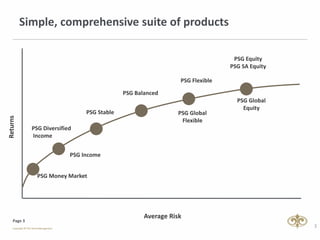

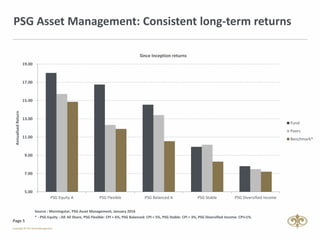

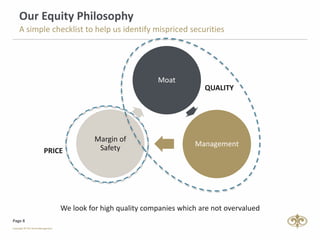

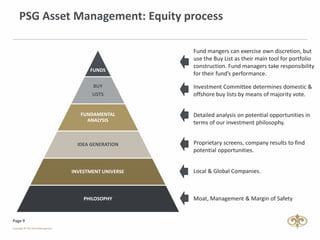

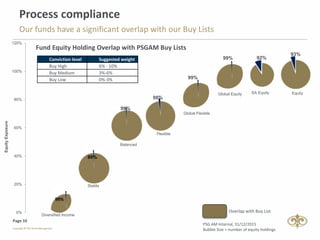

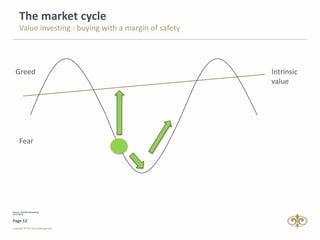

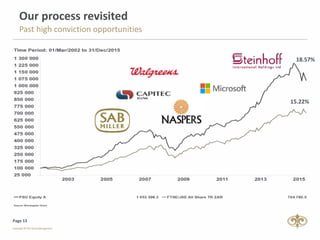

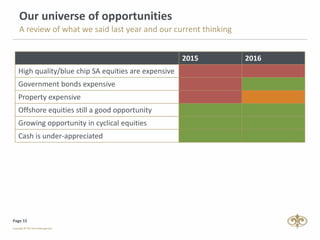

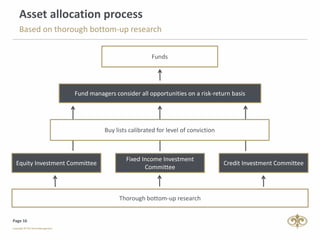

The document discusses PSG Asset Management's investment philosophy and process. It emphasizes long-term thinking, prudent risk management, and in-depth fundamental research. The summaries focus on high-level information about PSG's strategies and long-term performance across different funds.