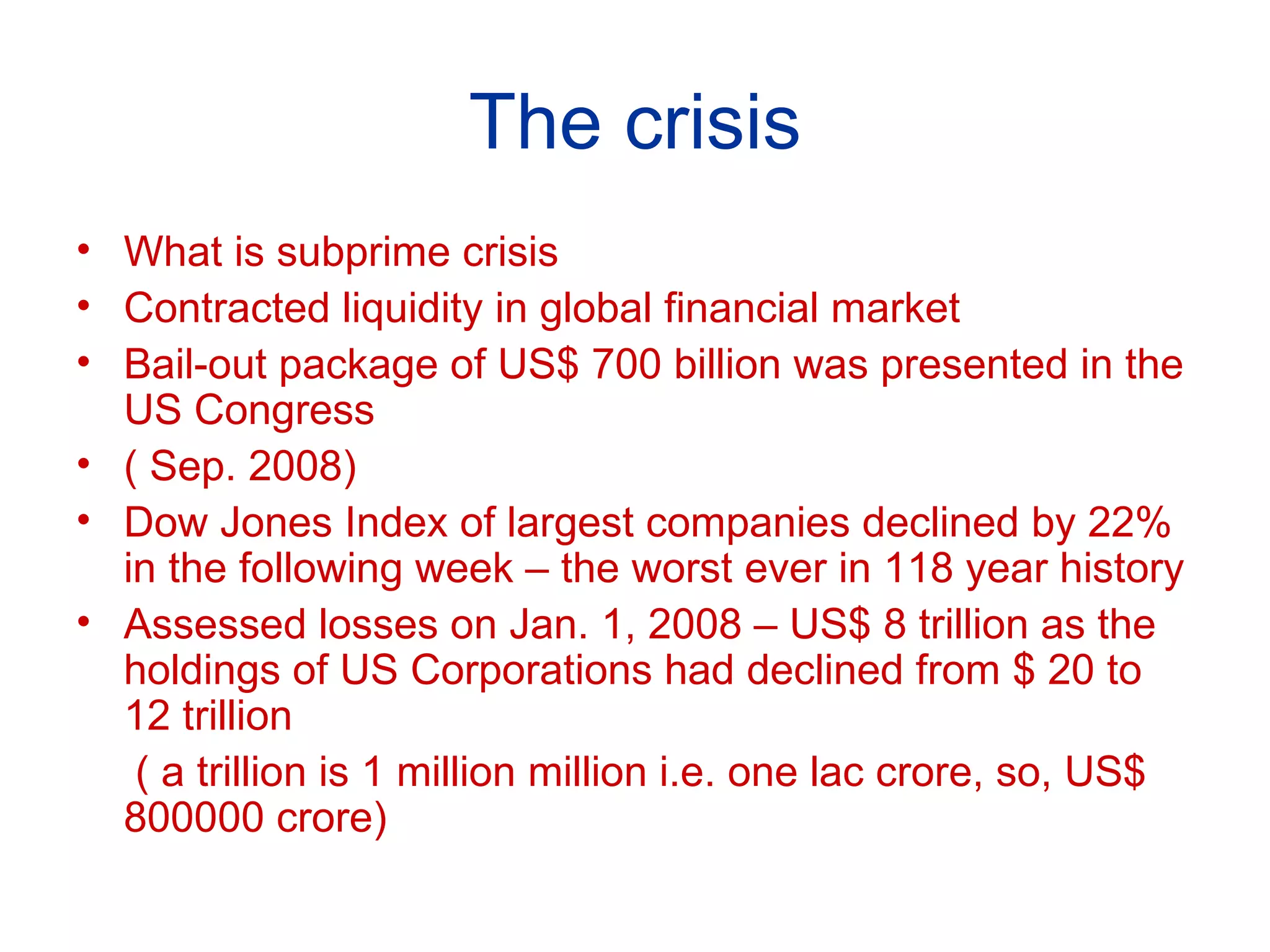

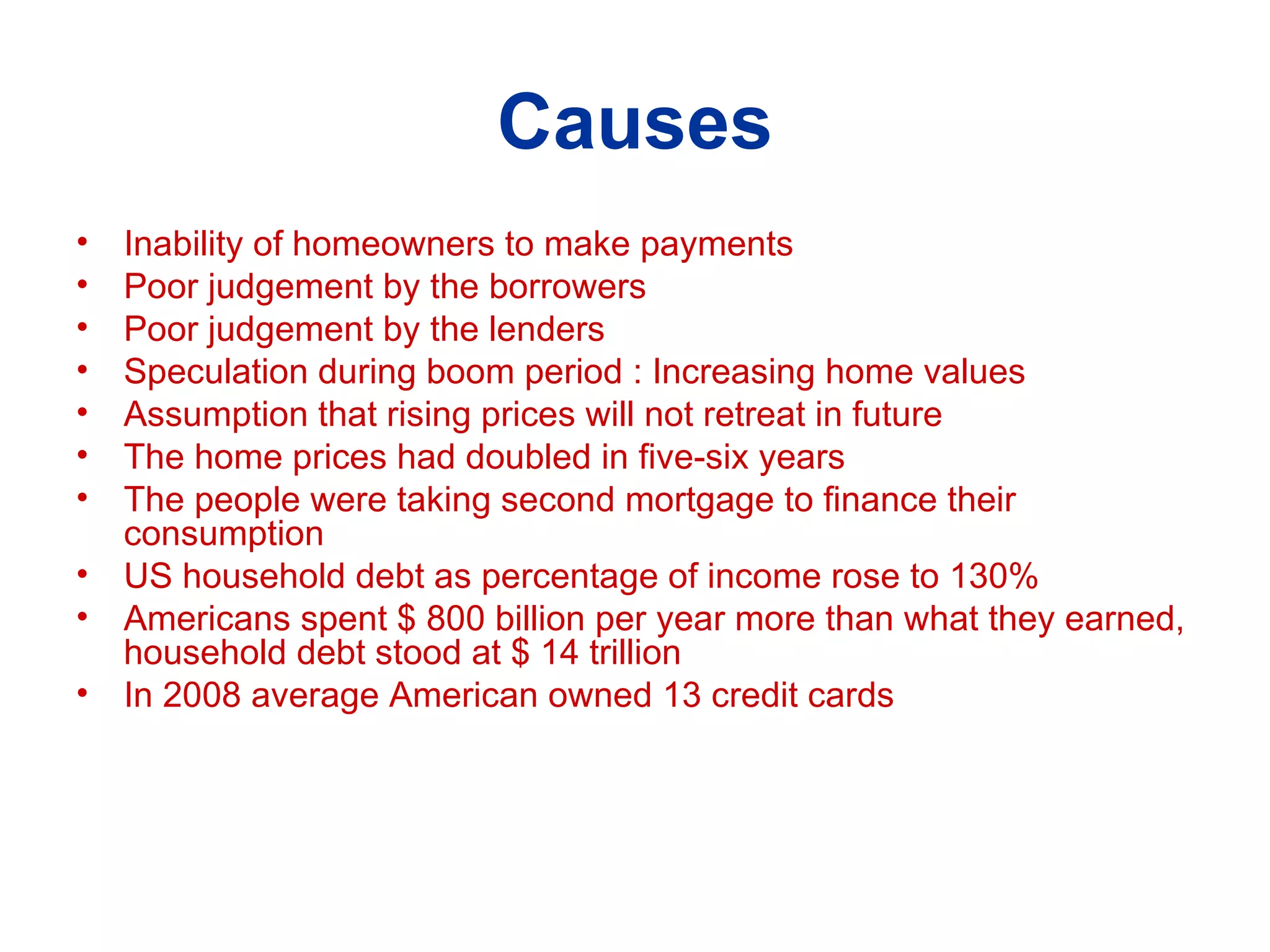

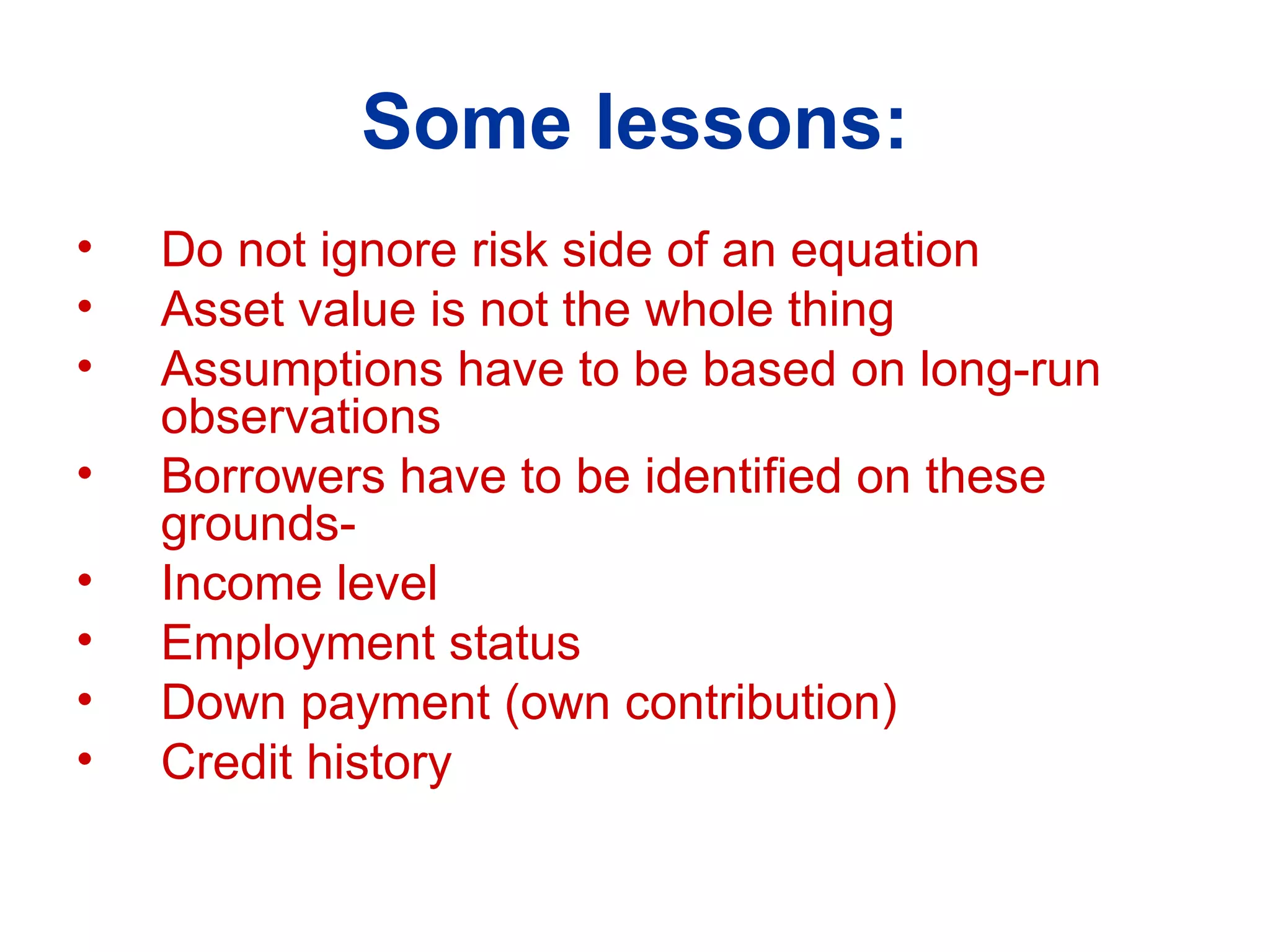

The document summarizes the subprime mortgage crisis and its global impact. It discusses how the crisis originated from risky lending practices involving subprime mortgages in the US housing market. This led to a contraction in liquidity and credit markets globally. Major financial institutions suffered huge losses totaling over $8 trillion. The crisis highlighted failures in mortgage underwriting, risky financial products, and lack of oversight that allowed risk to accumulate in the system.

![Subprime Under Ethics 980105 [Compatibility Mode]](https://cdn.slidesharecdn.com/ss_thumbnails/subprimeunderethics-980105compatibilitymode-090531062523-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)