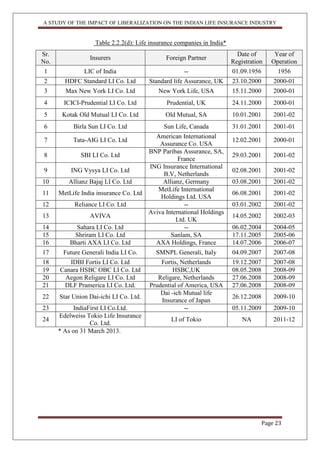

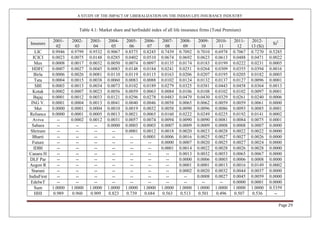

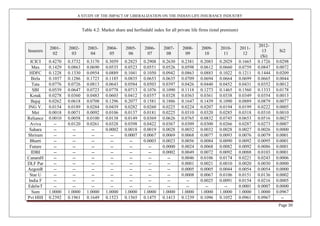

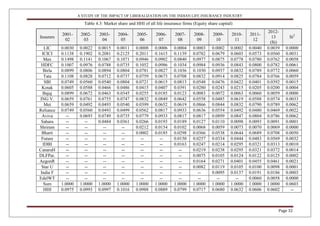

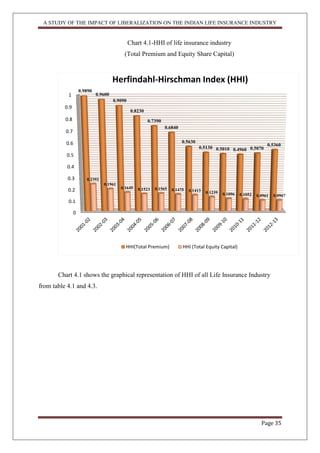

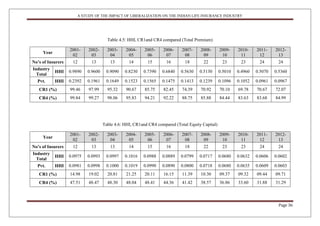

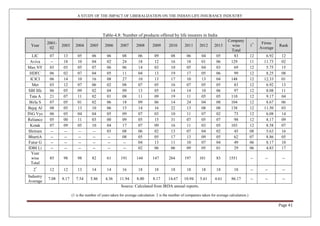

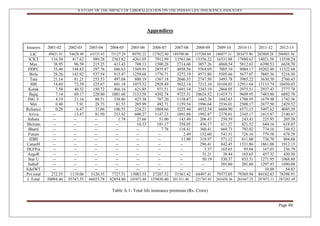

This project report analyzes the impact of liberalization on the Indian life insurance industry, focusing on the changes brought about by deregulation, competition, and entry of private players. It outlines the historical context, data analysis, and methodology used, and discusses the implications of these reforms on market concentration, efficiency, and customer service. The study spans the period from 2001-2013 and evaluates the extent to which the objectives of liberalization have been achieved.