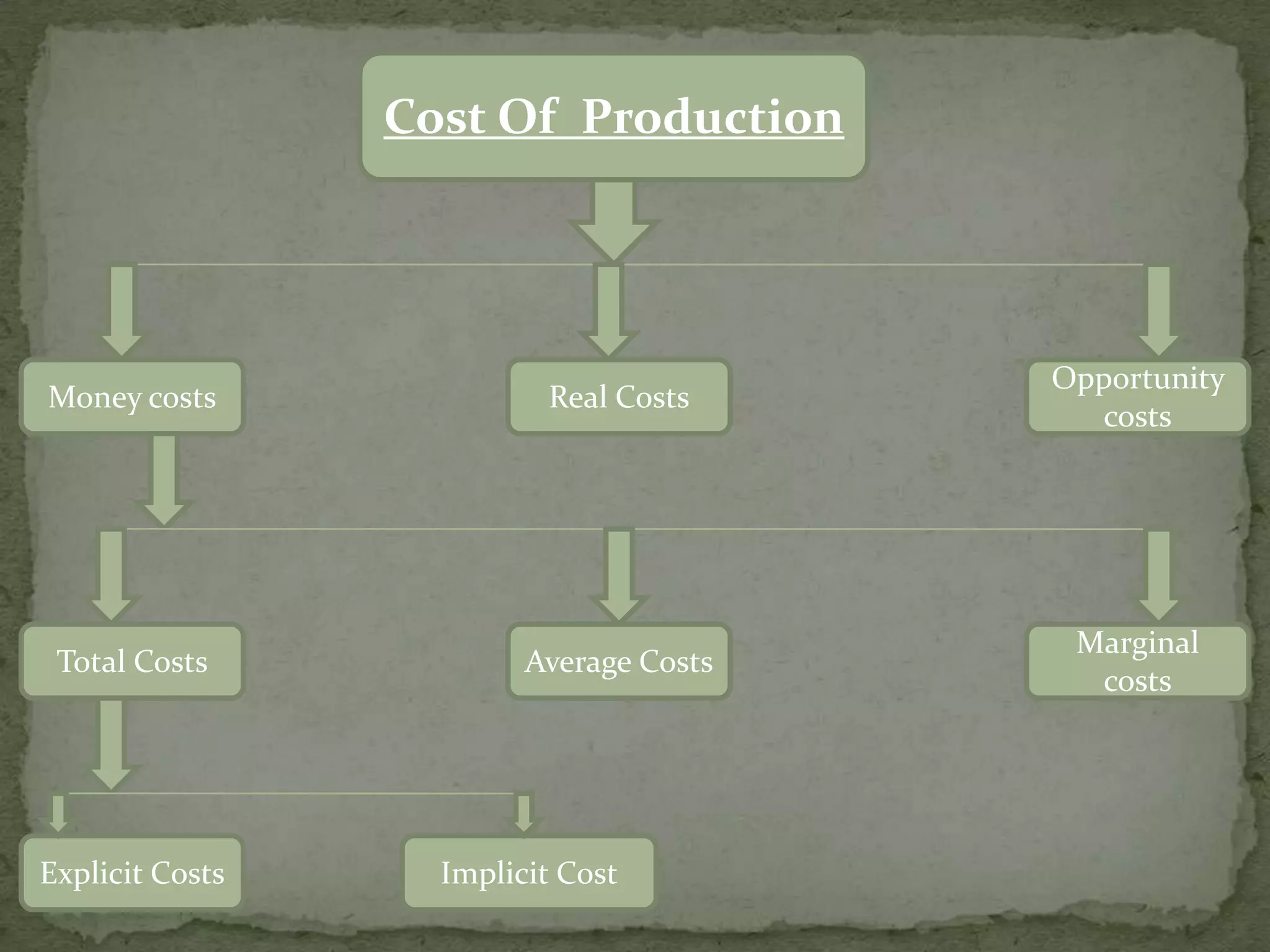

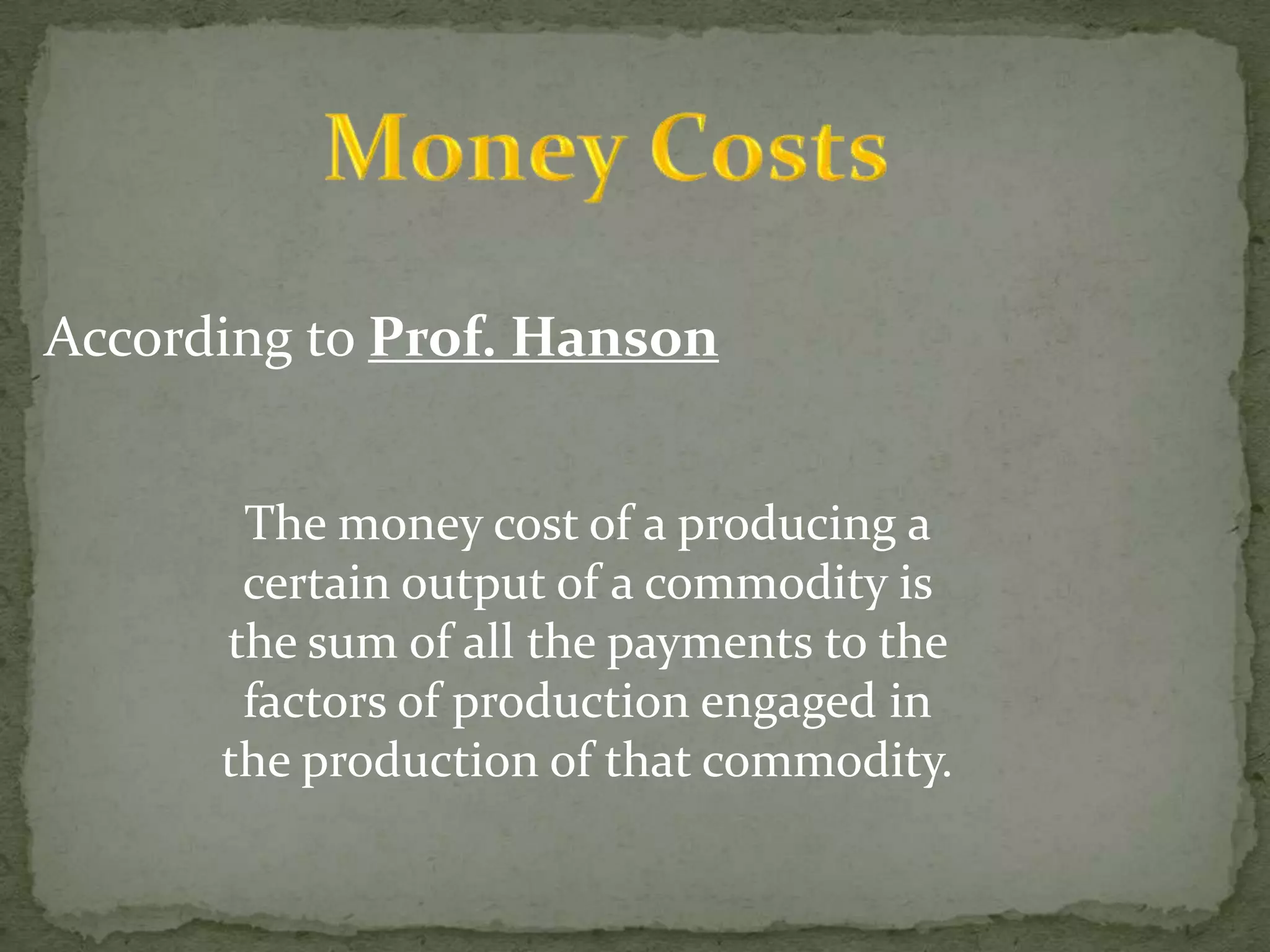

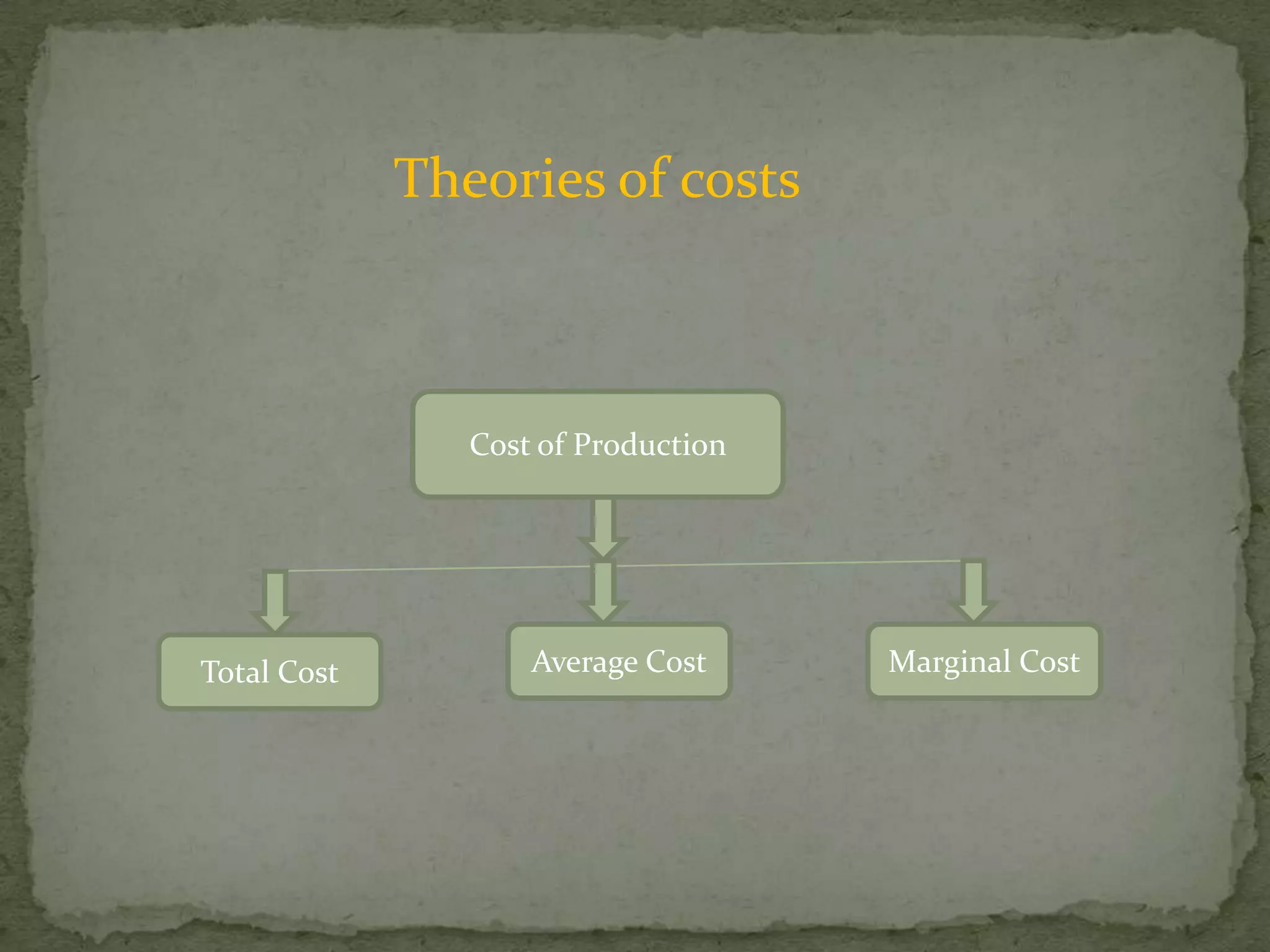

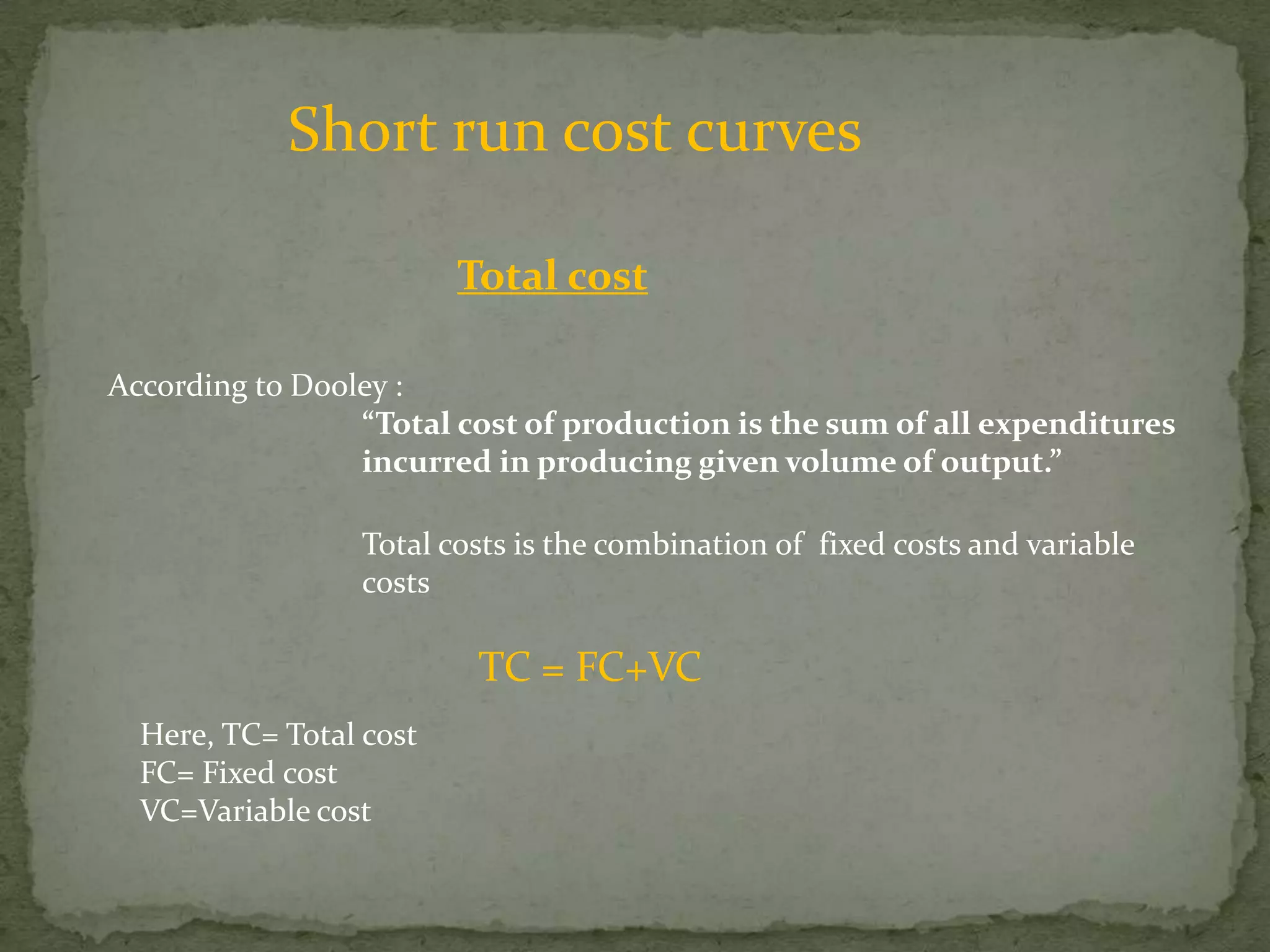

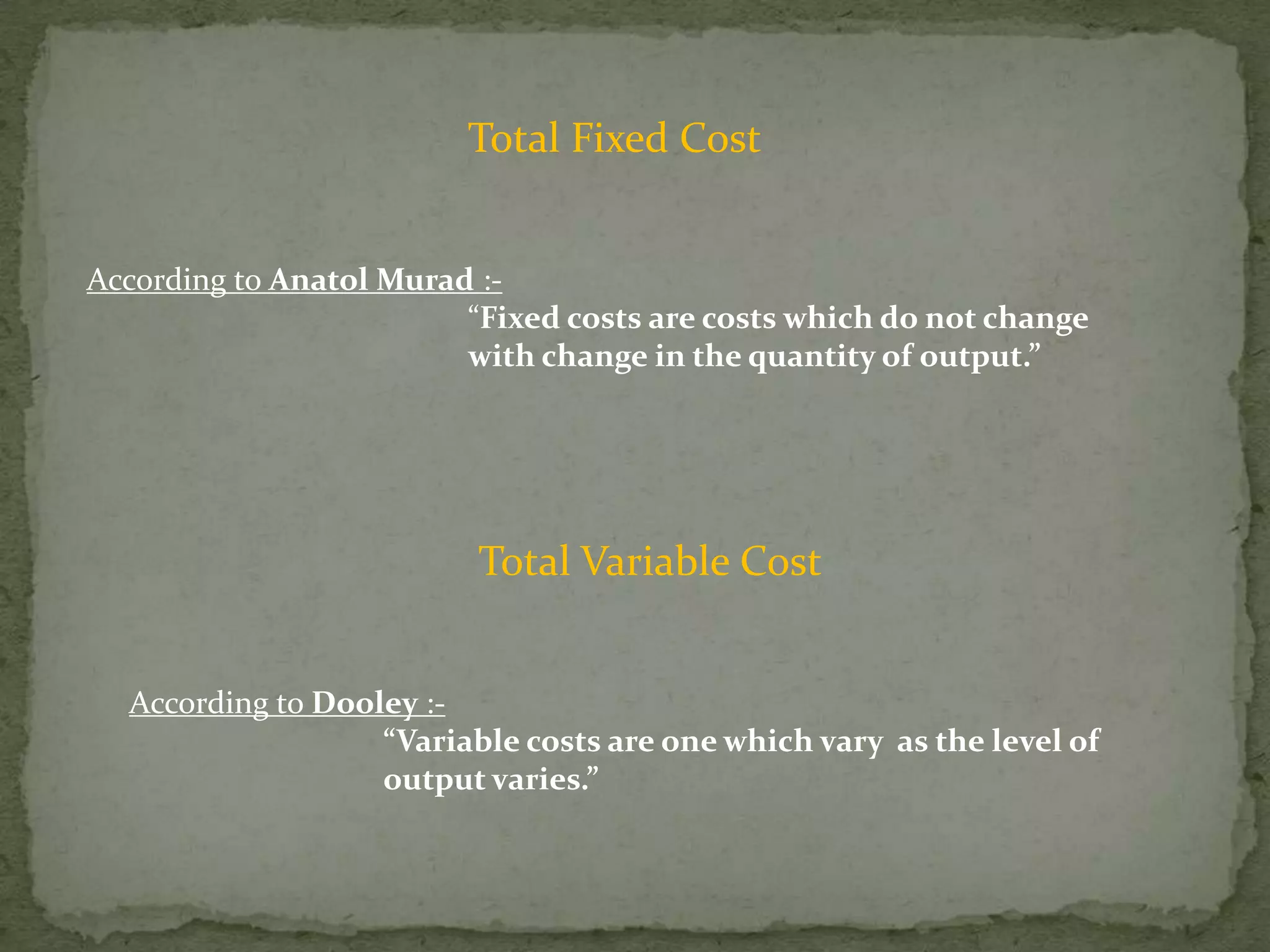

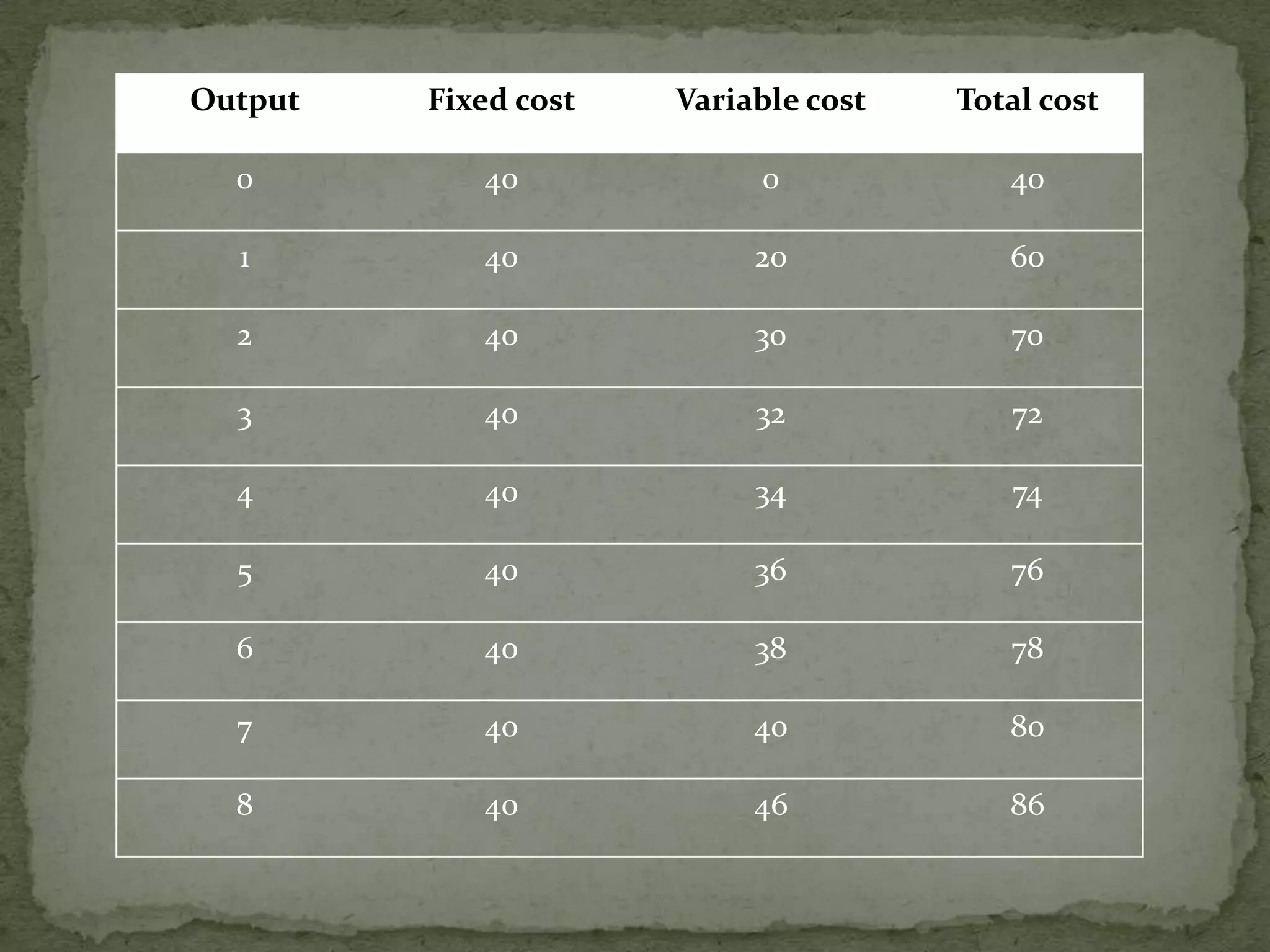

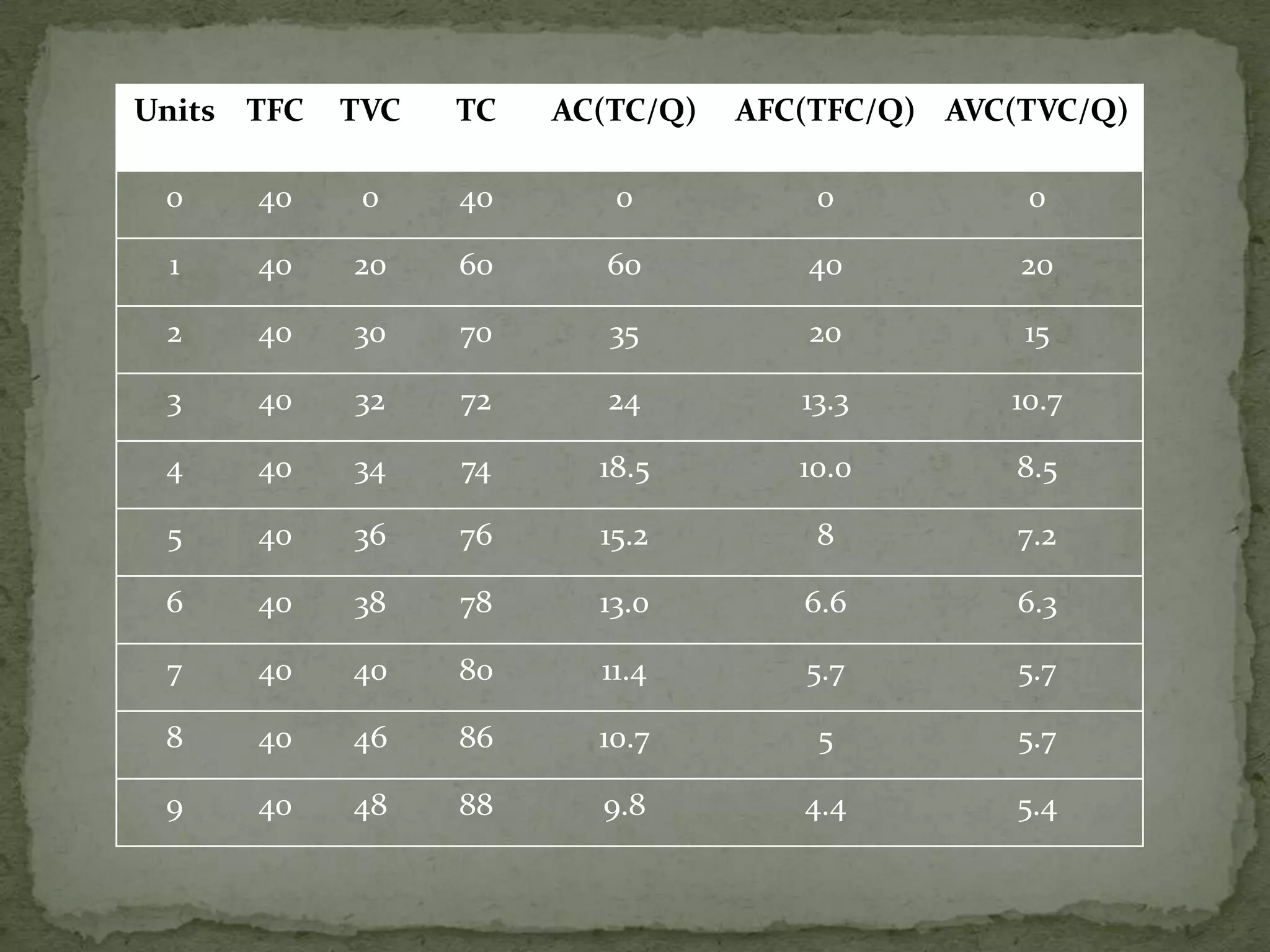

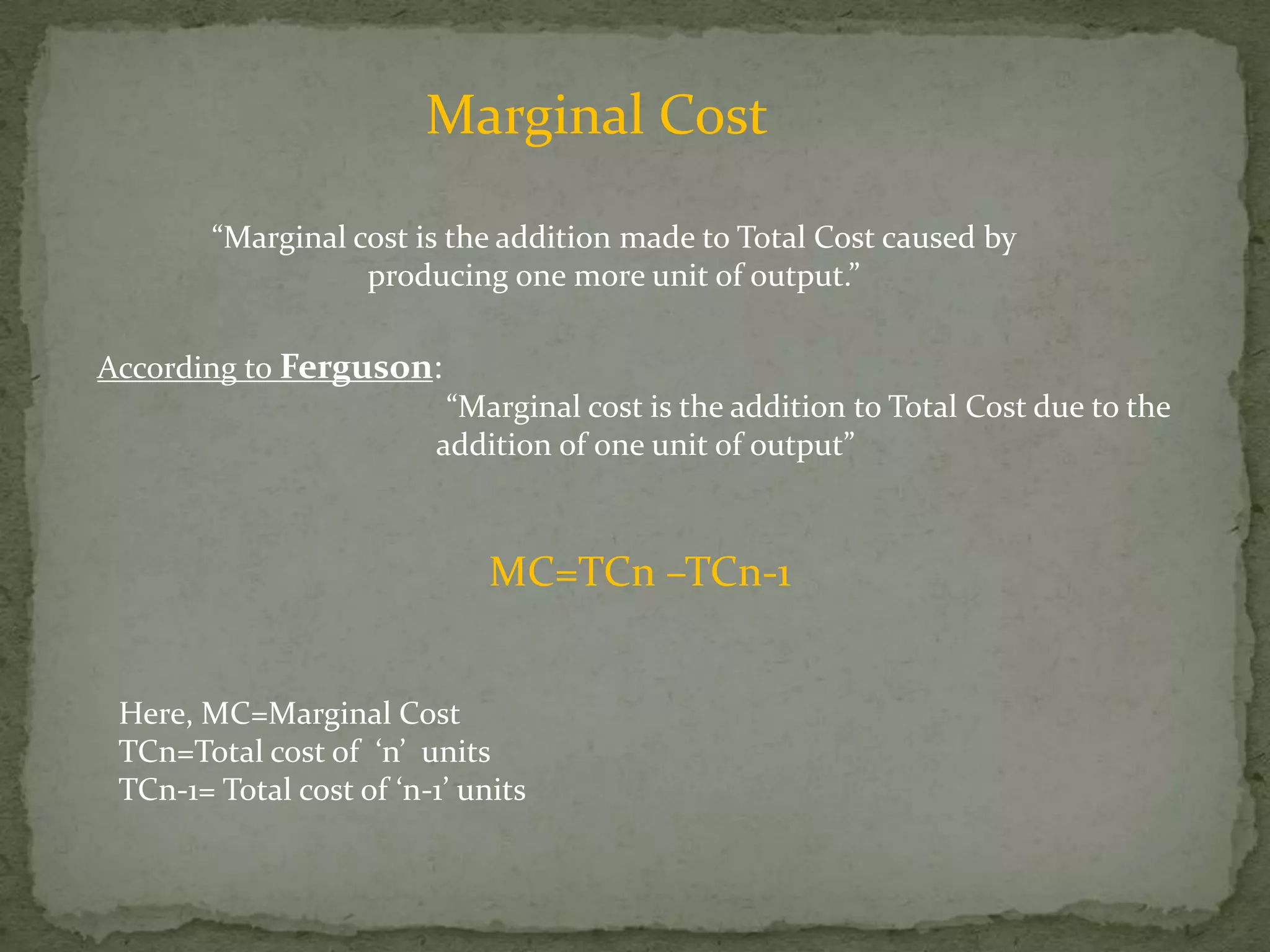

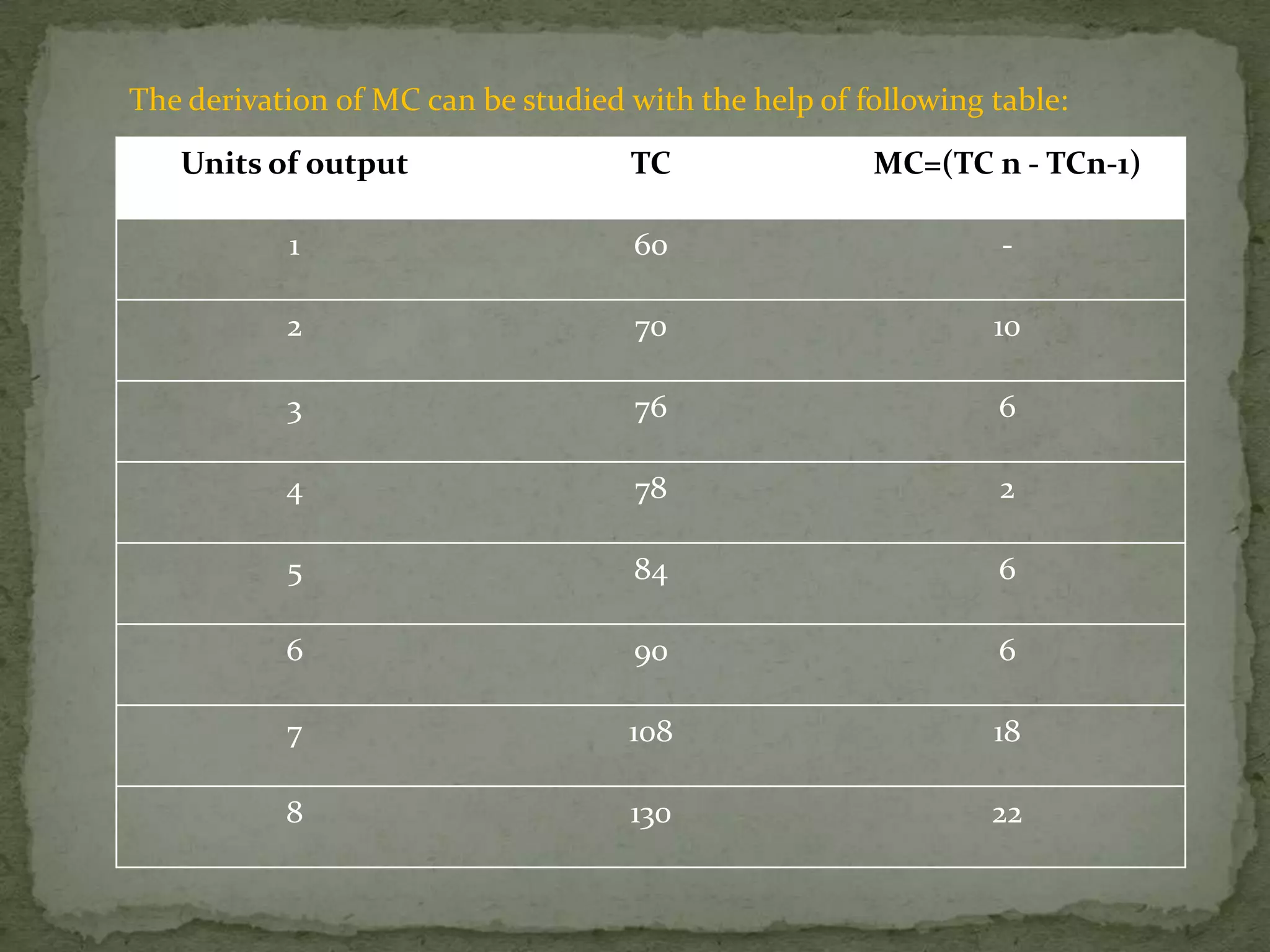

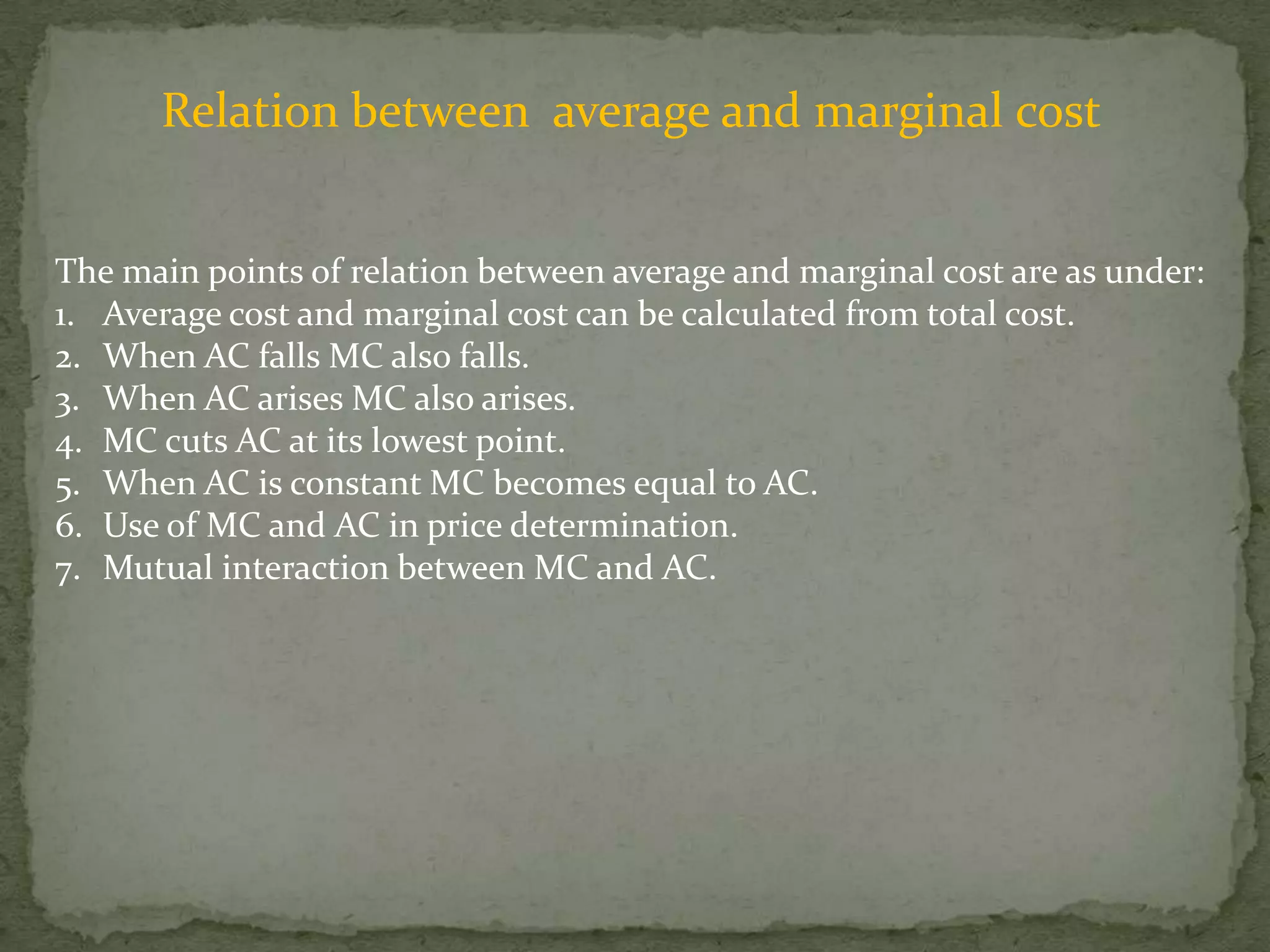

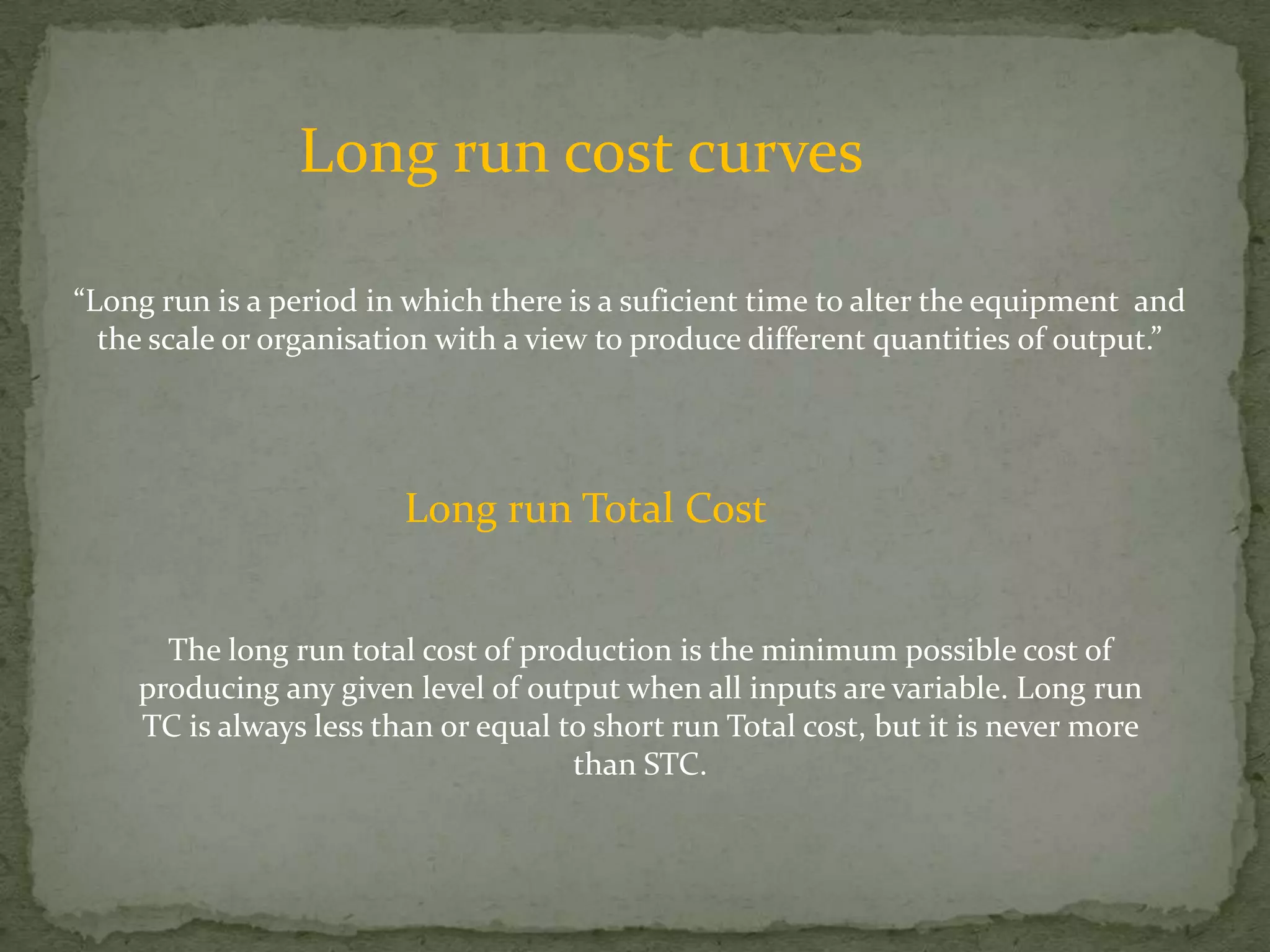

The document discusses different types of costs involved in production including money costs, real costs, opportunity costs, total costs, average costs, and marginal costs. It defines these terms and explains how they are calculated. For example, total cost is the sum of fixed and variable costs, average cost is total cost divided by output, and marginal cost is the change in total cost from producing one more unit. The document also discusses short-run and long-run cost curves including how average and marginal costs are related in both the short-run and long-run.