Download as PDF, PPTX

![“Let me state the matter as clearly as I can here: We believe

consumers should be able to access [their financial] information

and give their permission for third-party companies to access

this information as well.”

- Richard Cordray, Director, CFPB

at Money 20/20, October 2016

Challenge: Regulatory pressure

SOURCE: https://www.consumerfinance.gov/about-us/newsroom/prepared-remarks-cfpb-director-richard-cordray-money-2020/](https://image.slidesharecdn.com/finicity-webinar-03172017-170323004011/75/Revolutionizing-lending-in-today-s-digital-world-10-2048.jpg)

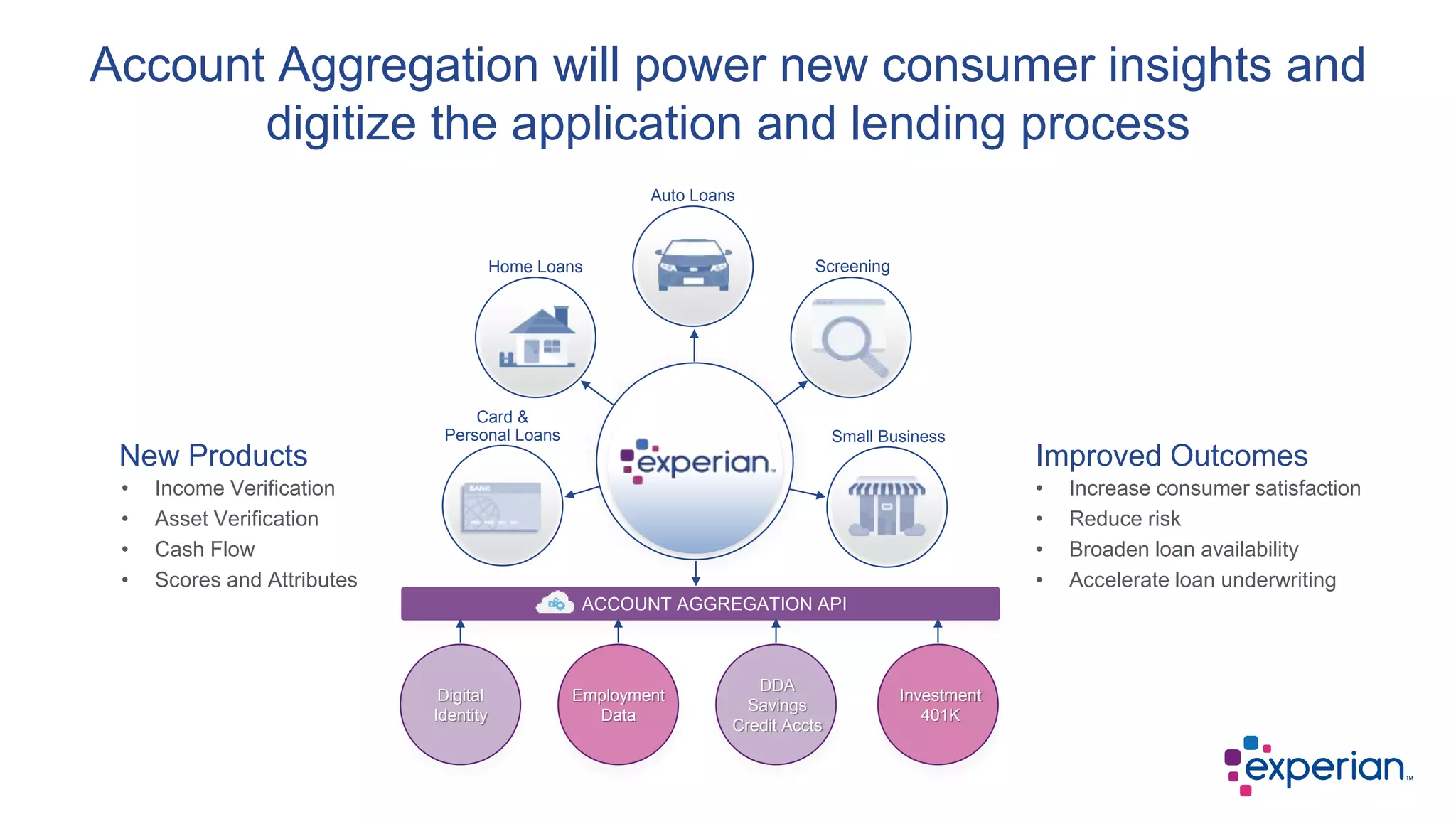

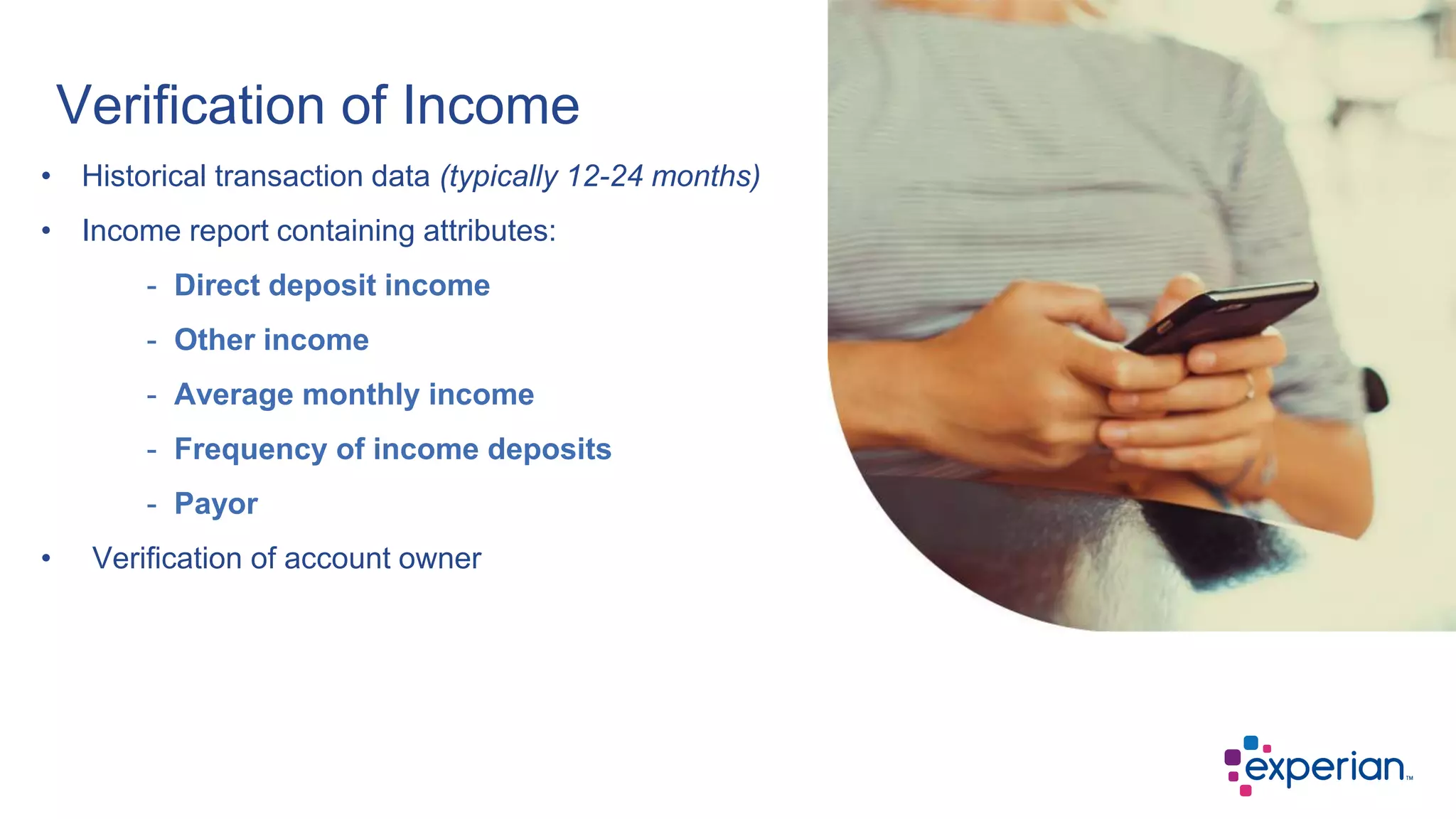

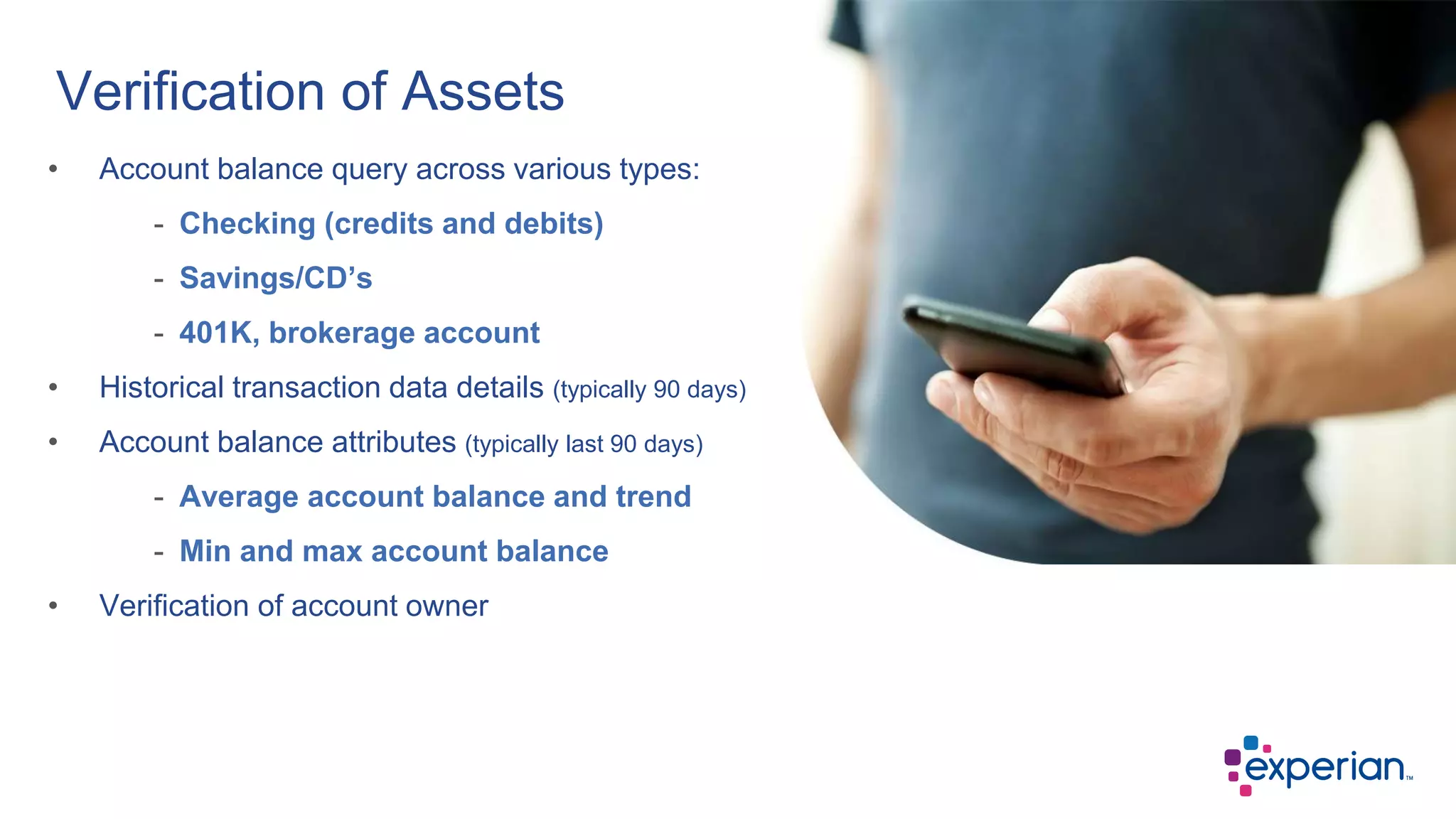

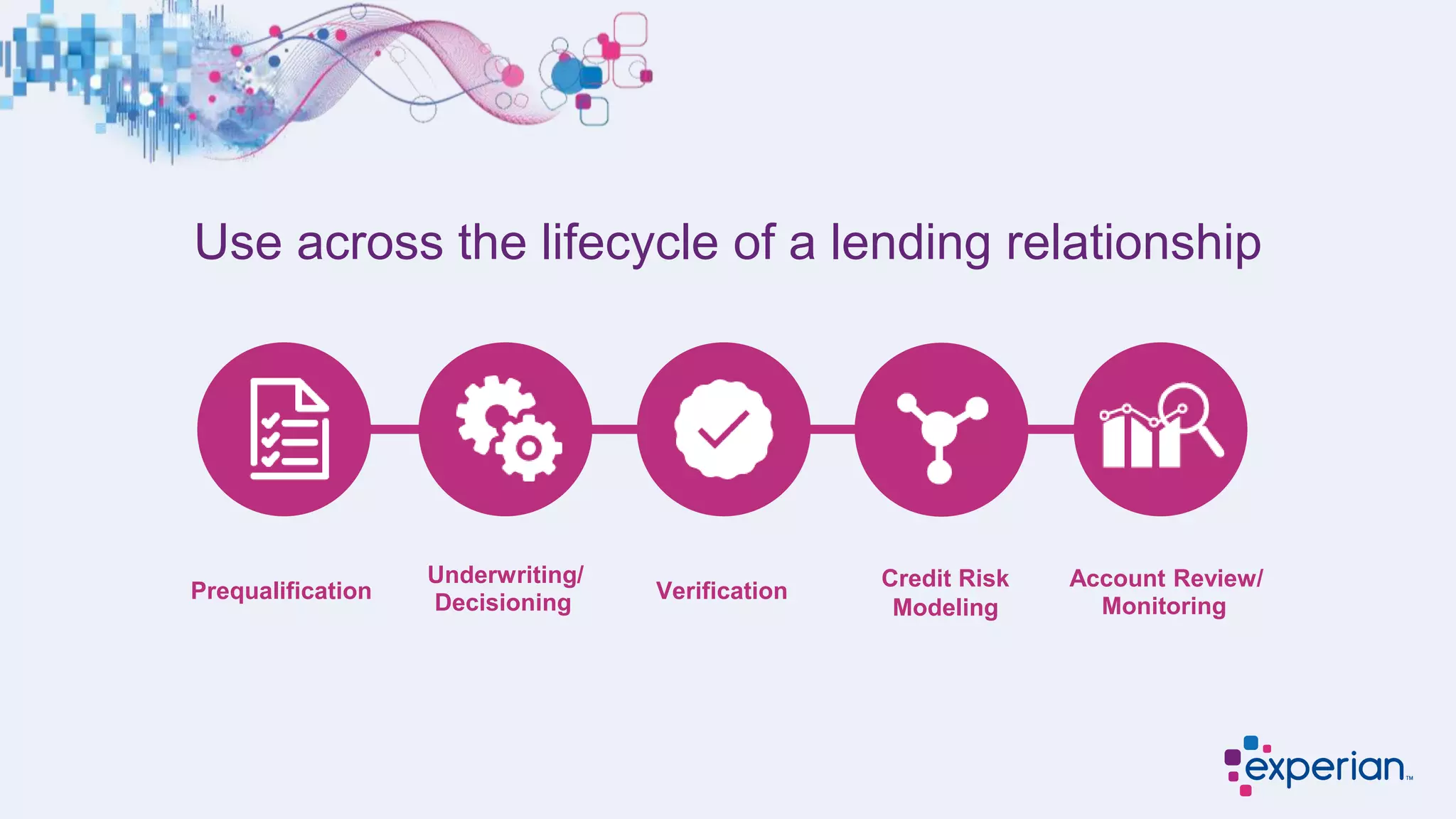

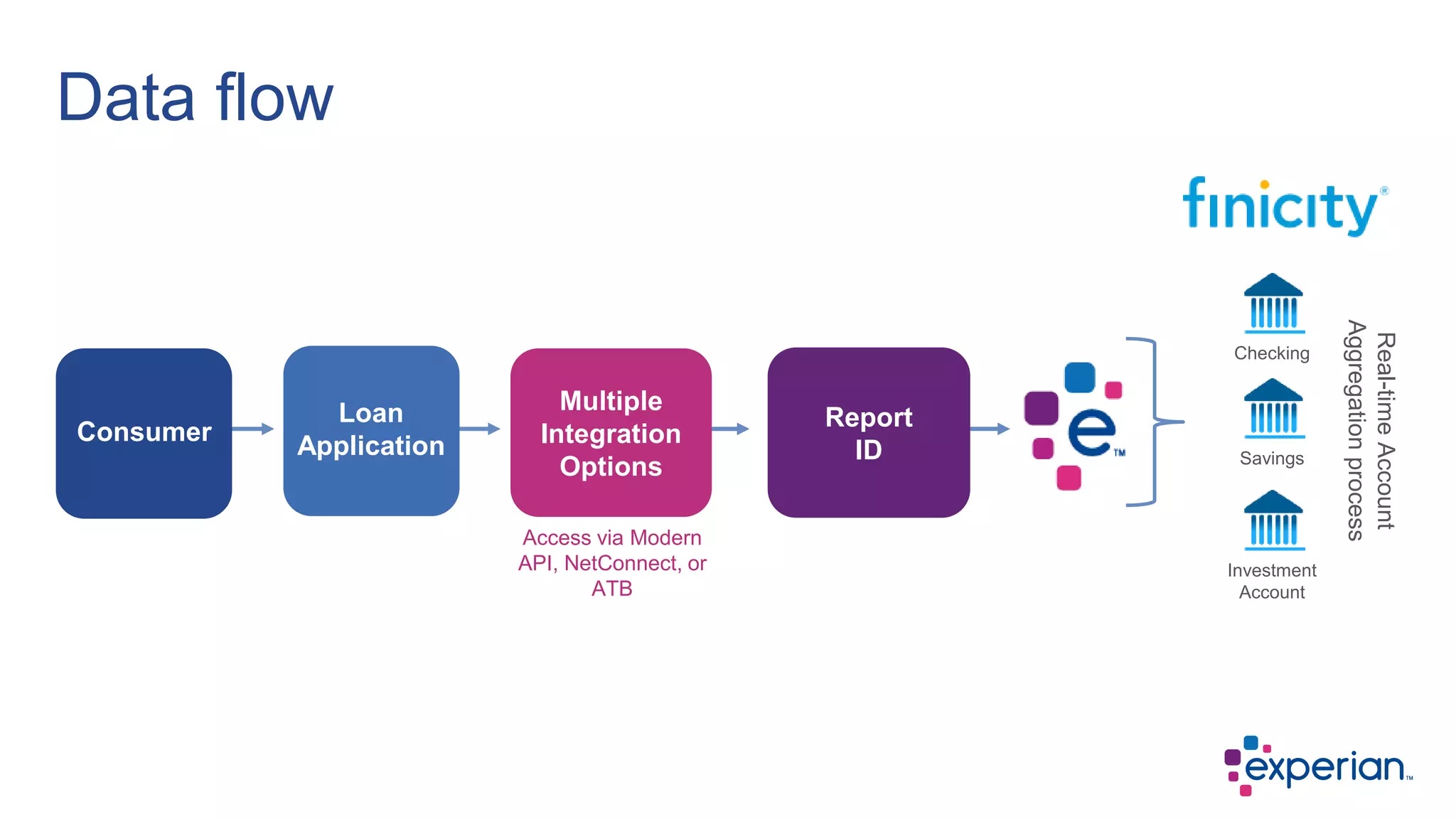

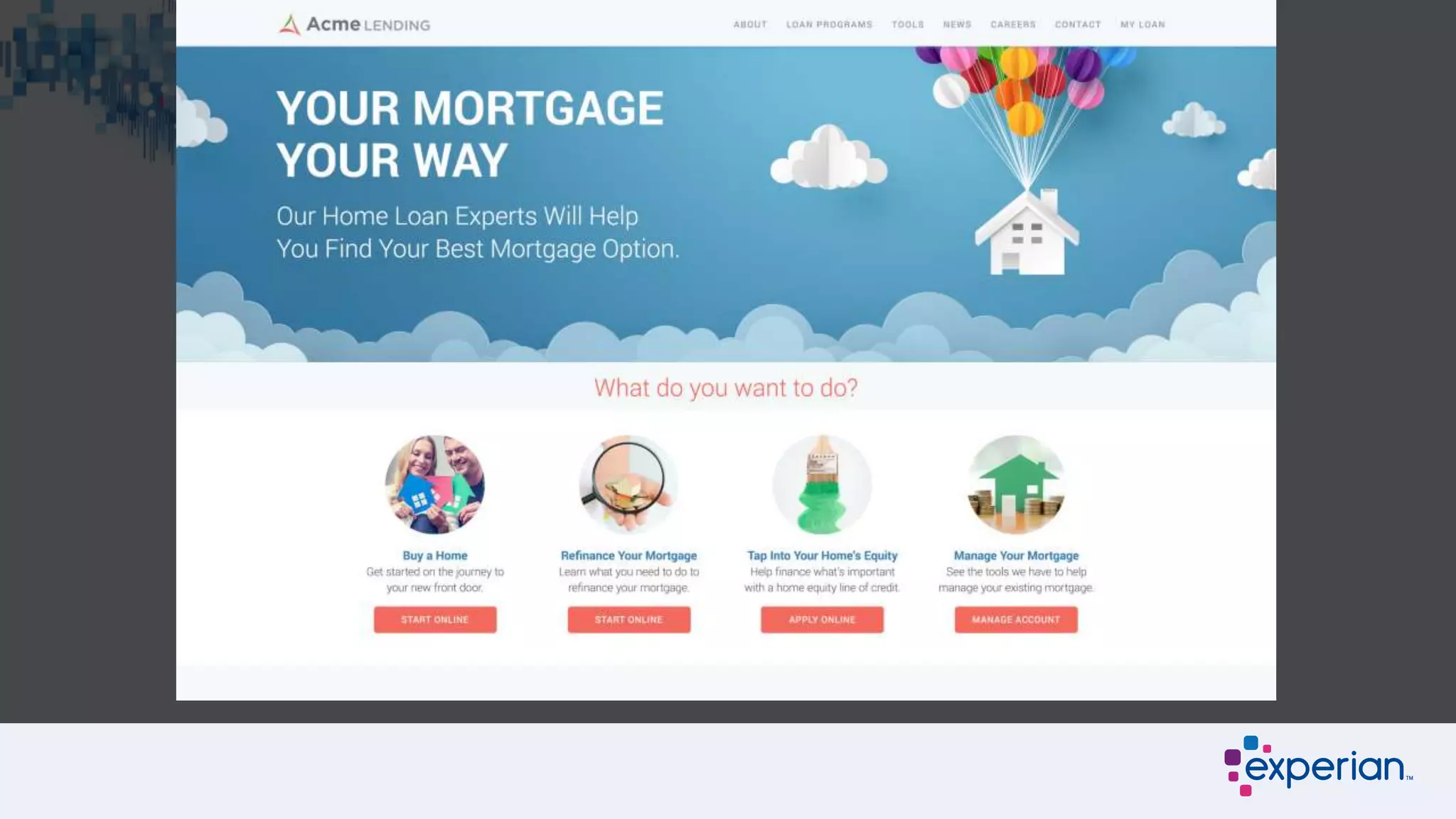

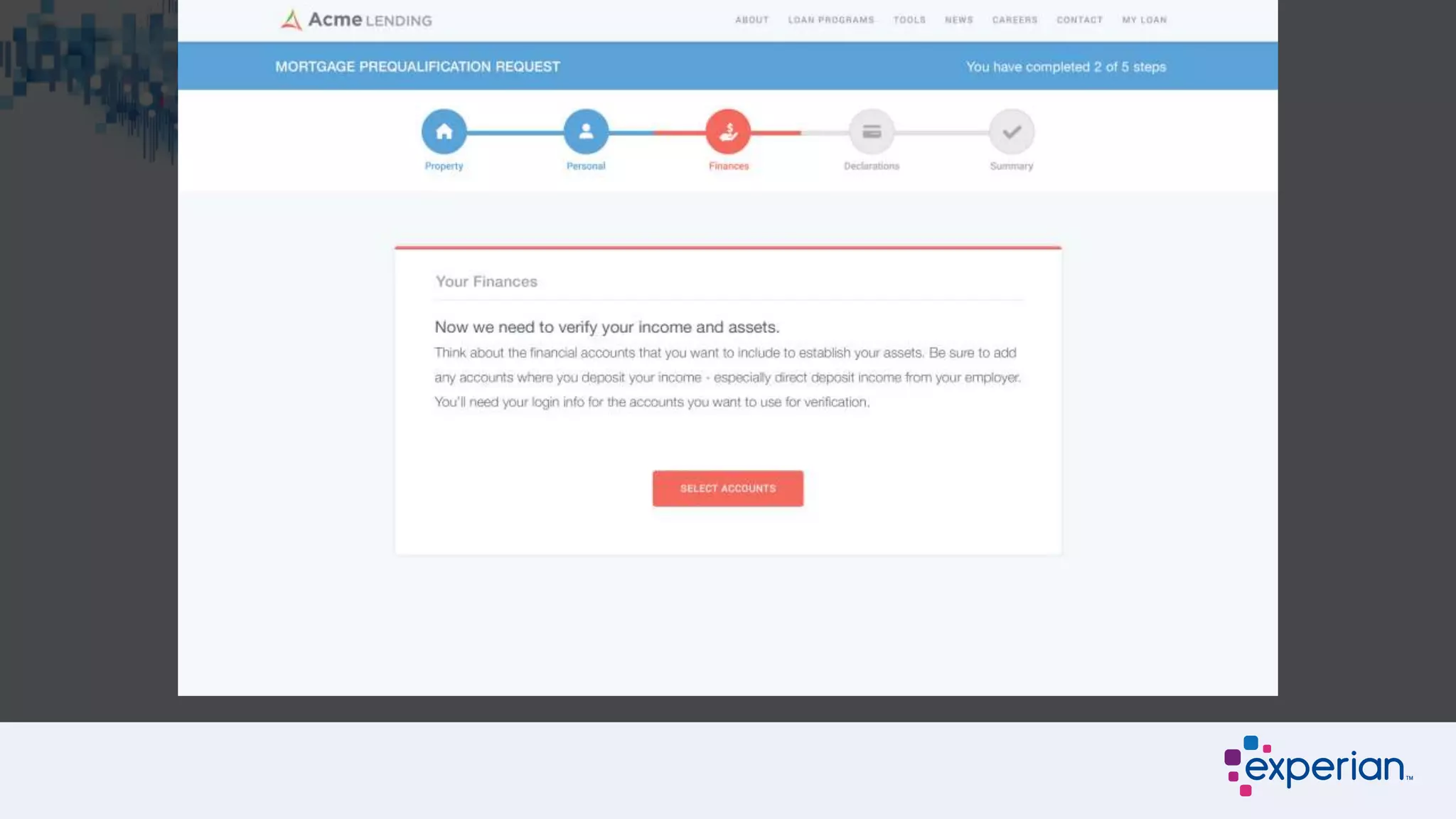

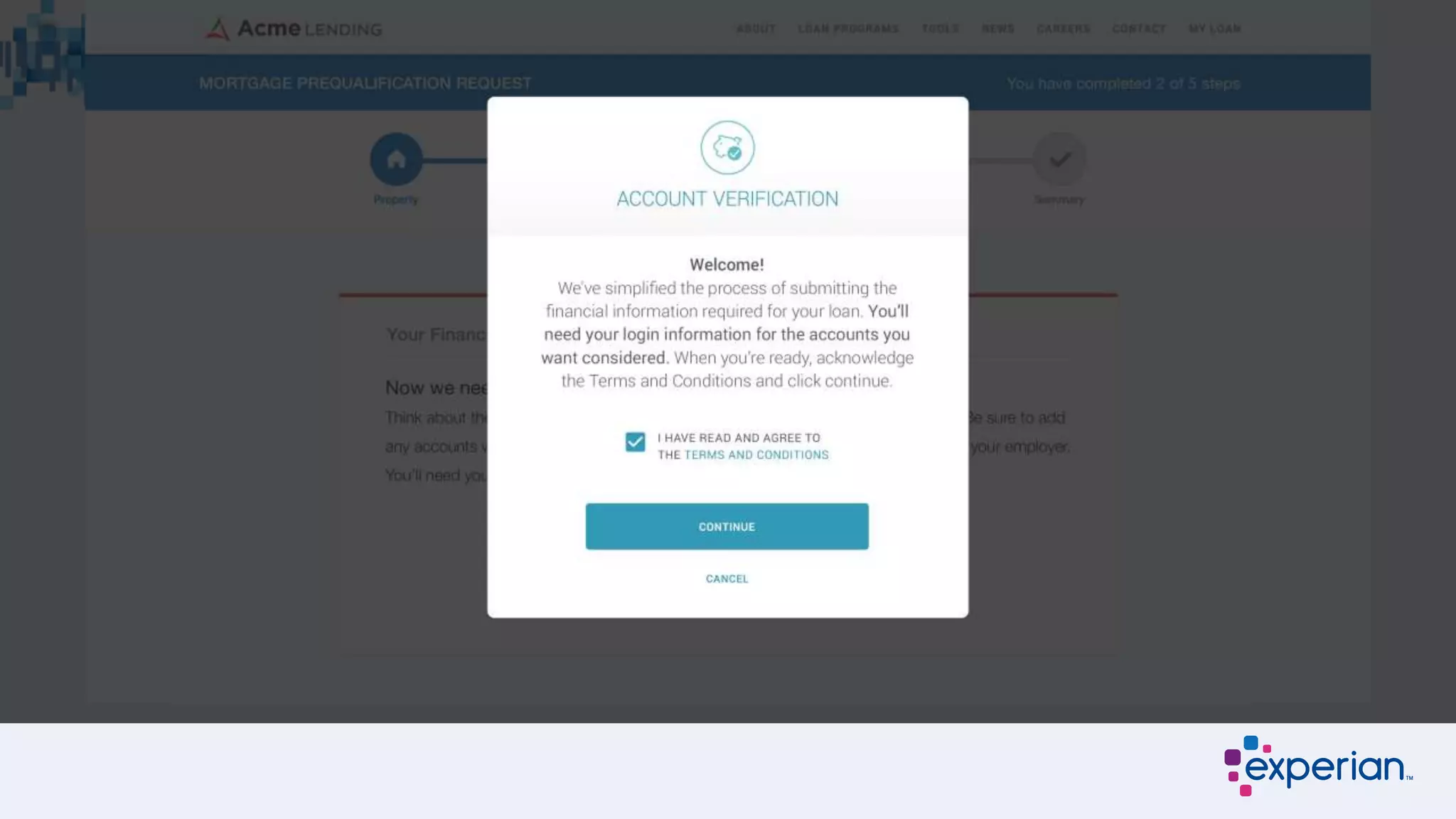

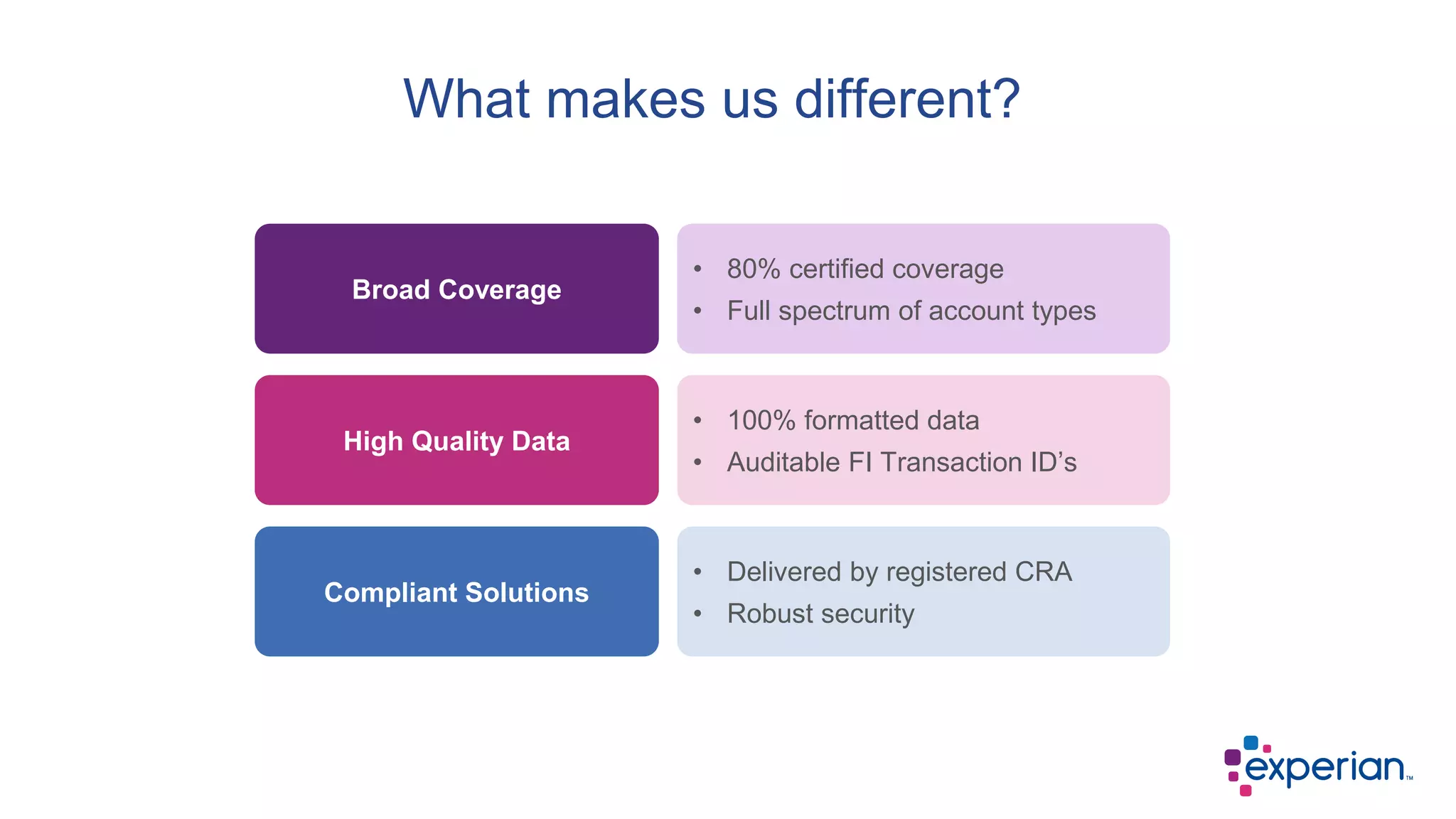

The document discusses the transformation in the lending landscape influenced by digital technology and consumer expectations. It highlights the role of account aggregation and Experian's digital transaction solutions to streamline processes, improve customer experiences, and enhance verification practices. Key challenges mentioned include regulatory pressures, outdated business models, and rising expectations for seamless digital financial services.