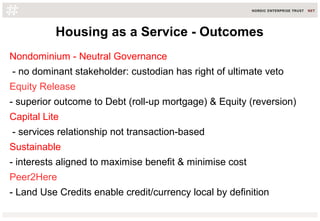

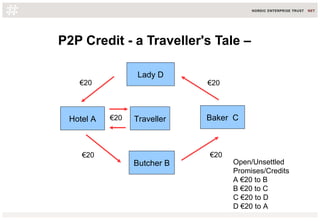

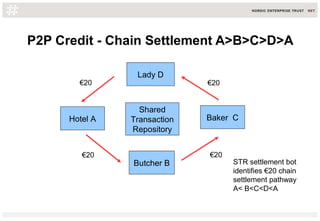

This document discusses the evolution of markets and fintech. It proposes moving from transaction-based fintech 1.0 to relationship-based fintech 2.0 that links digital currencies to real economic activity. Examples discussed include energy credit obligations that can be used to pre-pay for energy supply, and housing platforms that provide housing as a service using local land use credits. The document proposes a research project to develop community fintech prototypes in four Scottish locations to explore cooperative models of credit clearing, risk sharing, and cost sharing enabled by shared transaction repositories and digital currencies.