Downloaded 15 times

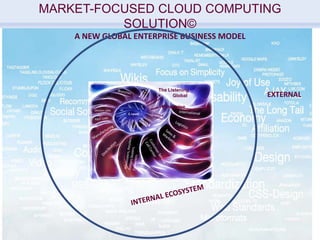

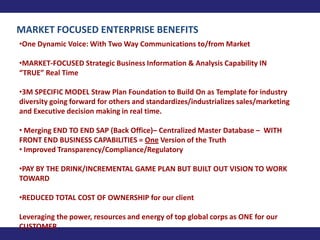

The document discusses SAP HANA in-memory processing technology and how it can be combined with cloud computing and SAP mobility solutions to provide competitive advantages. It proposes a market-focused cloud solution that uses these technologies along with big data and a patented process to create a listening, creative and responsive global enterprise with a single integrated approach focused on the customer. The solution aims to deliver faster and more efficient end-to-end cost reductions, closer customer satisfaction and leverage of business information for better decisions.

![Ams Webinar 25 March 2010 Jf Final[1]](https://cdn.slidesharecdn.com/ss_thumbnails/amswebinar25march2010jffinal1-12695451499652-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)