Downloaded 31 times

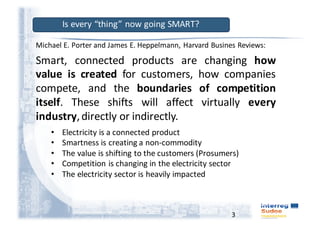

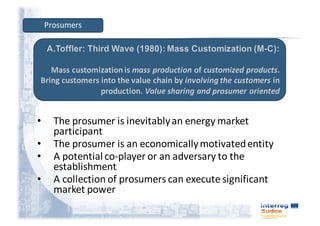

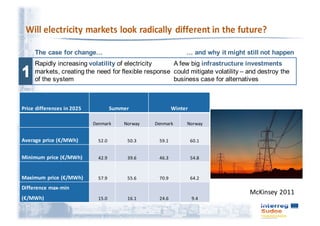

This document summarizes a presentation on smart grids given at a workshop in Barcelona, Spain in 2017. It discusses how the electricity system may look different in 20 years due to digitalization, with smart connected products changing competition. It also notes the potential for prosumers, or consumer-producers, to have significant market power if they collectively participate in energy markets. Finally, it discusses the case for transitioning to smart grids but also reasons why change may not fully materialize, such as certain large infrastructure investments undermining alternatives or business cases being too dependent on local conditions.

![[Smart Grid Market Research] Energy 2.0: Smart Grid Roadmap, 2012 – 2022, May...](https://cdn.slidesharecdn.com/ss_thumbnails/energy20smartgridroadmap20122022may2012zprymeandclasma-120530111428-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)