Downloaded 10 times

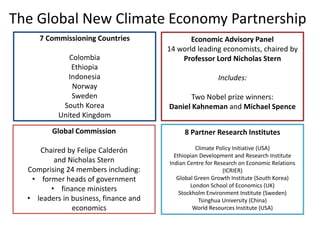

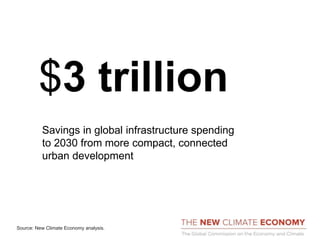

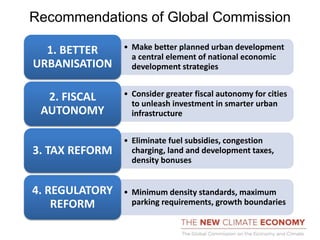

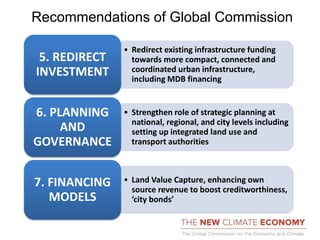

The Global New Climate Economy Partnership is a commission comprising former heads of government and other leaders, chaired by Felipe Calderón and Nicholas Stern. It aims to demonstrate that tackling climate change is an opportunity for better growth. The commission's research shows that compact, connected cities focused on public transport, energy efficiency and renewable energy can reduce emissions while saving $3 trillion in infrastructure costs by 2030. The commission recommends that countries prioritize smarter urban development, give cities more autonomy, reform taxes and regulations, redirect infrastructure spending, strengthen planning and explore new financing models to support low-carbon growth.