Downloaded 26 times

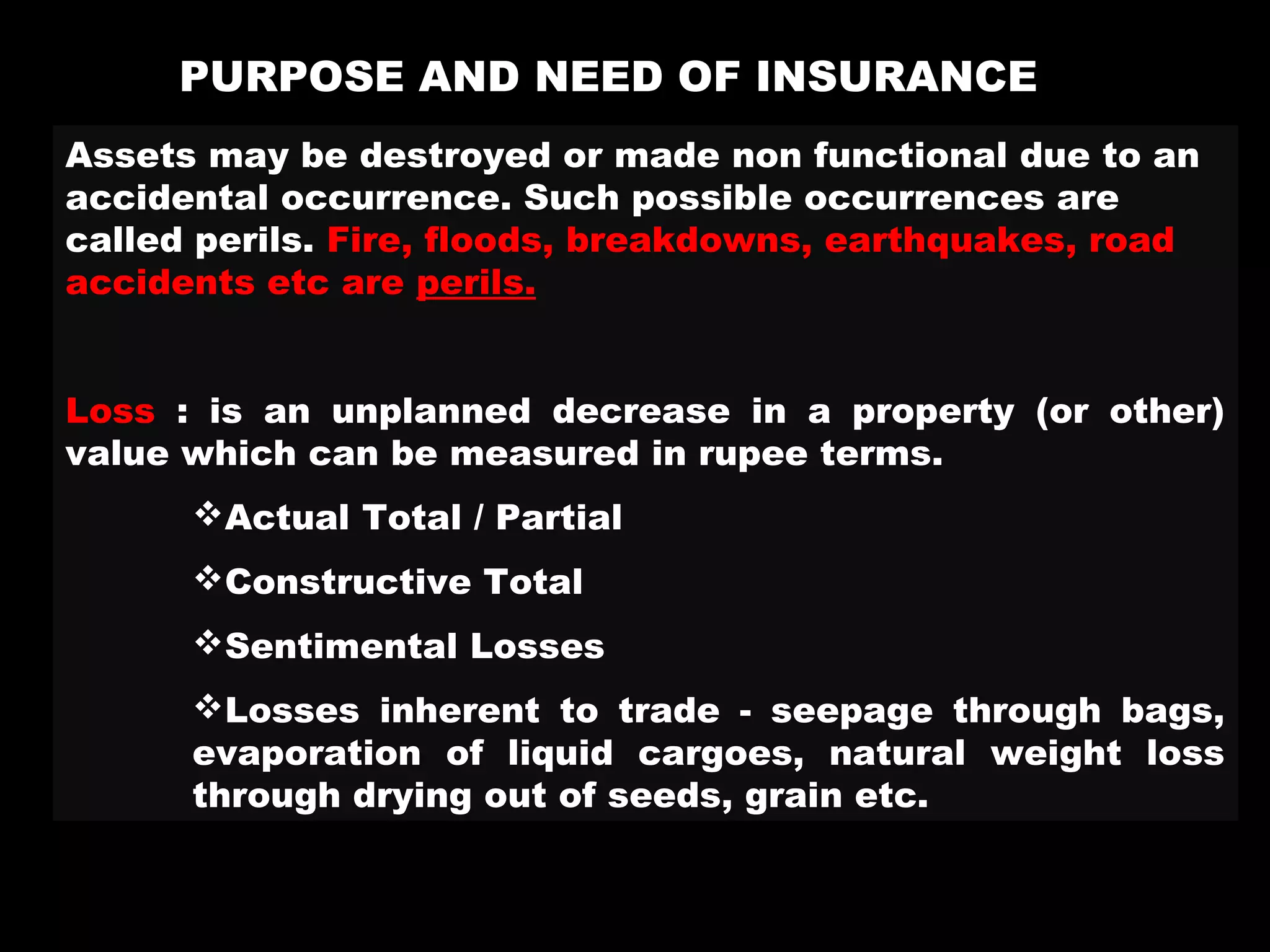

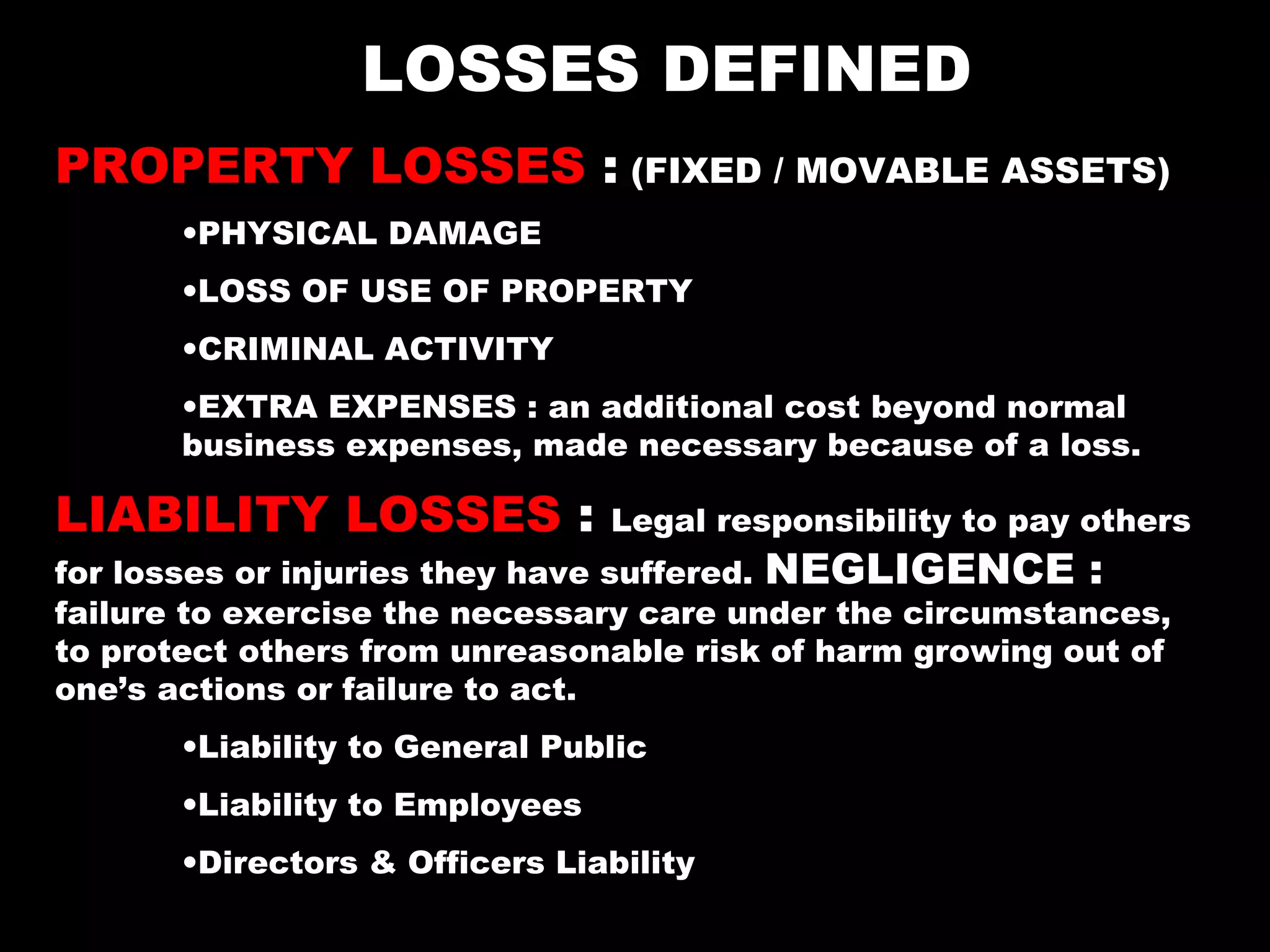

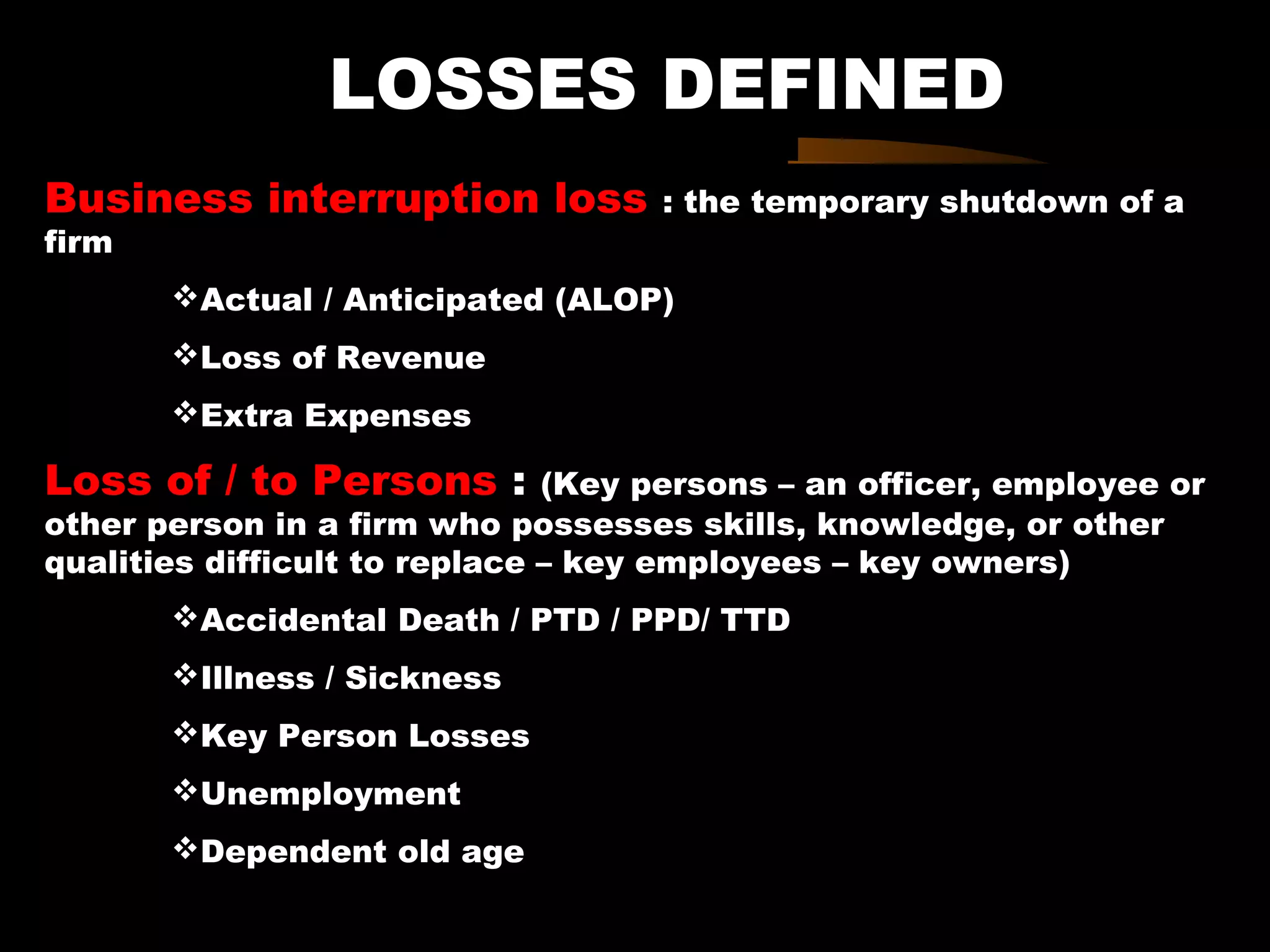

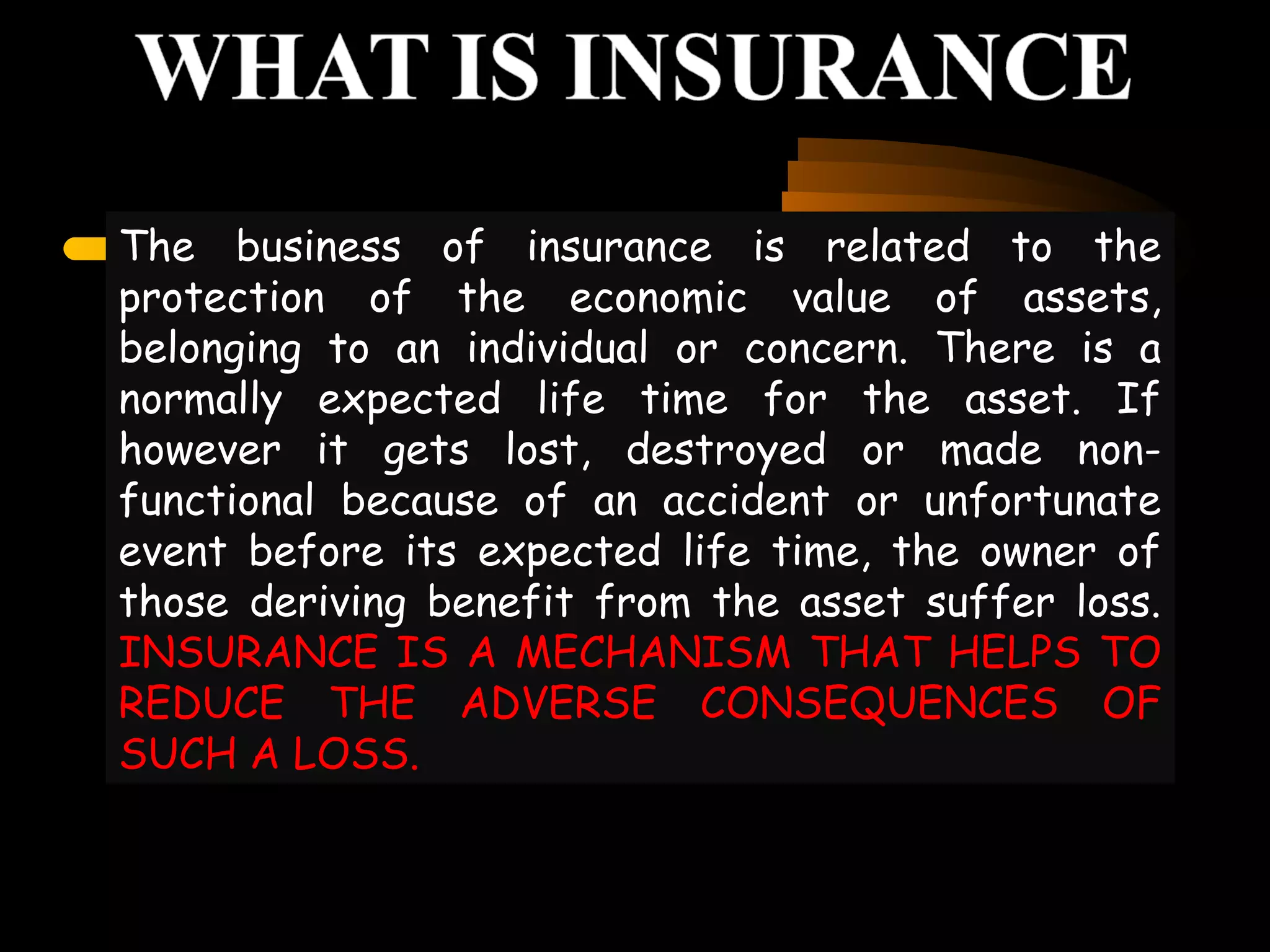

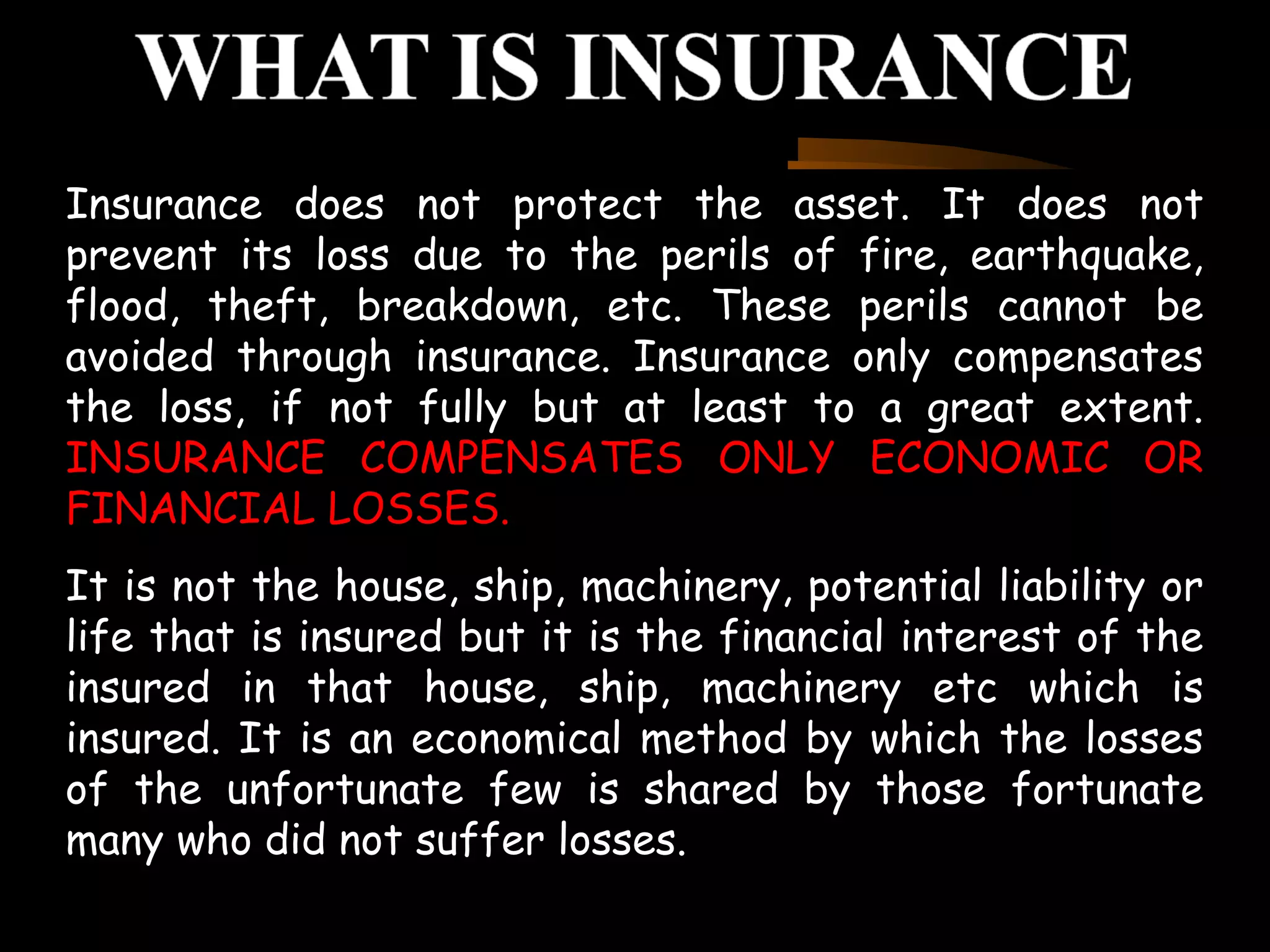

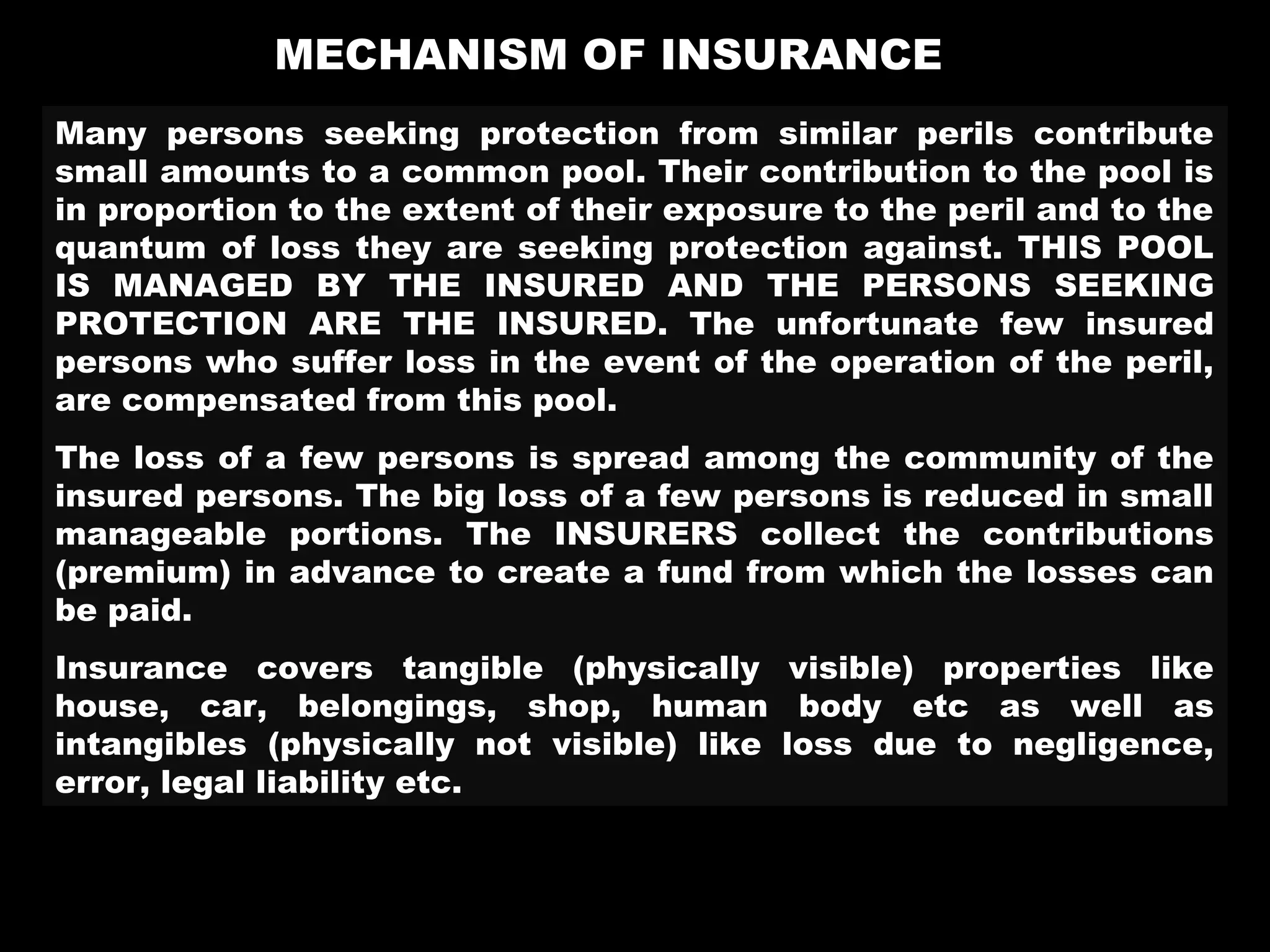

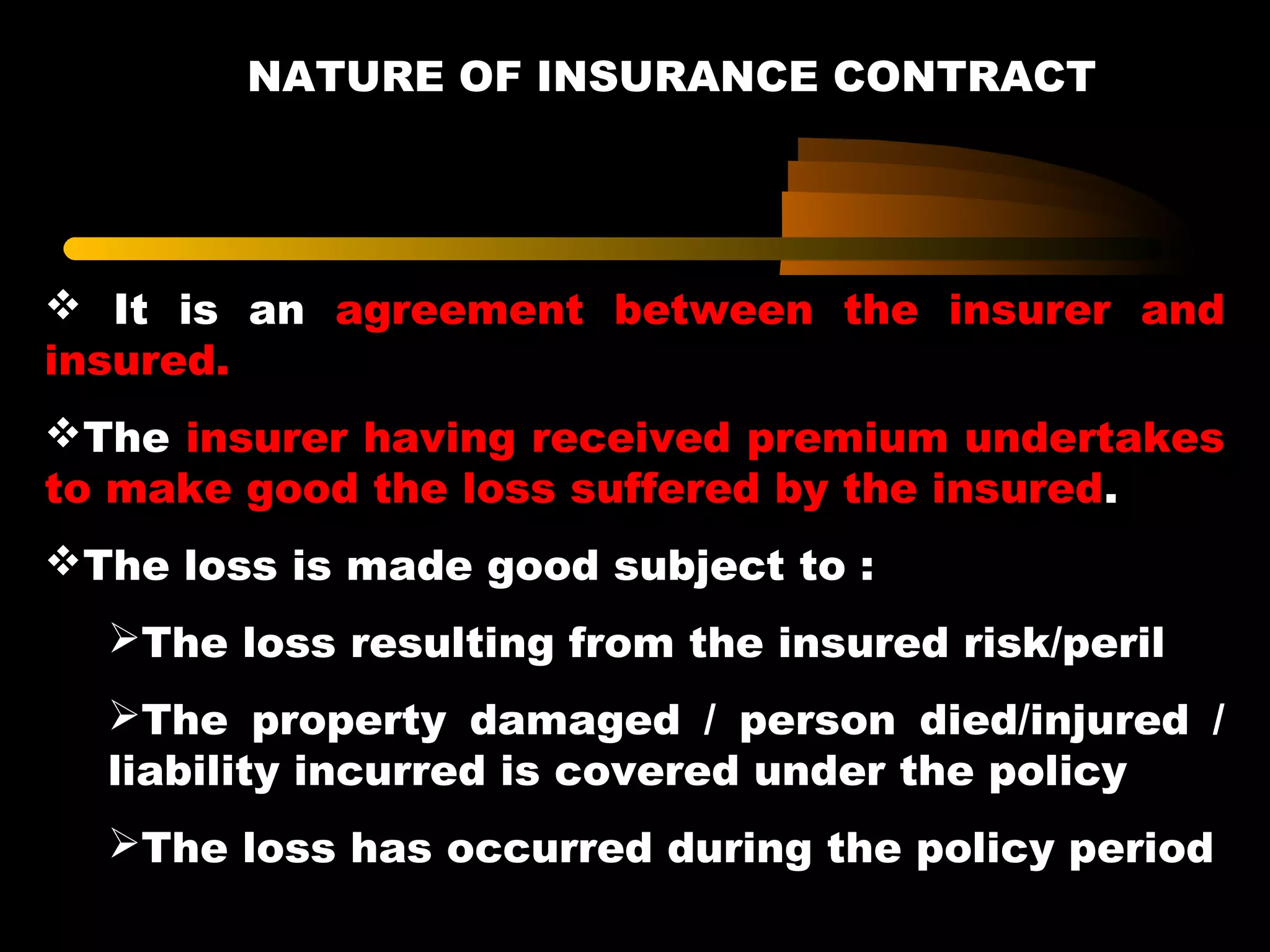

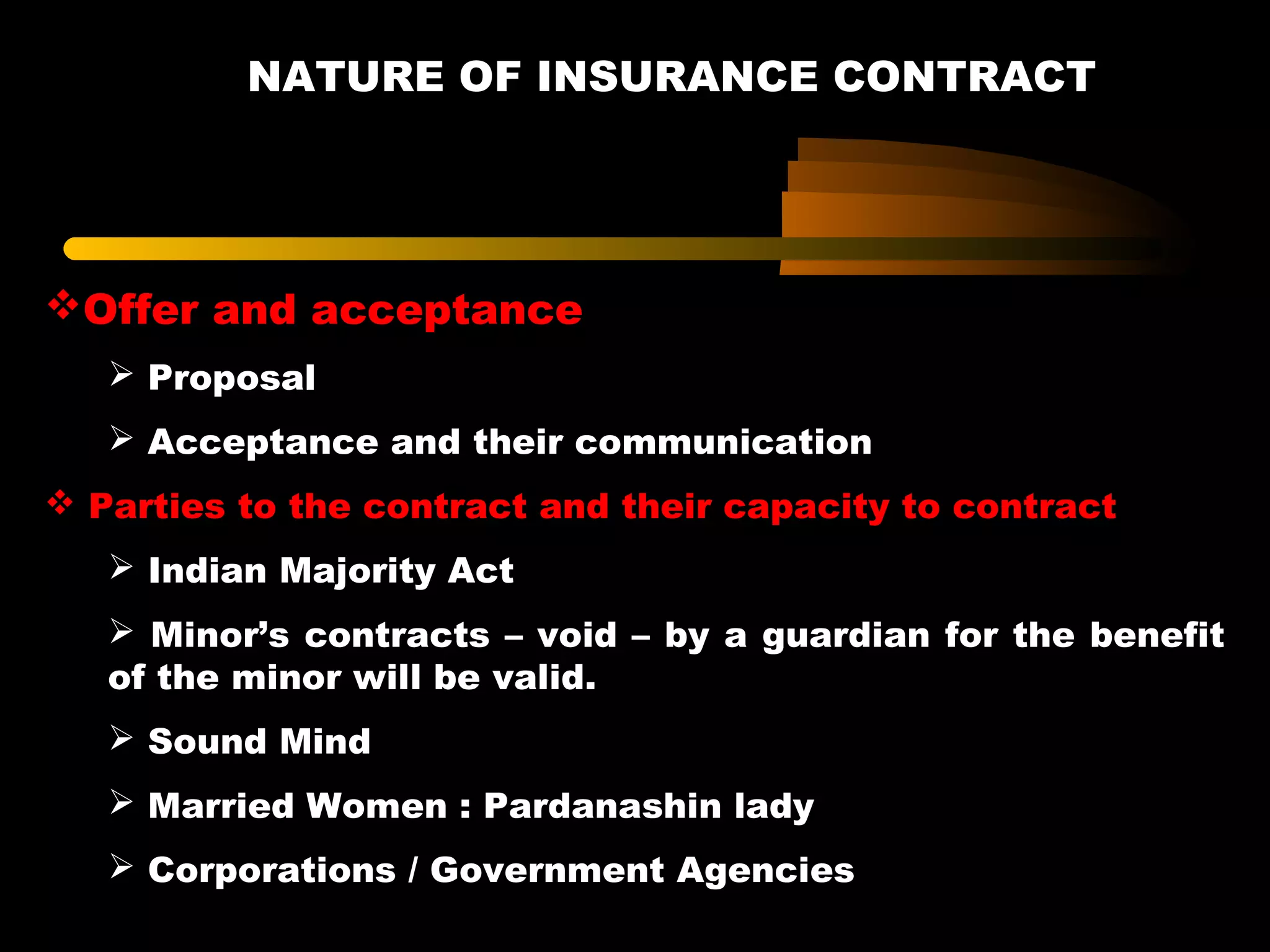

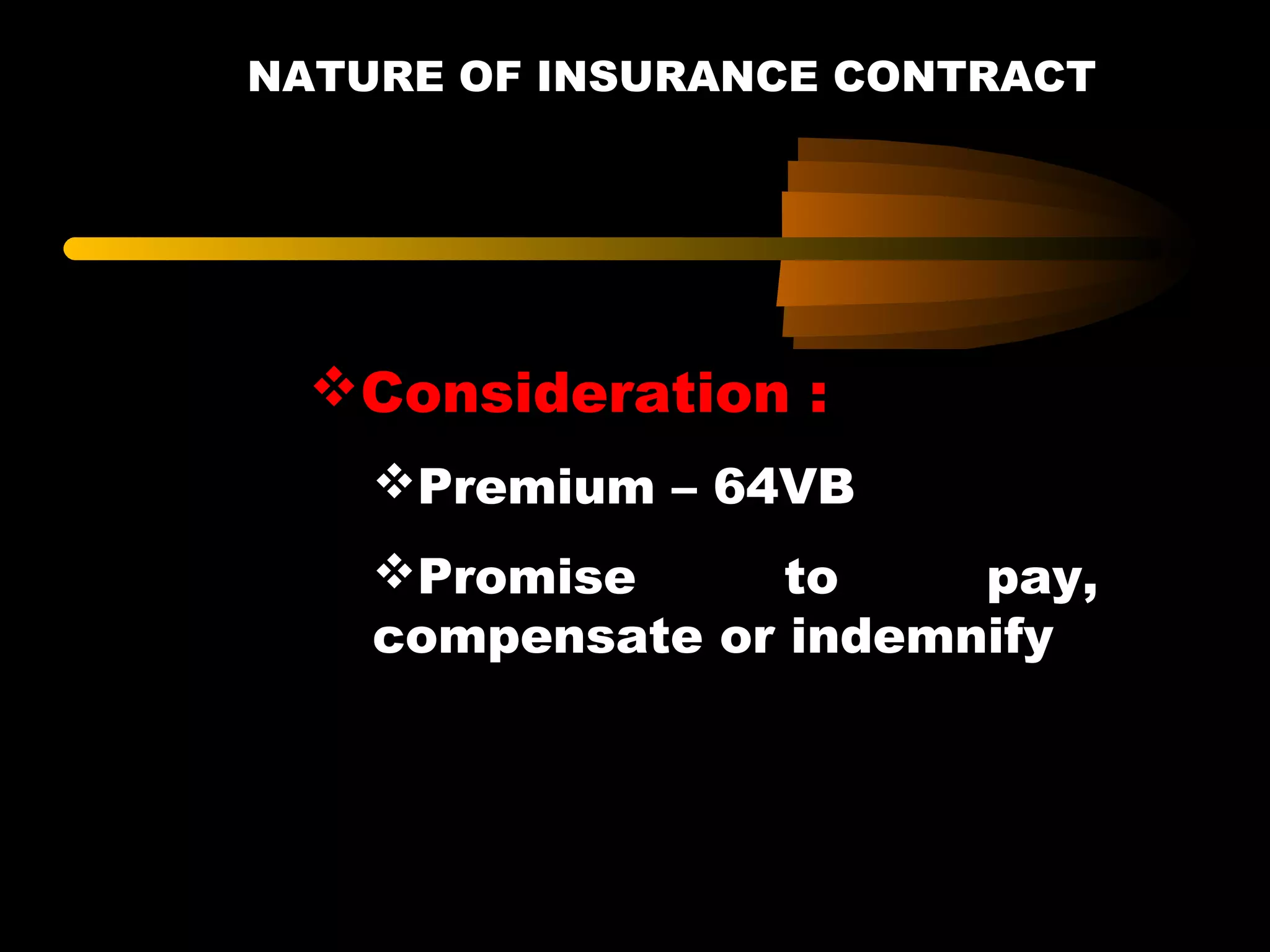

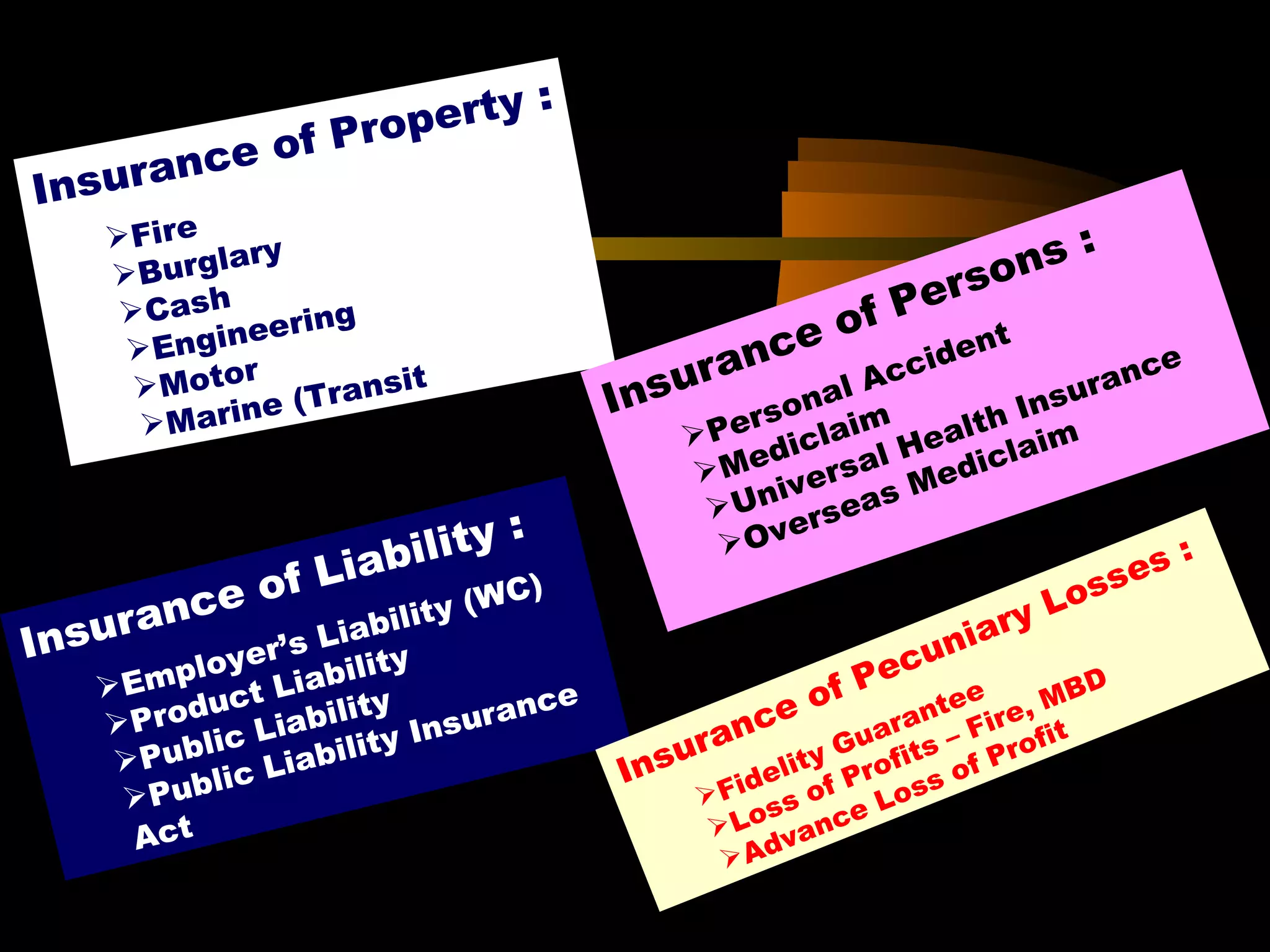

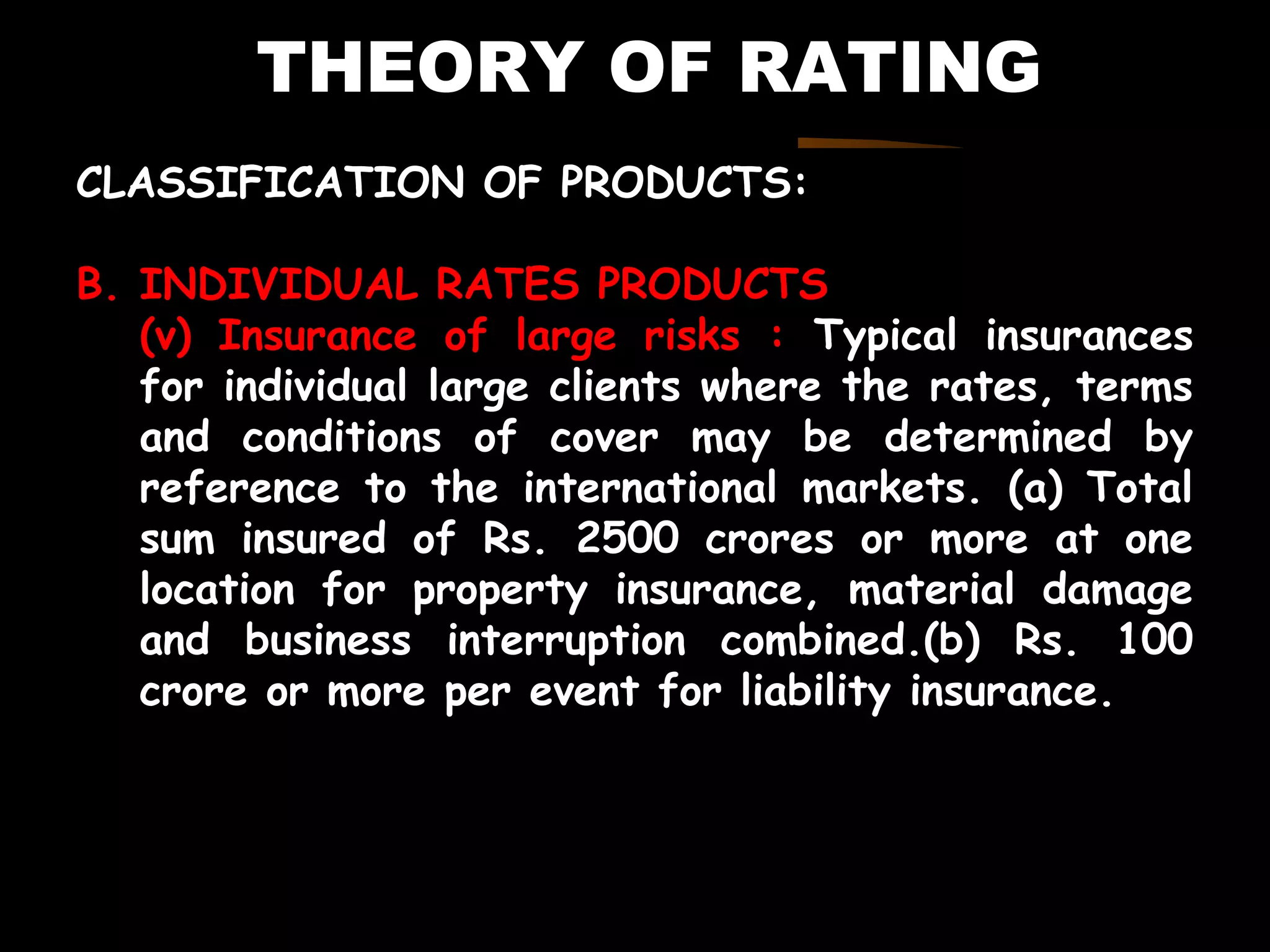

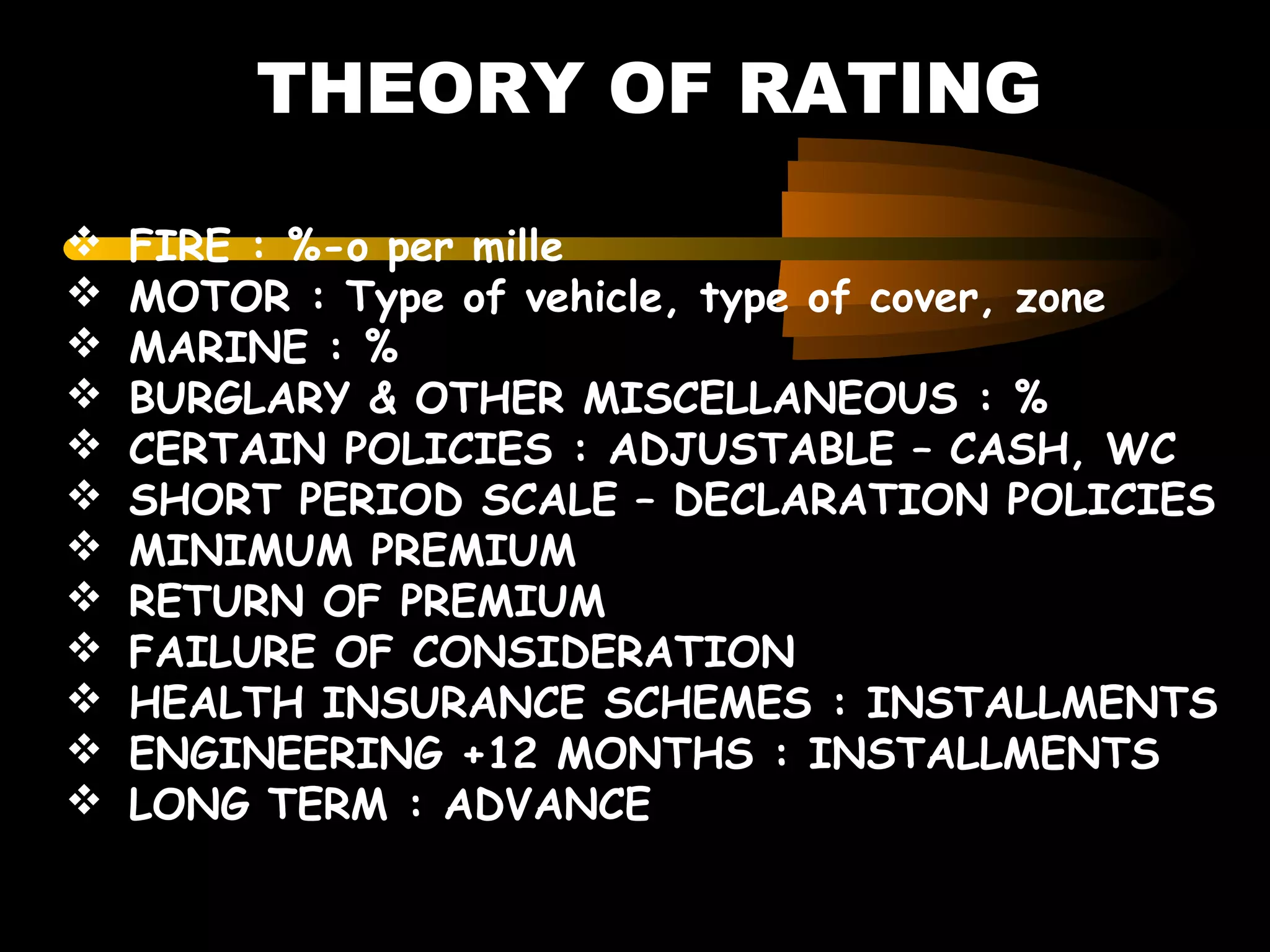

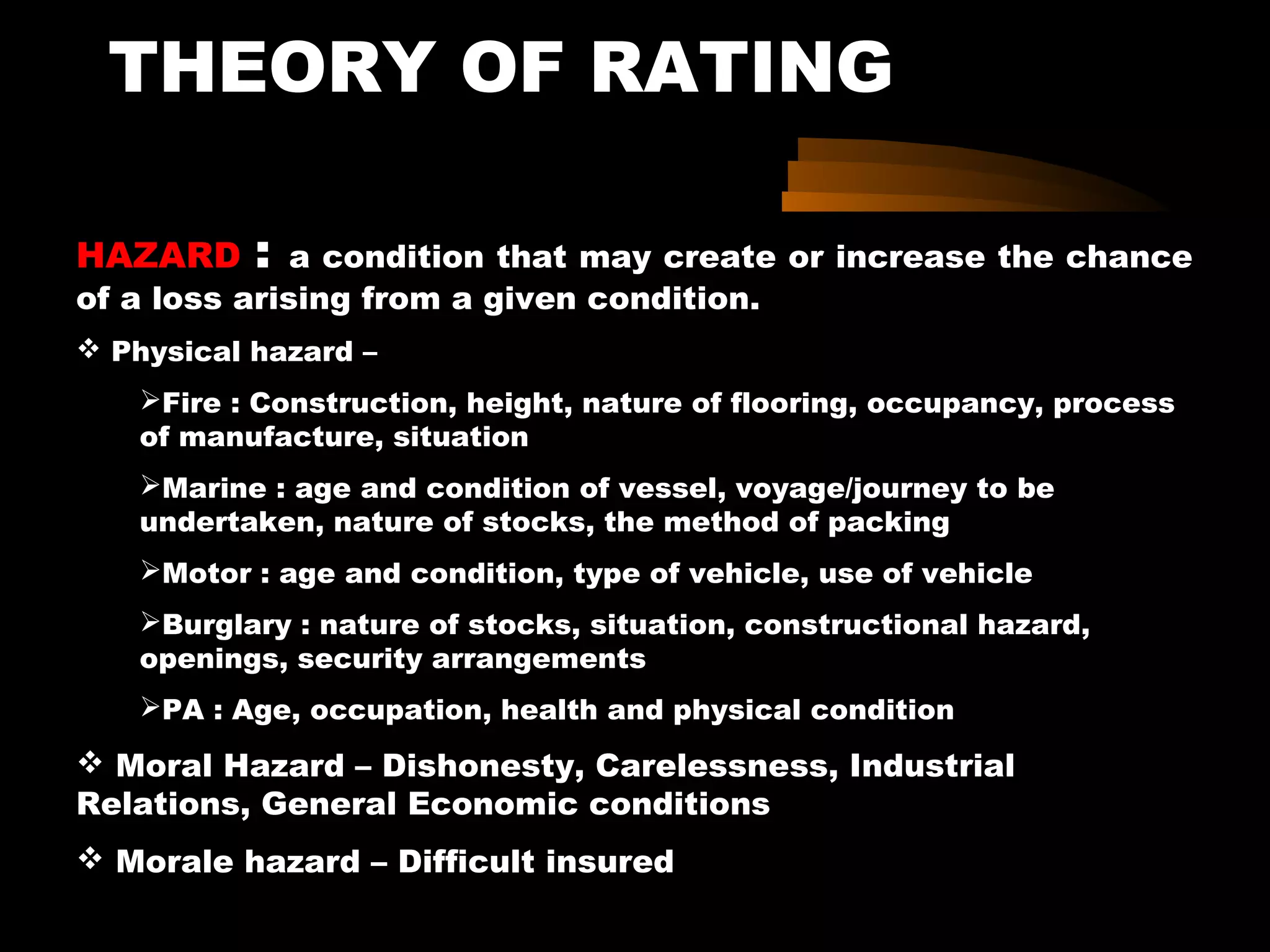

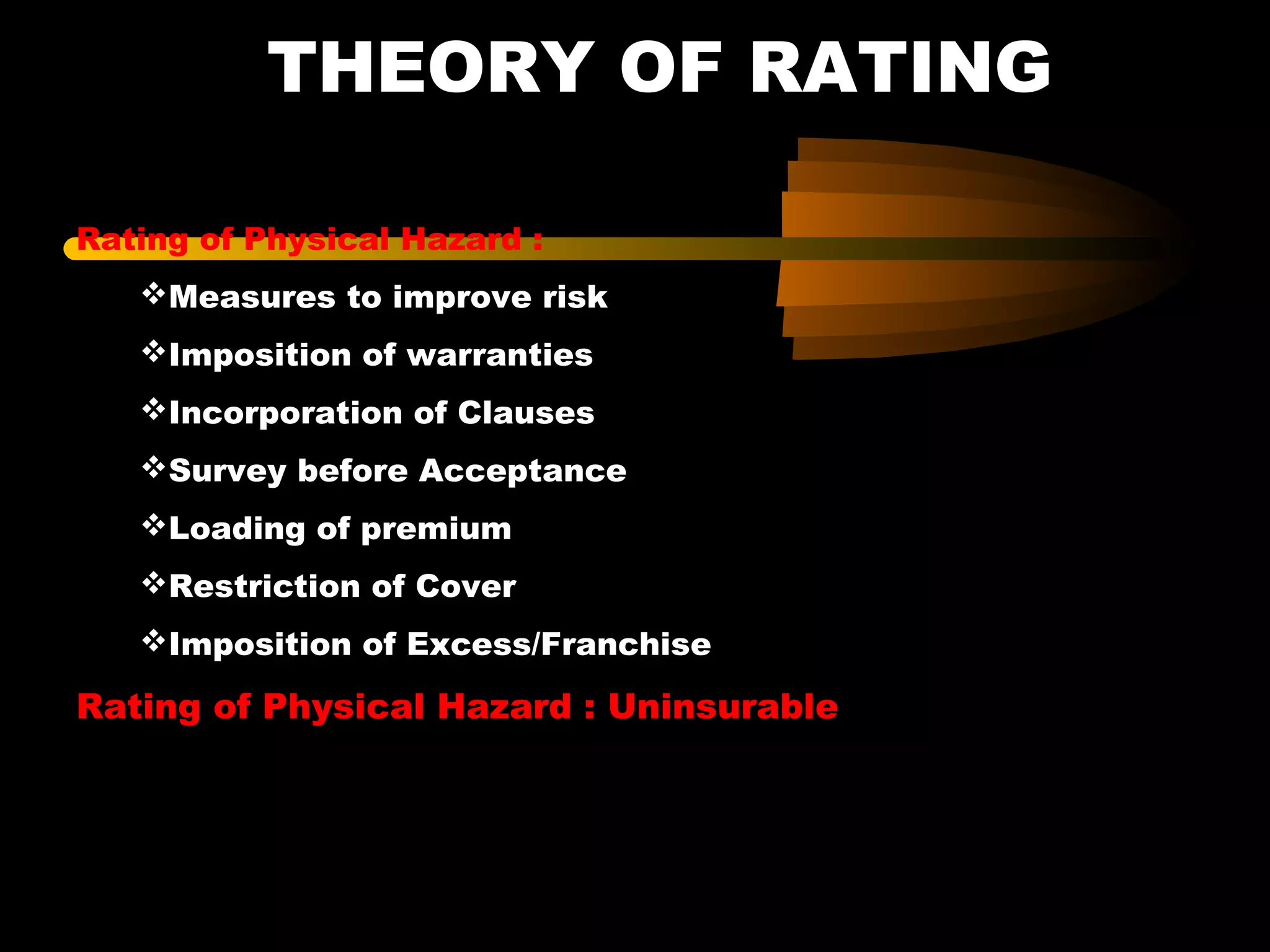

The document outlines the principles and practices of insurance, emphasizing the need for financial security against potential losses due to perils such as fire, floods, and accidents. It discusses different types of losses, including property, liability, and business interruption losses, and the importance of insurable interest and indemnity in insurance contracts. Furthermore, the document details the mechanisms of insurance, including pooling of risks, premium determination, and the classification of insurance products based on various factors.

![Chapter 1[definition and nature of insurance]](https://cdn.slidesharecdn.com/ss_thumbnails/chapter1definitionandnatureofinsurance-150912031826-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)