Downloaded 61 times

![Production Function [email_address]](https://image.slidesharecdn.com/productionfunctionlesson4-110708224040-phpapp01/75/Production-function-lesson-4-1-2048.jpg)

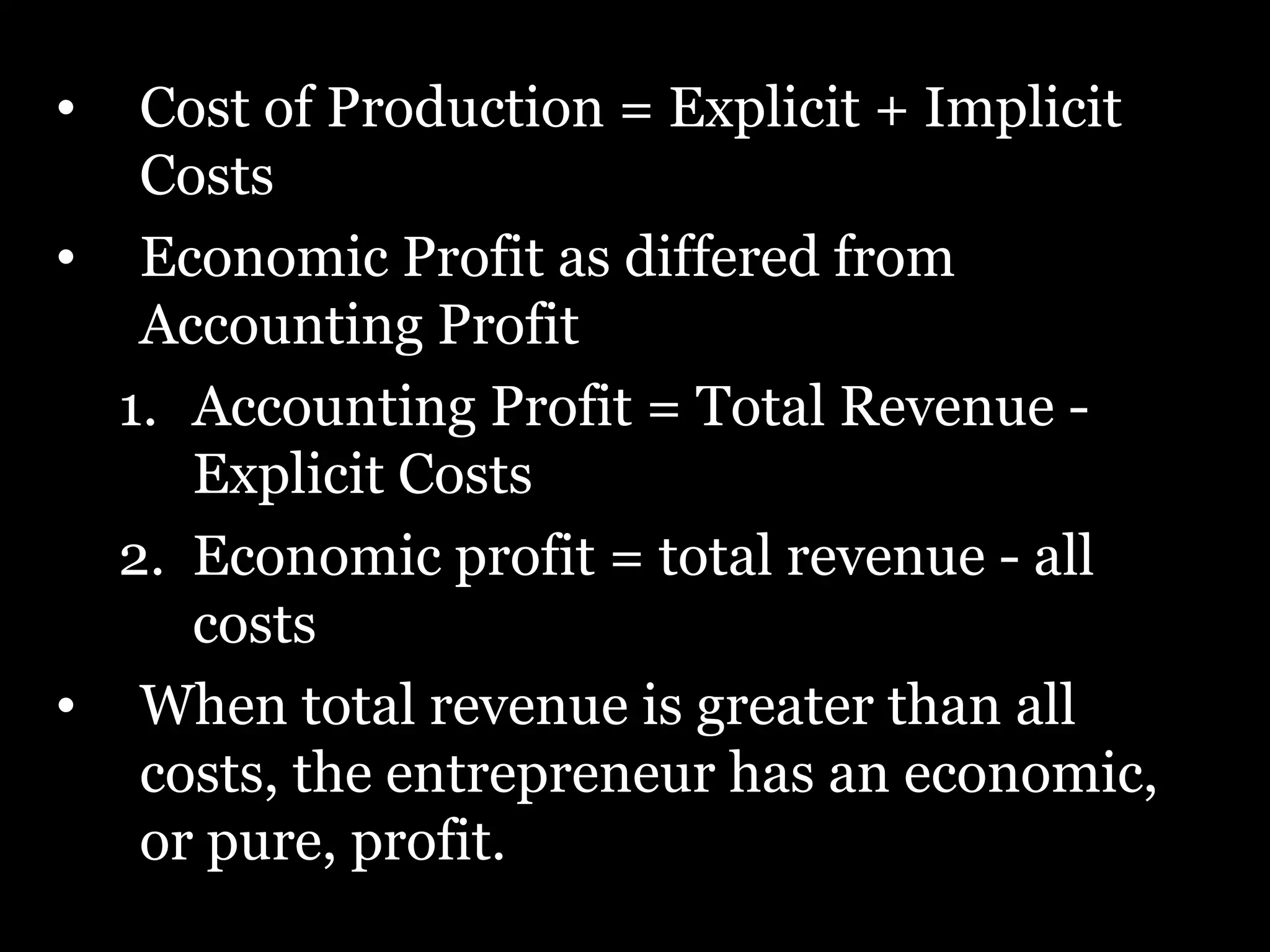

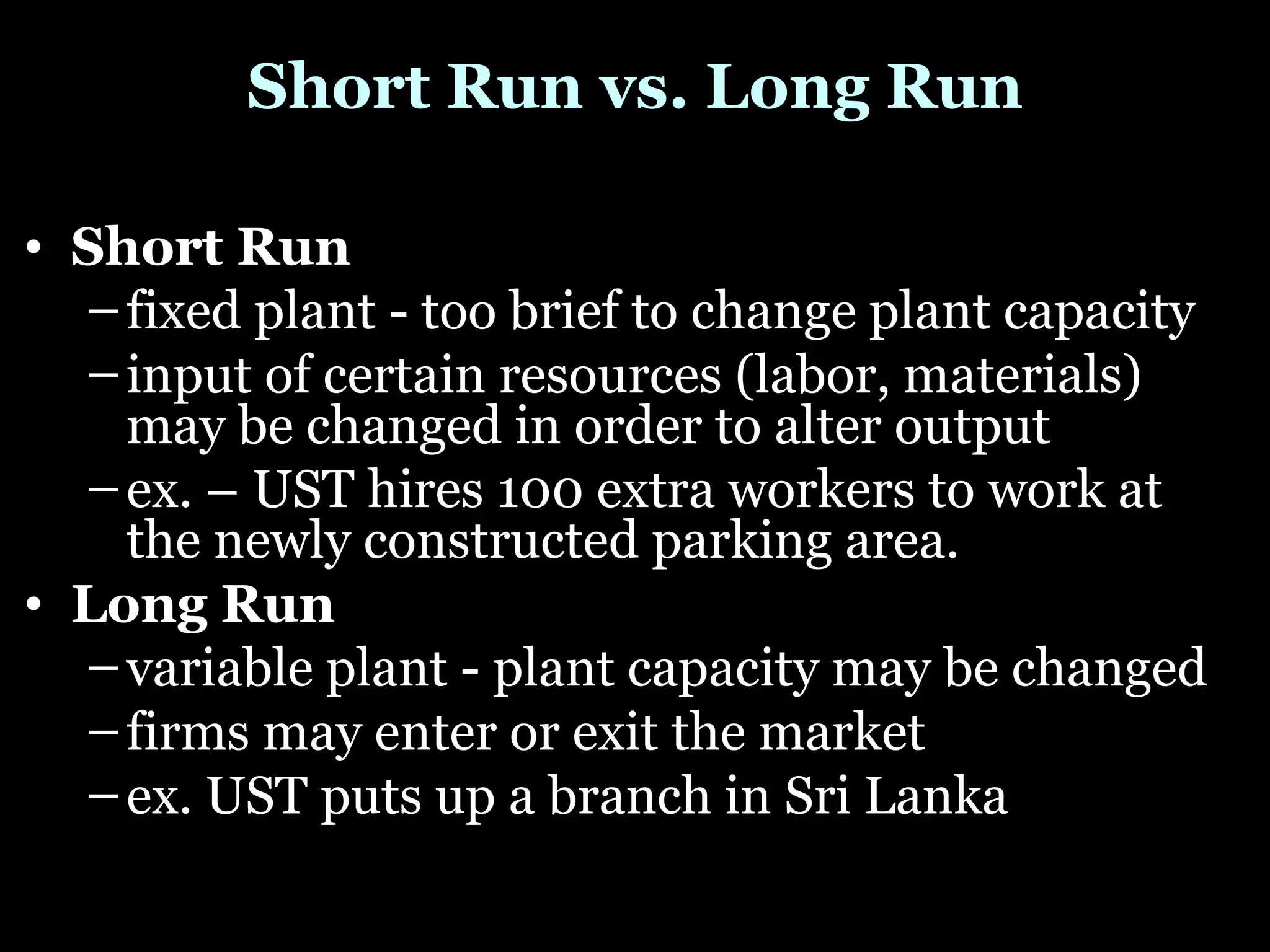

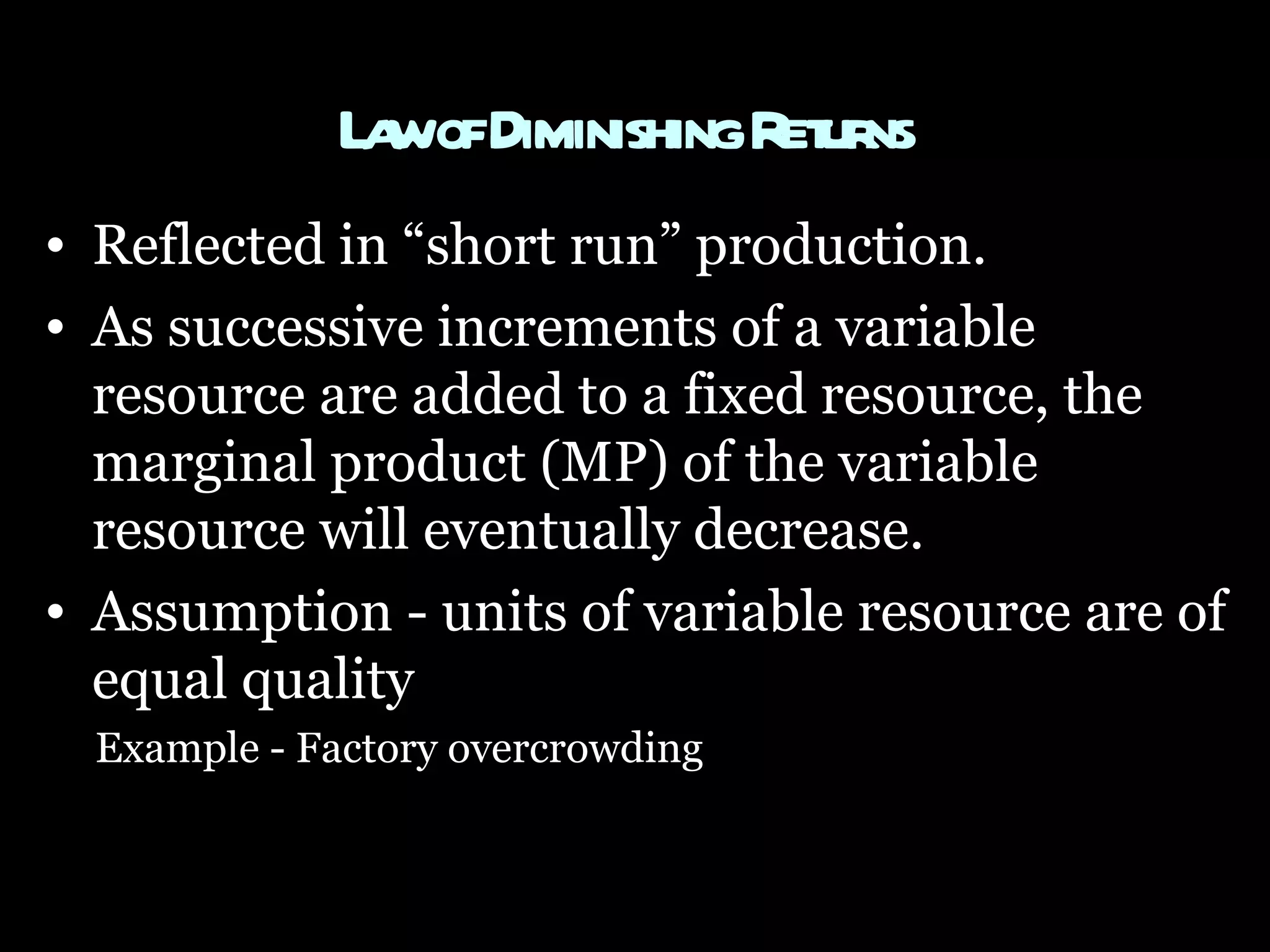

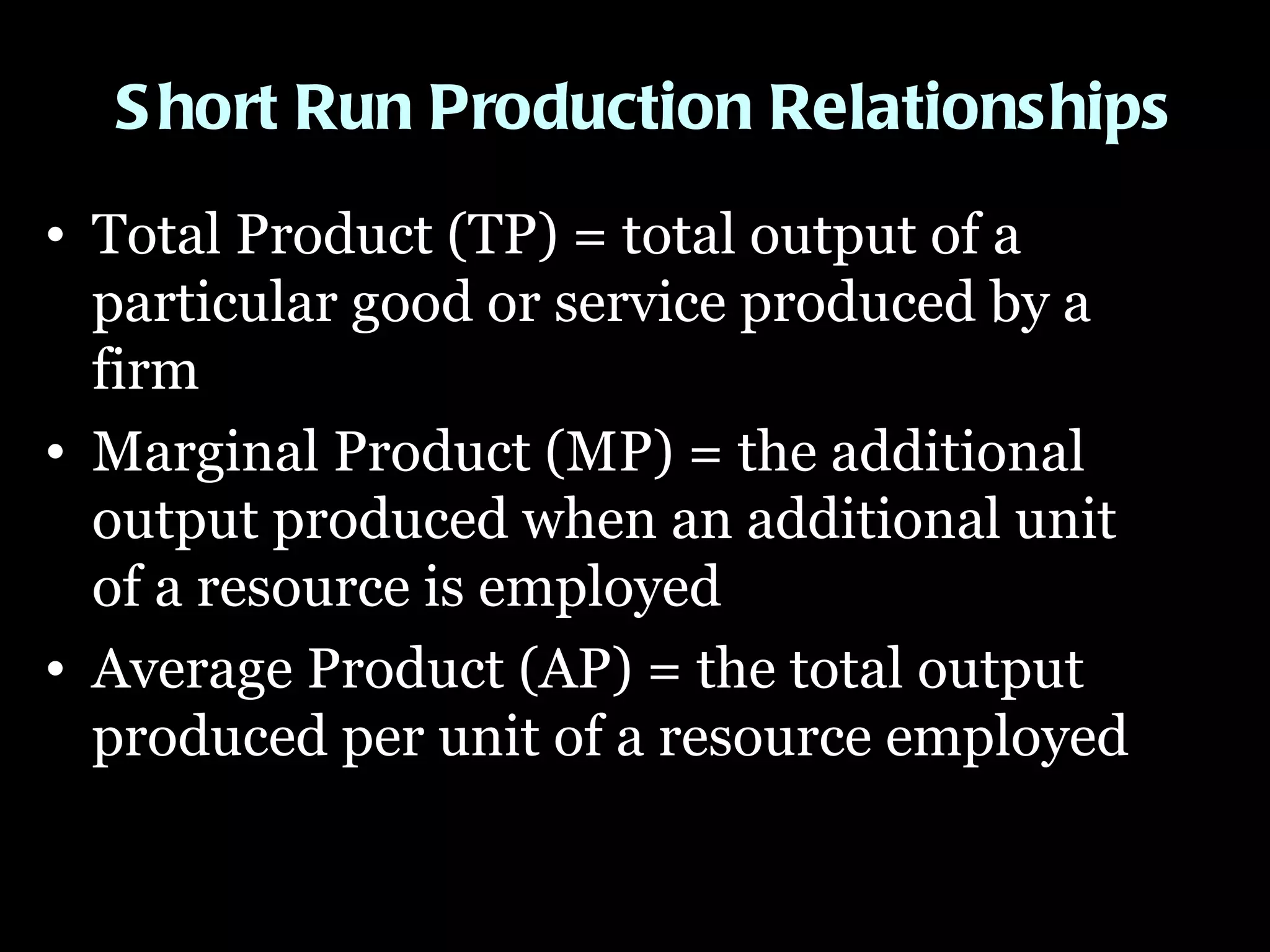

Capital goods like machines and tools are used to produce other goods. Firms acquire capital to begin, expand, or increase production. A firm's costs of production include explicit and implicit costs. Explicit costs involve direct monetary payments for resources while implicit costs do not but represent opportunities lost. The cost of production is the sum of explicit and implicit costs. Economic profit is calculated as total revenue minus all costs, while accounting profit only deducts explicit costs. In the short run a firm's capacity is fixed but variable resources can adjust, while in the long run capacity can change as firms enter and exit the market. The law of diminishing returns states that as more of a variable resource is added to a fixed resource, the marginal product