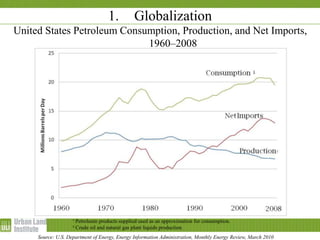

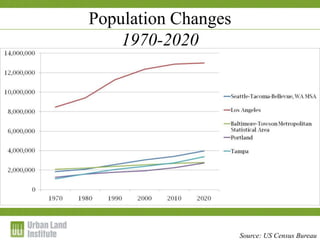

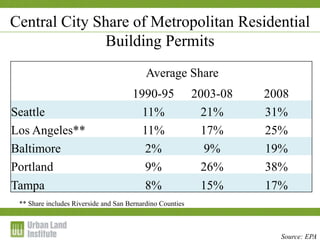

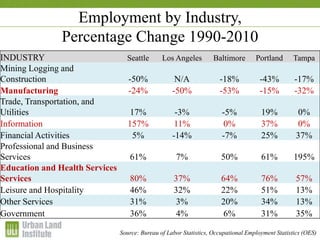

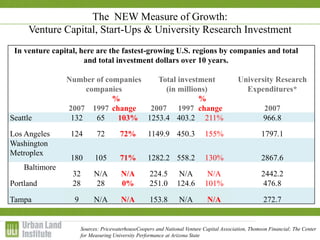

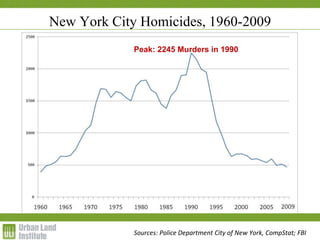

The document discusses key trends and challenges facing cities including globalization, climate change, technological innovation, aging infrastructure, and changing demographics. It analyzes population and employment changes in various cities between 1970-2020 and investment in areas like venture capital and university research. Quality of life factors like parks, culture and education are also examined. Lessons for cities include the need for leadership, a clear vision and goals, institutional capacity, transparency, appropriate financing, land control, design excellence, and public trust in development partnerships.