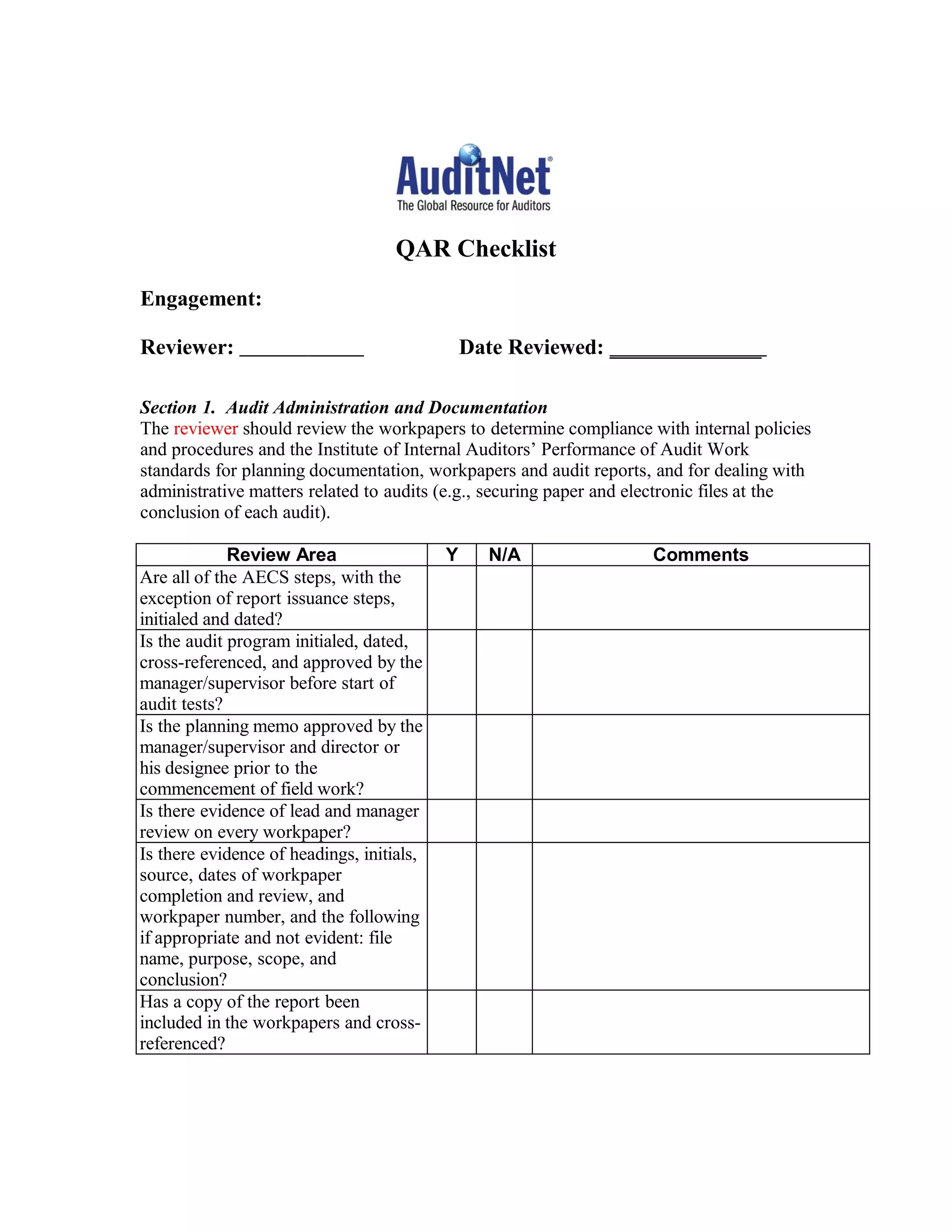

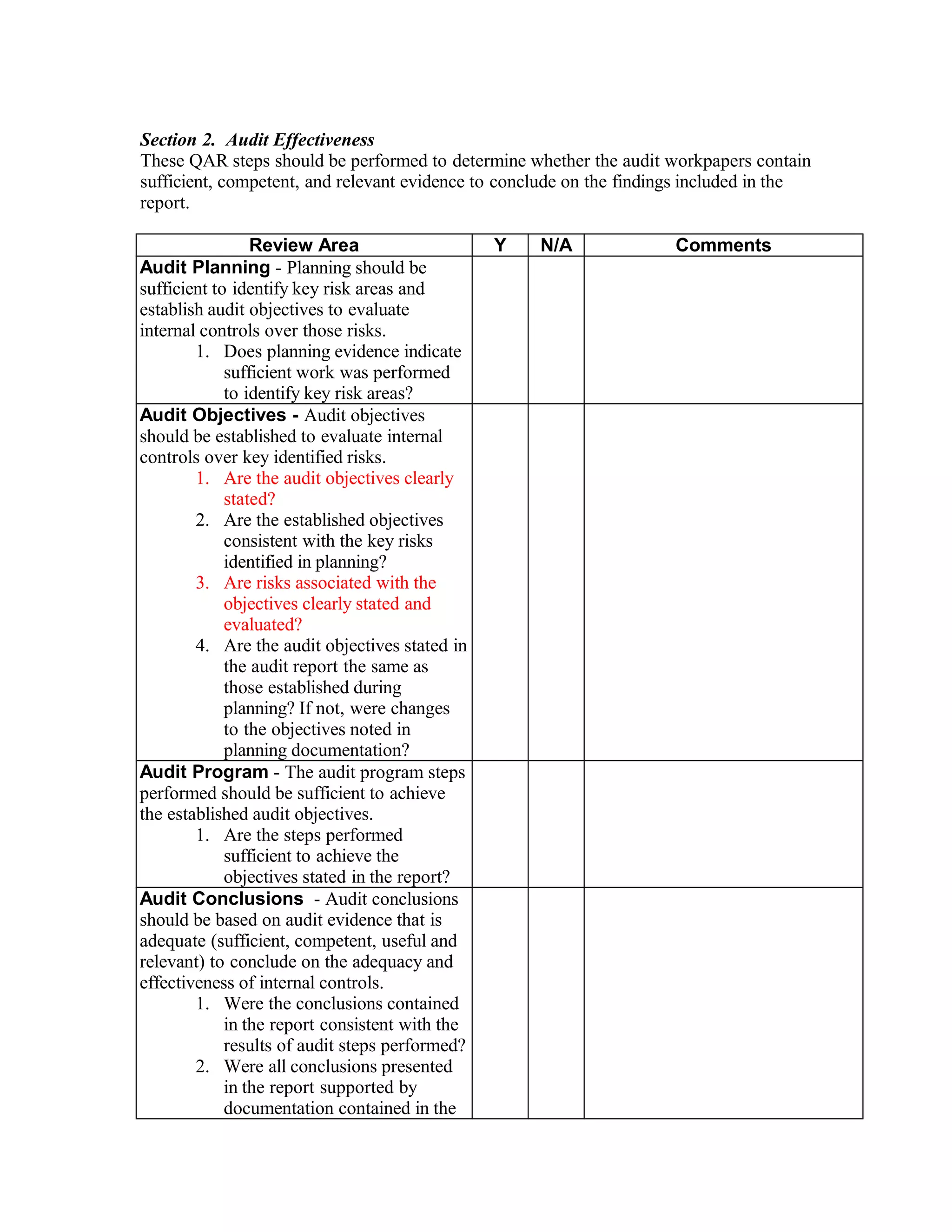

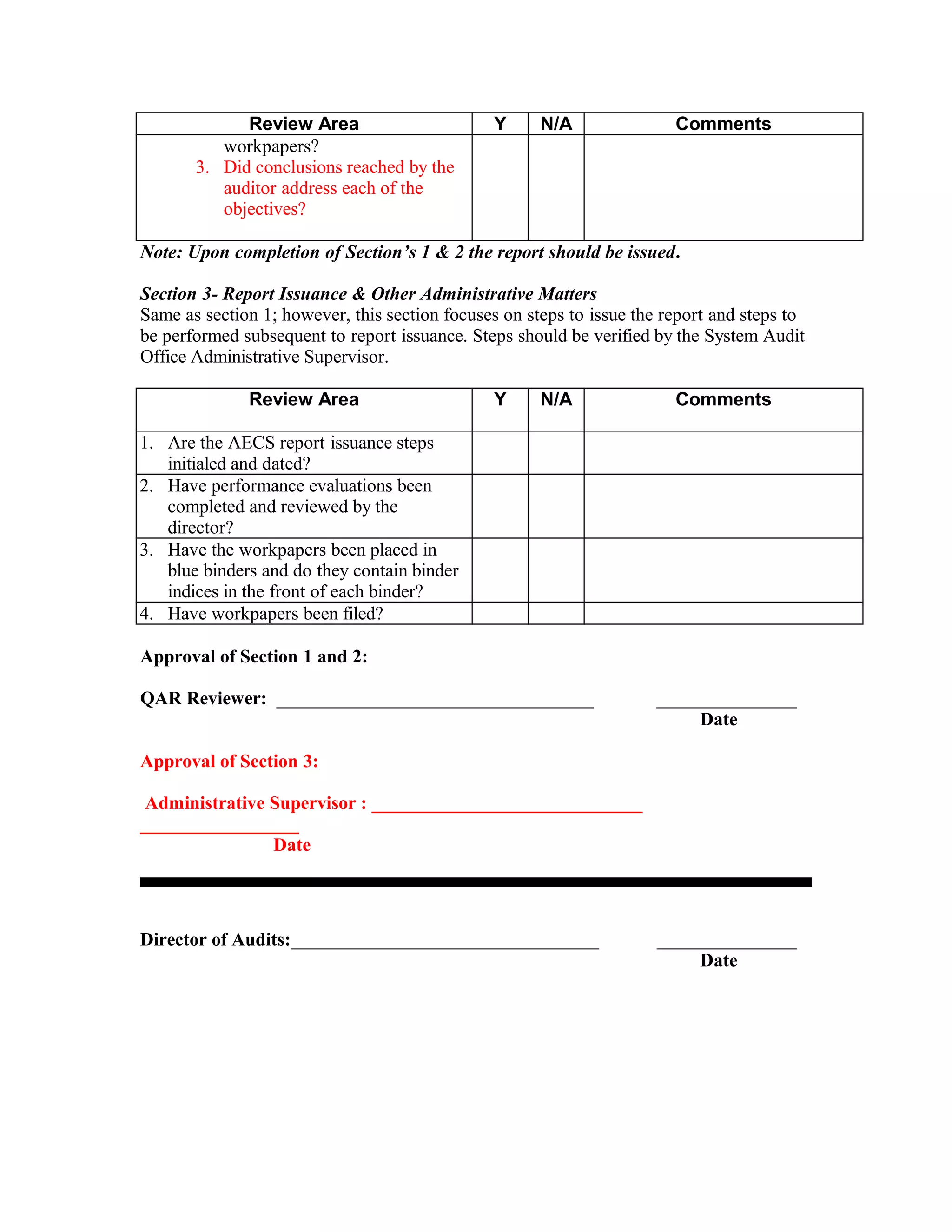

This document provides a checklist for reviewing audit documentation and workpapers. It contains 3 sections: 1) Audit administration and documentation, 2) Audit effectiveness, and 3) Report issuance and other administrative matters. Each section contains a list of review areas to check compliance with standards for planning, documentation, conclusions, and administrative procedures such as securing files. The reviewer uses the checklist to verify audits meet quality standards for key areas like objectives, program, conclusions, and proper documentation and approval of workpapers and reports.