Downloaded 382 times

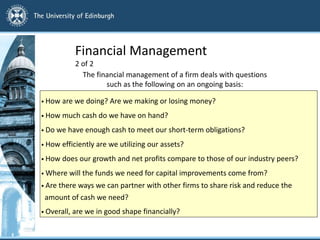

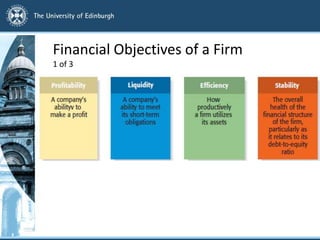

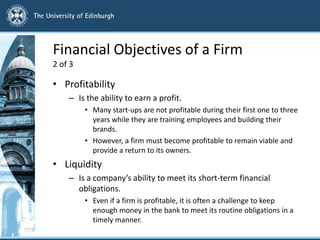

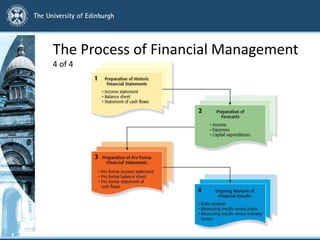

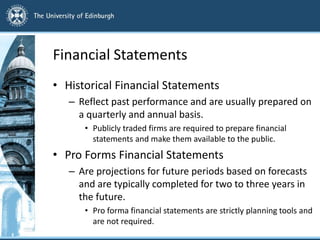

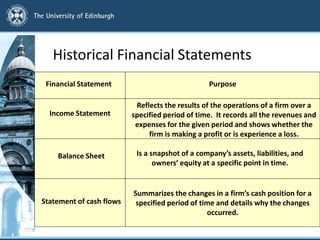

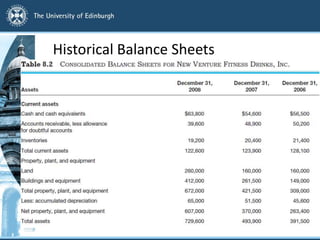

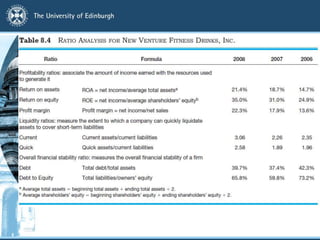

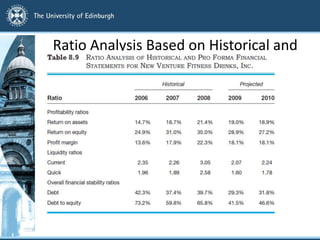

This document discusses financial management and analysis for new ventures. It explains that financial management involves raising funds and managing finances to achieve high returns. New ventures use historical and pro forma financial statements like income statements, balance sheets, and cash flow statements to assess performance and forecast future finances. Financial ratios are calculated from these statements to evaluate objectives like profitability, liquidity, efficiency and stability. Budgets and forecasts are made based on sales estimates and industry benchmarks to aid financial planning.