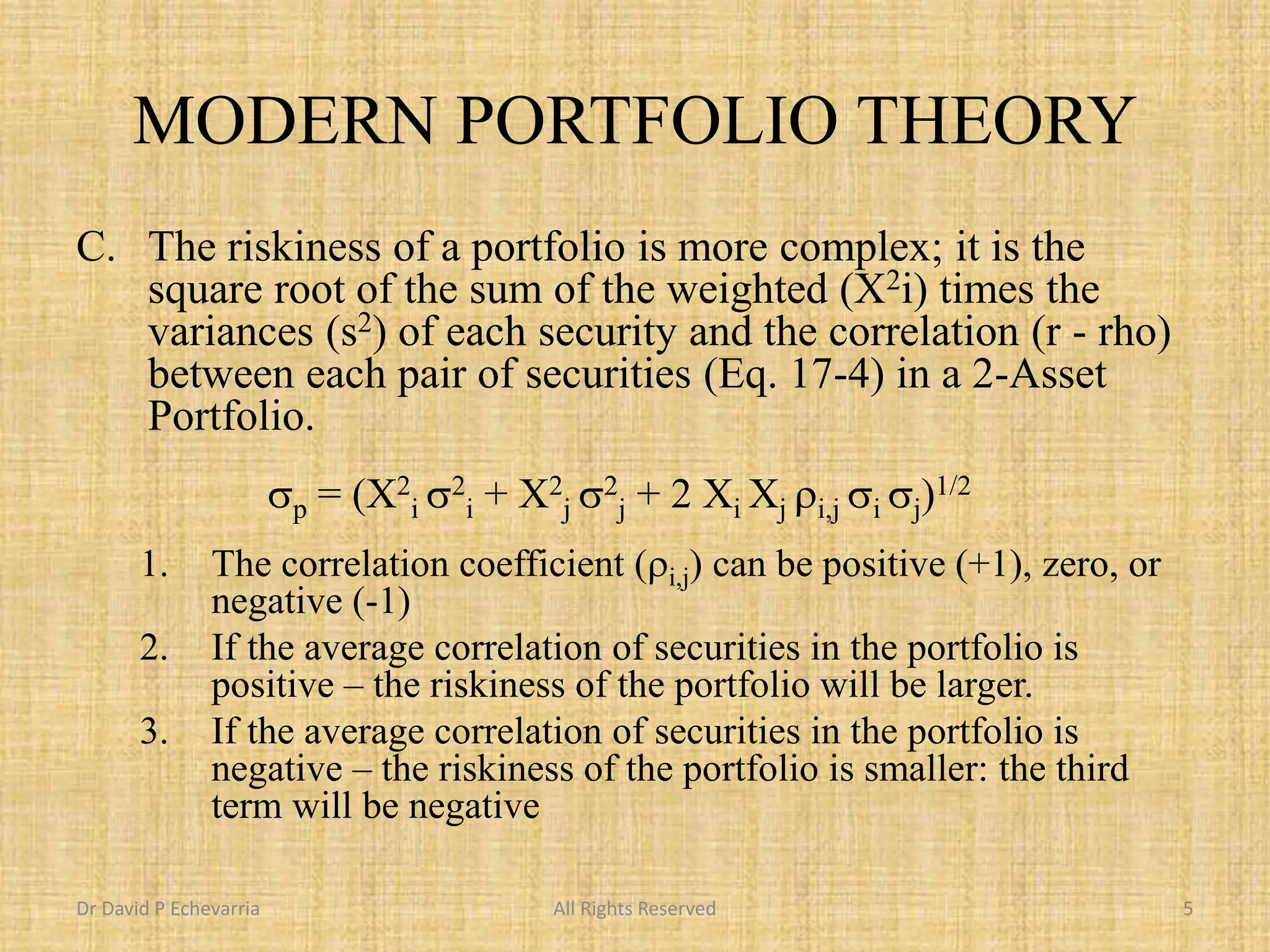

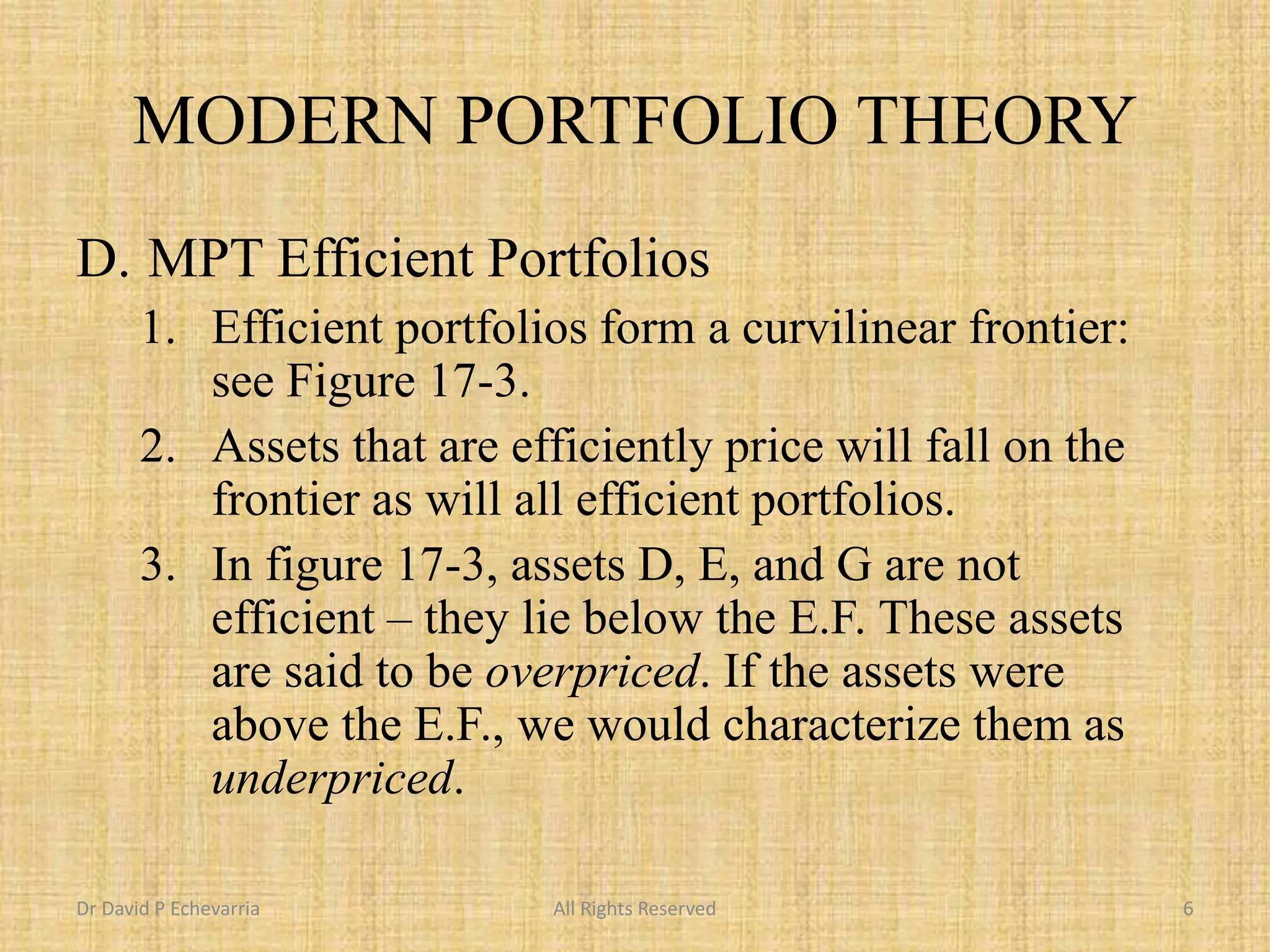

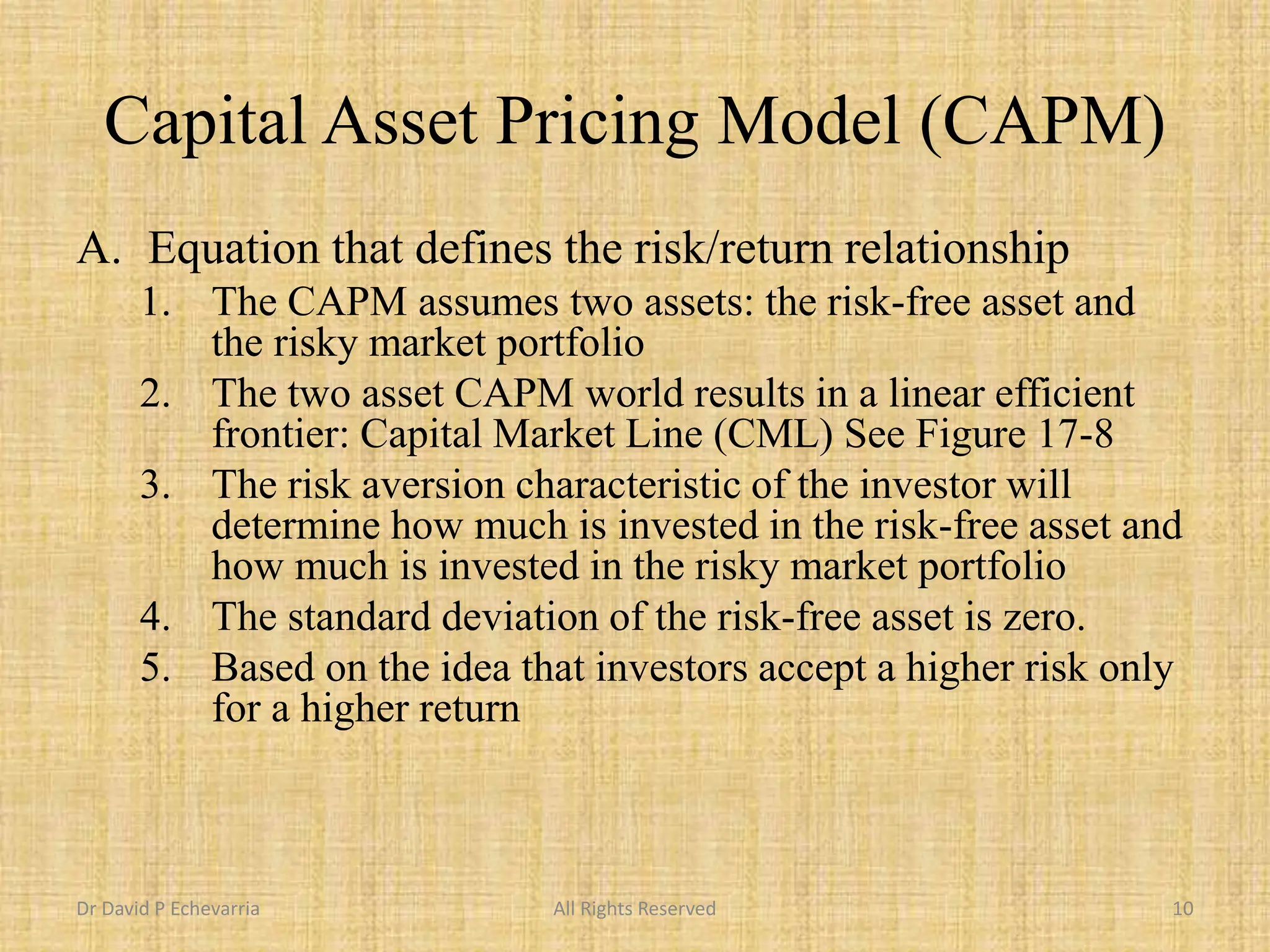

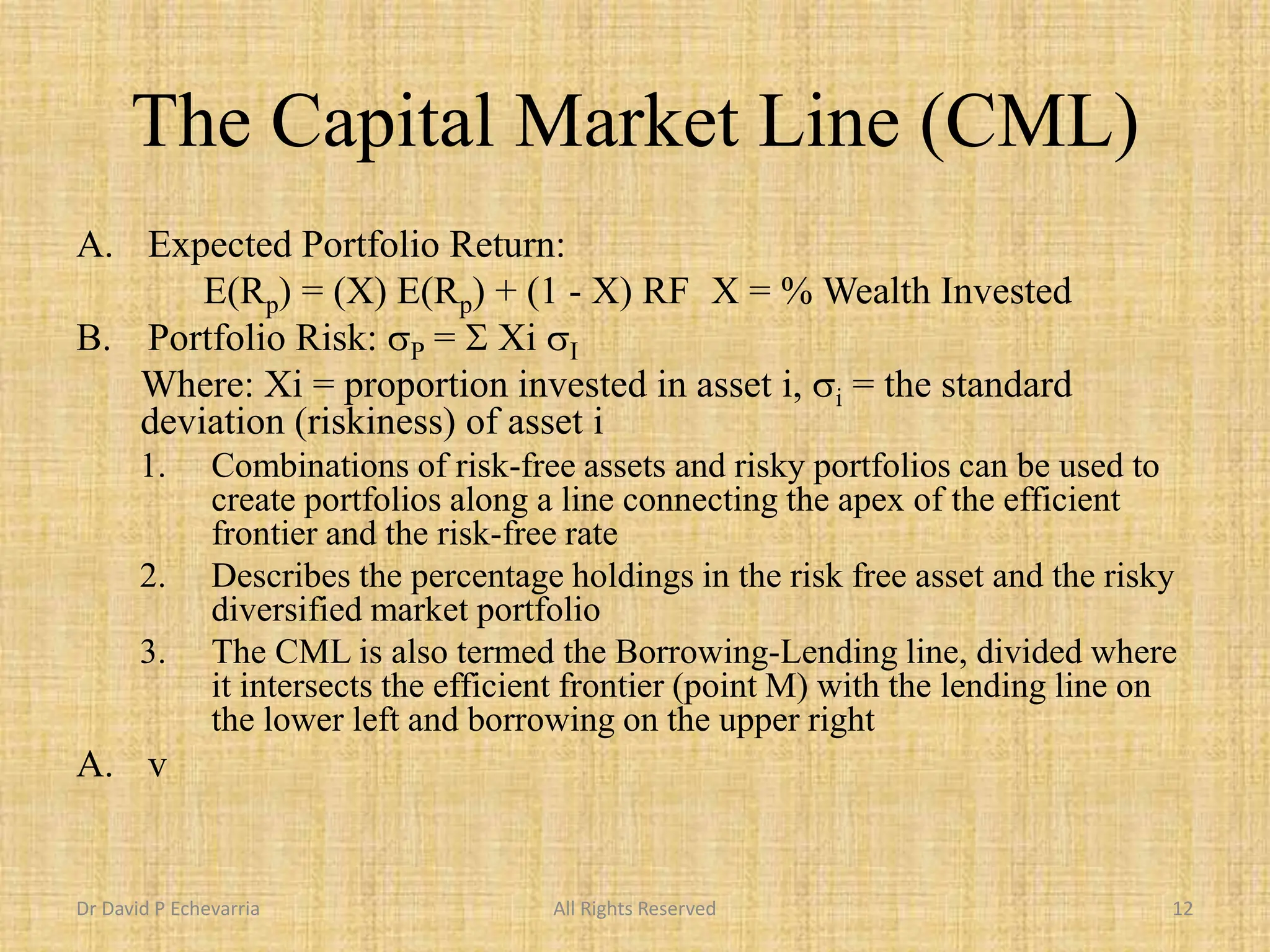

The document discusses key concepts in investing, focusing on investment risk, Modern Portfolio Theory (MPT), and the Capital Asset Pricing Model (CAPM). MPT explains how portfolios can be optimized for risk and return through diversification, while CAPM establishes the relationship between risk and expected return. It also introduces the Fama and French three-factor model and Arbitrage Pricing Theory (APT), emphasizing the importance of market efficiencies and factors influencing asset returns.

![MODERN PORTFOLIO THEORY (H.

MARKOWITZ)

A. The expected return of a portfolio is a

weighted average of the expected returns of

each of the securities in the portfolio

E(Rp) = S Xi Ri

B. The weights (Xi) are equal to the percentage

of the portfolio’s value which is invested in

each security and Ri is the [expected] return

for each asset i in the portfolio.

Dr David P Echevarria All Rights Reserved 4](https://image.slidesharecdn.com/fin330chapter17-240703072428-2a393942/75/Principal-of-investment-and-Portfolio-Management-4-2048.jpg)