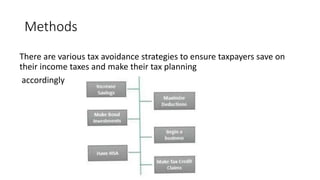

This document discusses tax planning, tax avoidance, and tax evasion. It provides information on the objectives of tax planning such as reduction of tax liability and promotion of economic growth. Tax avoidance is defined as using legal methods like deductions and credits to minimize taxes owed, while tax evasion relies on illegal underreporting of income. Some common tax avoidance methods mentioned include savings in retirement accounts, deductions for expenses, investments with tax advantages, starting a business, health insurance, and tax credits. The key difference between avoidance and evasion is that avoidance uses legal methods while evasion involves illegal underpayment or non-payment of taxes owed.

![Copy-of-Copy-of-Action-Research-in-Education[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/copy-of-copy-of-action-research-in-education1-251215094530-4aa5dedc-thumbnail.jpg?width=640&height=640&fit=bounds)