Downloaded 1,953 times

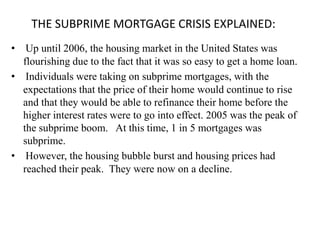

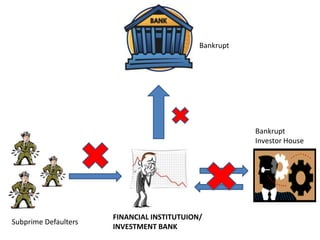

The document provides an overview of the subprime mortgage crisis, including: 1) It explains what subprime and prime loans are and defines what a crisis is. 2) The housing bubble burst as home prices declined after peaking in 2006, increasing foreclosures. 3) This sent a shock through the financial system as investment banks and other institutions incurred major losses on mortgage-backed securities.

![Subprime Under Ethics 980105 [Compatibility Mode]](https://cdn.slidesharecdn.com/ss_thumbnails/subprimeunderethics-980105compatibilitymode-090531062523-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)