Presentation Mudarabah And Agency Costs

•

5 likes•2,154 views

Just a quick presentation about the impact of agency cost and information asymmetry on PLS contracts.

Report

Share

Report

Share

![Mudarabah Contract and Musharakah Contract in Comparison ,[object Object],Musharakah Contract (profit & loss sharing) ,[object Object],[object Object],Mudarabah Contract (profit sharing) Source of Investment Profit/ Loss Sharing Management ,[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],Ownership 1 2 3 4 1 2 3 4](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recommended

Sukuk

The document discusses Sukuk, an Islamic financial certificate that is an alternative to conventional bonds. Sukuk are asset-backed and represent partial ownership of an asset, rather than debt. They can be structured using various Islamic financing contracts like murabahah, ijara, musharakah, and mudharabah. Malaysia has been a pioneer in developing the Sukuk market, with the first issuance in 1990 and the establishment of regulatory standards. It remains one of the largest Sukuk issuing countries globally.

Risk management in islamic banking

This document discusses risk management in Islamic banking. It defines risk and risk management, noting they are the same concepts as in conventional banks but with some unique aspects for Islamic banks. Generic risks include operational, credit, market, and liquidity risk, while unique risks are Shariah non-compliance, rate of return, displaced commercial, and equity investment risk. The document stresses Islamic banks need formal risk management frameworks to identify, measure, and control risks. It dispels myths that Islamic banks are not exposed to risks like interest rates and can use financial instruments to transfer some risks.

MURABAHAH

1) Murabahah is a sale contract where the seller discloses the cost price and profit margin to the buyer. It involves the purchase and resale of assets where the seller earns a defined profit margin.

2) The key pillars of a murabahah contract include the seller, buyer, asset being traded, price, and offer/acceptance. It must also avoid elements of riba such as uncertainty around prices.

3) Modern applications of murabahah include its use in Islamic banking for financing, treasury products, sukuk issuances, and international trade. Structures like tri-party murabahah and murabahah to the purchase order are commonly used.

Application of bay al dayn

The document discusses the sale of debt (bay' al dayn) under Islamic finance. It notes that while the sale of debt for another debt is prohibited, the sale of debt for cash to the debtor or a third party is permissible under certain conditions, such as payment being on a cash basis and the debtor confirming the debt. The document also examines various structured finance contracts used in Islamic bonds and Islamic accepted bills to facilitate the sale of debt in a Sharia-compliant manner.

Islamic Finance

The document provides an overview of Islamic finance instruments, with a focus on Murabaha. It defines Murabaha as a sale transaction where the seller discloses the cost of goods to the buyer and adds a known profit margin. The key steps of a Murabaha transaction are that the bank appoints the client as an agent to purchase goods, then the bank sells those goods to the client on a deferred payment basis at a marked-up price including the disclosed profit. Several legal documents are required to structure a Sharia-compliant Murabaha deal.

Musharakah presentation slides

The document discusses Musharakah, which is an Islamic financing structure based on profit-and-loss sharing partnership. It defines Musharakah and various types of Shirkah (partnership). It also describes how Musharakah works as a financing model, including diminishing Musharakah. The key differences between interest-based financing and Musharakah are that Musharakah shares profits and losses between partners according to contribution ratios, while interest guarantees a fixed return. The document proposes using market prices and rental data rather than interest rates to determine profit rates for Musharakah financing.

Types of Sukuk

There are several types of sukuk discussed in the document. Istisna'a sukuk involve project financing where funds are advanced for supplies/labor and repaid from project revenues. Salam sukuk involve the purchase of commodities on a deferred delivery basis, with full payment up front. Ijarah sukuk involve the purchase of tangible assets by an SPV from an originator which are then leased back, with rental payments funding returns to sukuk holders. Mudharabah and musharakah sukuk also exist but are not described in detail. Each structure aims to comply with Shariah principles while providing financing.

ISLAMIC BOND (SUKUK)

The document provides a case study on Islamic bonds (sukuk). It begins with an introduction that explains how sukuk developed and the key differences between sukuk and conventional bonds. The body then outlines the steps and procedures for issuing sukuk, including establishing a special purpose vehicle to hold the underlying assets. It describes the characteristics of sukuk, such as bondholders having ownership of enterprise assets and receiving regular distributions. The advantages of issuing sukuk and restrictions in Malaysia are also discussed. Responsibilities of the issuing and paying agent are covered.

Recommended

Sukuk

The document discusses Sukuk, an Islamic financial certificate that is an alternative to conventional bonds. Sukuk are asset-backed and represent partial ownership of an asset, rather than debt. They can be structured using various Islamic financing contracts like murabahah, ijara, musharakah, and mudharabah. Malaysia has been a pioneer in developing the Sukuk market, with the first issuance in 1990 and the establishment of regulatory standards. It remains one of the largest Sukuk issuing countries globally.

Risk management in islamic banking

This document discusses risk management in Islamic banking. It defines risk and risk management, noting they are the same concepts as in conventional banks but with some unique aspects for Islamic banks. Generic risks include operational, credit, market, and liquidity risk, while unique risks are Shariah non-compliance, rate of return, displaced commercial, and equity investment risk. The document stresses Islamic banks need formal risk management frameworks to identify, measure, and control risks. It dispels myths that Islamic banks are not exposed to risks like interest rates and can use financial instruments to transfer some risks.

MURABAHAH

1) Murabahah is a sale contract where the seller discloses the cost price and profit margin to the buyer. It involves the purchase and resale of assets where the seller earns a defined profit margin.

2) The key pillars of a murabahah contract include the seller, buyer, asset being traded, price, and offer/acceptance. It must also avoid elements of riba such as uncertainty around prices.

3) Modern applications of murabahah include its use in Islamic banking for financing, treasury products, sukuk issuances, and international trade. Structures like tri-party murabahah and murabahah to the purchase order are commonly used.

Application of bay al dayn

The document discusses the sale of debt (bay' al dayn) under Islamic finance. It notes that while the sale of debt for another debt is prohibited, the sale of debt for cash to the debtor or a third party is permissible under certain conditions, such as payment being on a cash basis and the debtor confirming the debt. The document also examines various structured finance contracts used in Islamic bonds and Islamic accepted bills to facilitate the sale of debt in a Sharia-compliant manner.

Islamic Finance

The document provides an overview of Islamic finance instruments, with a focus on Murabaha. It defines Murabaha as a sale transaction where the seller discloses the cost of goods to the buyer and adds a known profit margin. The key steps of a Murabaha transaction are that the bank appoints the client as an agent to purchase goods, then the bank sells those goods to the client on a deferred payment basis at a marked-up price including the disclosed profit. Several legal documents are required to structure a Sharia-compliant Murabaha deal.

Musharakah presentation slides

The document discusses Musharakah, which is an Islamic financing structure based on profit-and-loss sharing partnership. It defines Musharakah and various types of Shirkah (partnership). It also describes how Musharakah works as a financing model, including diminishing Musharakah. The key differences between interest-based financing and Musharakah are that Musharakah shares profits and losses between partners according to contribution ratios, while interest guarantees a fixed return. The document proposes using market prices and rental data rather than interest rates to determine profit rates for Musharakah financing.

Types of Sukuk

There are several types of sukuk discussed in the document. Istisna'a sukuk involve project financing where funds are advanced for supplies/labor and repaid from project revenues. Salam sukuk involve the purchase of commodities on a deferred delivery basis, with full payment up front. Ijarah sukuk involve the purchase of tangible assets by an SPV from an originator which are then leased back, with rental payments funding returns to sukuk holders. Mudharabah and musharakah sukuk also exist but are not described in detail. Each structure aims to comply with Shariah principles while providing financing.

ISLAMIC BOND (SUKUK)

The document provides a case study on Islamic bonds (sukuk). It begins with an introduction that explains how sukuk developed and the key differences between sukuk and conventional bonds. The body then outlines the steps and procedures for issuing sukuk, including establishing a special purpose vehicle to hold the underlying assets. It describes the characteristics of sukuk, such as bondholders having ownership of enterprise assets and receiving regular distributions. The advantages of issuing sukuk and restrictions in Malaysia are also discussed. Responsibilities of the issuing and paying agent are covered.

Operational Risk

Operational risk in Islamic finance can arise from a variety of sources. The document identifies six main categories of operational risk: 1) Shariah non-compliance risk, 2) people risk, 3) technology risk, 4) fiduciary risk, 5) legal risk, and 6) reputational risk. It also discusses the nature of operational risks as either internally or externally inflicted, the impacts as direct or indirect, and the degree of expectancy as expected or unexpected losses. Proper identification and management of operational risks are important for Islamic financial institutions.

Islamic banking by G.Reka

This document provides an overview of Islamic banking including its meaning, principles, deposits, differences from conventional banking, benefits, issues and a SWOT analysis. The key points are:

- Islamic banking complies with Sharia law and prohibits interest, requiring profit and loss sharing. It aims to achieve socially and financially acceptable objectives.

- The basic principles are sharing of profit and loss, prohibiting investment in unlawful businesses and interest. Deposits include savings, current and investment accounts.

- It differs from conventional banking in its basis in Islamic principles, risk sharing approach, and status as partners rather than creditors/debtors.

- Benefits include inclusive economic growth, availability of funds, and protection from

Bba2

The document discusses the issue of Bai Bithaman Ajil (BBA) contracts as used in Islamic financing in Malaysia. It summarizes the conceptual model of BBA, which involves the deferred payment sale of an asset from a seller to a purchaser. The document then discusses 5 previous court cases related to BBA and the legal issues they raised. The cases analyzed whether the BBA structure qualified as a legitimate sale contract under Shariah or resembled interest-based financing. The document concludes by noting the Malaysian government strengthened regulations on Islamic finance to address legal uncertainties surrounding BBA raised by the court cases.

Murabaha finance

This document provides an overview of Murabaha finance, which is a particular type of sale in Islamic finance where the seller discloses the cost of purchasing an asset and sells it to the buyer at a higher price to generate a profit. The document defines Murabaha and explains its key features and components. It also outlines three common models for structuring Murabaha transactions, with Model III involving banks as the most prevalent in modern Islamic banking. Model III is explained in further detail through its typical phases and documentation requirements.

Murabaha mbl

This document provides an introduction and overview of Murabaha, an Islamic financing structure. It defines Murabaha as a sale where the seller discloses the cost of goods to the buyer and adds a known profit. The key features are that the asset being sold must exist, the sale price must be determined, and the sale must be unconditional. It then outlines the basic 6 step process for Murabaha financing between a bank and client, where the client acts as an agent to purchase goods on the bank's behalf that are then sold to the client. Finally, it lists some common applications of Murabaha for meeting working capital needs, long-term purchases, and trade finance.

bai as-salam and istisna

1. Bai As-Salam refers to a contract where advance cash payment is made for goods to be delivered later. The seller undertakes to supply specific goods to the buyer at a future date in exchange for the advanced price paid in full.

2. Salam transactions require full payment of the purchase price at the time of sale. This ensures the seller has the liquidity expected and the basic purpose of the transaction is not defeated.

3. Parallel or back-to-back salam involves three parties, where one party enters into two consecutive salam contracts to manage risks from price fluctuations between the contracts.

Risk Management Process in Islamic Banks

Risk management is a vital process for Islamic banks that consists of several interconnected phases. It includes establishing a risk management framework based on ISO 31000:2009, identifying risks through analysis of products and activities, measuring risks using a composite risk index, developing a risk matrix to plot risks by severity and impact, reviewing risks and monitoring actual risk levels. Effective risk management also requires infrastructure like documentation of policies, an organizational structure with risk management committees, use of information technology systems and databases, and selecting appropriate risk measurement models. The goal is to properly manage both generic financial risks and unique risks to Islamic banks like Sharia non-compliance, displaced commercial, and equity investment risks.

BAY' BITHAMAN AAJIL

The document discusses the concept of Bai Bithaman Ajil (BBA), which is an Islamic financing technique that allows for the deferred payment of goods purchased. BBA involves the immediate delivery of an asset to the buyer while payment is postponed to a future date or paid through installments. The document examines the principles, evidence, objectives, mechanics, and pricing considerations of BBA transactions.

chapter 6 islamic banking 2

The document discusses various Islamic financial instruments used in Malaysia. It describes instruments like Mudharabah, Musharakah, Murabahah, Ijarah, and Wakalah. It explains how these instruments work, including the rights and responsibilities of parties in each contract. Shariah committees provide oversight to ensure Islamic banks operate according to Shariah principles.

Risk management in islamic banking

This document discusses risk management in Islamic banking. It begins with definitions of risk management and describes the risk management process. It then outlines the major risks faced by both Islamic and conventional banks, as well as unique risks faced only by Islamic banks. The document discusses the Shariah perspective on risk, as well as tools for risk mitigation and measurement. It provides guidance principles from Basel, IFSB, and other organizations and discusses challenges in capturing unique risks of Islamic banking. It concludes with ten rules of risk management and a word of caution about managing risks in life.

Salam

The document discusses Salam, a type of Islamic financing contract. Some key points:

1. In a Salam contract, the seller undertakes to supply specific goods to the buyer at a future date in exchange for full payment of the price at the time of the contract.

2. Several conditions must be met for a Salam contract to be valid, including full advance payment, precise specification of goods, and setting an exact date and place of delivery.

3. Salam can help finance agricultural sectors by allowing farmers to receive funds upfront before harvest in exchange for committing to future delivery of crops. Banks can use parallel Salam contracts to mitigate delivery risk.

Topic v. islamic bonds sukuk

This document discusses Islamic bonds (sukuk). It begins by defining sukuk and explaining their historical origins. Sukuk are asset-backed financial certificates that represent ownership in the underlying assets. The document then discusses how sukuk are structured, focusing on the most common types - mudarabah, musharakah and ijarah sukuk. It explains the standards from AAOIFI and the process for structuring each type of sukuk. The document concludes by discussing ratings of Islamic bonds, differentiating between sovereign and corporate ratings and the methodology used.

Ijarah

This clause makes the Ijarah contract invalid because selling of the asset cannot be contingent upon fulfilling the terms of the Ijarah contract. Under Islamic finance principles, the lease and sale contracts must be separate, with the sale not being an automatic outcome of fulfilling the lease terms.

Bay al dayn

Bay al-dayn refers to the sale of debt in Islamic finance. It involves the sale and purchase of a quality debt, either to the debtor or a third party. There are differing views among Islamic scholars on whether debt can be sold to a third party. Proponents argue it can be allowed subject to certain conditions to avoid risks like gharar. Critics argue the sale of debt to non-debtors is prohibited due to issues like selling something one does not possess.

Ijarah INTRODUCTION

Ijarah is an Islamic financing method where a lessor leases an asset to a lessee for an agreed upon rental payment. There are three key points:

1) Ijarah allows the use of an asset but ownership remains with the lessor, who bears risks related to ownership. The lessee bears risks related to use of the asset.

2) Rental payments and sale of the asset must be structured separately to avoid making the lease contingent on sale.

3) Rules governing ijarah require the asset to be identified and the lease period determined. Rent can be set ahead of time but not increased unilaterally. The lessee bears costs of use while the lessor

Morabaha Financing

The word Morabaha is taken from the Arabic word Ribh which means Profit. Originally, Morabaha is a contract of sale in which a commodity is sold on profit. The seller tells the buyer his cost price as well as his profit he is adding to the cost. Modern form of Morabaha has become the single most popular technique of financing all over the world.

Bay' al-Tawarruq

This document defines and discusses the concept of bay' al-tawarruq, an Islamic financing structure. It provides the definition, evidence from Islamic legal sources, key pillars and participants, types, conditions and a modern application of bay' al-tawarruq. Bay' al-tawarruq involves the purchase of a commodity on credit followed by the immediate resale of that commodity to a third party for a lower price in cash. The document outlines the different types and conditions that must be met for bay' al-tawarruq to be valid according to Islamic law.

ISSUES AND RECOMMENDATIONS IN MUSHARAKAH MUTANAQISAH HOUSE FINANCING

BY ZALEHA ZAIN.

In our world nowadays, the contract of Al-Bay’ Bithaman Ajil (BBA) had always been used for long time duration of financing. For example, home financing. In Malaysia also, this concept is popular and it showed that at the Kuala Lumpur High Court alone, 90% of the 3,200 Muamalat cases registered between 2003 to 2009 concerns BBA . While the BBA is popular, it has proven to be quite unsatisfactory to the customers and bankers. That’s why Musharakah Mutanaqisah concept is being argued as a better contract than BBA for long time duration.

THIS PAPER DISCUSSED ON THE ISSUES AND RECOMS OF MM.

Credit Risk

This document discusses credit risk in Islamic finance. It begins by defining credit risk as the potential financial loss from a counterparty failing to meet contractual obligations. It then outlines the various types of credit risk exposures that can occur in common Islamic financing contracts such as mudarabah, musharakah, murabahah, ijarah, salam and istisna. The document also discusses IFSB guiding principles for credit risk management, including conducting due diligence reviews and having appropriate risk mitigation techniques. It emphasizes the importance of effective credit risk management for ensuring the financial stability and growth of Islamic banks.

Collateral Management and Market Developments - Whitepaper

1) Collateral management has become increasingly important for financial institutions due to market developments like increased collateral circulation and new regulations requiring more collateral. It is no longer a back office function but a major challenge.

should build or buy systems that can integrate with existing

2) Key features of collateral management include bi-party agreements between two parties, tri-party agreements involving a third party custodian, collateral trading and re-hypothecation, and repurchase (repo) agreements.

infrastructure and provide a centralized view of collateral across

3) Best practices for financial institutions include regularly revaluing collateral, maintaining relationships with key clients, performing regular portfolio reconciliations, considering outsourcing collateral

Credit Risk of UAE banks

This document analyzes the credit risk of UAE banks and corporations. It discusses research methodology, hypotheses, types of credit risk, and principles of managing credit risk. Cross-sectional analysis of corporate financial ratios is used to assess creditworthiness. The empirical analysis finds Etisalat and Surooh to have the lowest credit risk among corporations, while Citibank and HSBC are found to have the lowest risk among banks. Conclusions state that analysis of financial ratios can help identify firms and banks with the highest and lowest credit risk.

More Related Content

What's hot

Operational Risk

Operational risk in Islamic finance can arise from a variety of sources. The document identifies six main categories of operational risk: 1) Shariah non-compliance risk, 2) people risk, 3) technology risk, 4) fiduciary risk, 5) legal risk, and 6) reputational risk. It also discusses the nature of operational risks as either internally or externally inflicted, the impacts as direct or indirect, and the degree of expectancy as expected or unexpected losses. Proper identification and management of operational risks are important for Islamic financial institutions.

Islamic banking by G.Reka

This document provides an overview of Islamic banking including its meaning, principles, deposits, differences from conventional banking, benefits, issues and a SWOT analysis. The key points are:

- Islamic banking complies with Sharia law and prohibits interest, requiring profit and loss sharing. It aims to achieve socially and financially acceptable objectives.

- The basic principles are sharing of profit and loss, prohibiting investment in unlawful businesses and interest. Deposits include savings, current and investment accounts.

- It differs from conventional banking in its basis in Islamic principles, risk sharing approach, and status as partners rather than creditors/debtors.

- Benefits include inclusive economic growth, availability of funds, and protection from

Bba2

The document discusses the issue of Bai Bithaman Ajil (BBA) contracts as used in Islamic financing in Malaysia. It summarizes the conceptual model of BBA, which involves the deferred payment sale of an asset from a seller to a purchaser. The document then discusses 5 previous court cases related to BBA and the legal issues they raised. The cases analyzed whether the BBA structure qualified as a legitimate sale contract under Shariah or resembled interest-based financing. The document concludes by noting the Malaysian government strengthened regulations on Islamic finance to address legal uncertainties surrounding BBA raised by the court cases.

Murabaha finance

This document provides an overview of Murabaha finance, which is a particular type of sale in Islamic finance where the seller discloses the cost of purchasing an asset and sells it to the buyer at a higher price to generate a profit. The document defines Murabaha and explains its key features and components. It also outlines three common models for structuring Murabaha transactions, with Model III involving banks as the most prevalent in modern Islamic banking. Model III is explained in further detail through its typical phases and documentation requirements.

Murabaha mbl

This document provides an introduction and overview of Murabaha, an Islamic financing structure. It defines Murabaha as a sale where the seller discloses the cost of goods to the buyer and adds a known profit. The key features are that the asset being sold must exist, the sale price must be determined, and the sale must be unconditional. It then outlines the basic 6 step process for Murabaha financing between a bank and client, where the client acts as an agent to purchase goods on the bank's behalf that are then sold to the client. Finally, it lists some common applications of Murabaha for meeting working capital needs, long-term purchases, and trade finance.

bai as-salam and istisna

1. Bai As-Salam refers to a contract where advance cash payment is made for goods to be delivered later. The seller undertakes to supply specific goods to the buyer at a future date in exchange for the advanced price paid in full.

2. Salam transactions require full payment of the purchase price at the time of sale. This ensures the seller has the liquidity expected and the basic purpose of the transaction is not defeated.

3. Parallel or back-to-back salam involves three parties, where one party enters into two consecutive salam contracts to manage risks from price fluctuations between the contracts.

Risk Management Process in Islamic Banks

Risk management is a vital process for Islamic banks that consists of several interconnected phases. It includes establishing a risk management framework based on ISO 31000:2009, identifying risks through analysis of products and activities, measuring risks using a composite risk index, developing a risk matrix to plot risks by severity and impact, reviewing risks and monitoring actual risk levels. Effective risk management also requires infrastructure like documentation of policies, an organizational structure with risk management committees, use of information technology systems and databases, and selecting appropriate risk measurement models. The goal is to properly manage both generic financial risks and unique risks to Islamic banks like Sharia non-compliance, displaced commercial, and equity investment risks.

BAY' BITHAMAN AAJIL

The document discusses the concept of Bai Bithaman Ajil (BBA), which is an Islamic financing technique that allows for the deferred payment of goods purchased. BBA involves the immediate delivery of an asset to the buyer while payment is postponed to a future date or paid through installments. The document examines the principles, evidence, objectives, mechanics, and pricing considerations of BBA transactions.

chapter 6 islamic banking 2

The document discusses various Islamic financial instruments used in Malaysia. It describes instruments like Mudharabah, Musharakah, Murabahah, Ijarah, and Wakalah. It explains how these instruments work, including the rights and responsibilities of parties in each contract. Shariah committees provide oversight to ensure Islamic banks operate according to Shariah principles.

Risk management in islamic banking

This document discusses risk management in Islamic banking. It begins with definitions of risk management and describes the risk management process. It then outlines the major risks faced by both Islamic and conventional banks, as well as unique risks faced only by Islamic banks. The document discusses the Shariah perspective on risk, as well as tools for risk mitigation and measurement. It provides guidance principles from Basel, IFSB, and other organizations and discusses challenges in capturing unique risks of Islamic banking. It concludes with ten rules of risk management and a word of caution about managing risks in life.

Salam

The document discusses Salam, a type of Islamic financing contract. Some key points:

1. In a Salam contract, the seller undertakes to supply specific goods to the buyer at a future date in exchange for full payment of the price at the time of the contract.

2. Several conditions must be met for a Salam contract to be valid, including full advance payment, precise specification of goods, and setting an exact date and place of delivery.

3. Salam can help finance agricultural sectors by allowing farmers to receive funds upfront before harvest in exchange for committing to future delivery of crops. Banks can use parallel Salam contracts to mitigate delivery risk.

Topic v. islamic bonds sukuk

This document discusses Islamic bonds (sukuk). It begins by defining sukuk and explaining their historical origins. Sukuk are asset-backed financial certificates that represent ownership in the underlying assets. The document then discusses how sukuk are structured, focusing on the most common types - mudarabah, musharakah and ijarah sukuk. It explains the standards from AAOIFI and the process for structuring each type of sukuk. The document concludes by discussing ratings of Islamic bonds, differentiating between sovereign and corporate ratings and the methodology used.

Ijarah

This clause makes the Ijarah contract invalid because selling of the asset cannot be contingent upon fulfilling the terms of the Ijarah contract. Under Islamic finance principles, the lease and sale contracts must be separate, with the sale not being an automatic outcome of fulfilling the lease terms.

Bay al dayn

Bay al-dayn refers to the sale of debt in Islamic finance. It involves the sale and purchase of a quality debt, either to the debtor or a third party. There are differing views among Islamic scholars on whether debt can be sold to a third party. Proponents argue it can be allowed subject to certain conditions to avoid risks like gharar. Critics argue the sale of debt to non-debtors is prohibited due to issues like selling something one does not possess.

Ijarah INTRODUCTION

Ijarah is an Islamic financing method where a lessor leases an asset to a lessee for an agreed upon rental payment. There are three key points:

1) Ijarah allows the use of an asset but ownership remains with the lessor, who bears risks related to ownership. The lessee bears risks related to use of the asset.

2) Rental payments and sale of the asset must be structured separately to avoid making the lease contingent on sale.

3) Rules governing ijarah require the asset to be identified and the lease period determined. Rent can be set ahead of time but not increased unilaterally. The lessee bears costs of use while the lessor

Morabaha Financing

The word Morabaha is taken from the Arabic word Ribh which means Profit. Originally, Morabaha is a contract of sale in which a commodity is sold on profit. The seller tells the buyer his cost price as well as his profit he is adding to the cost. Modern form of Morabaha has become the single most popular technique of financing all over the world.

Bay' al-Tawarruq

This document defines and discusses the concept of bay' al-tawarruq, an Islamic financing structure. It provides the definition, evidence from Islamic legal sources, key pillars and participants, types, conditions and a modern application of bay' al-tawarruq. Bay' al-tawarruq involves the purchase of a commodity on credit followed by the immediate resale of that commodity to a third party for a lower price in cash. The document outlines the different types and conditions that must be met for bay' al-tawarruq to be valid according to Islamic law.

ISSUES AND RECOMMENDATIONS IN MUSHARAKAH MUTANAQISAH HOUSE FINANCING

BY ZALEHA ZAIN.

In our world nowadays, the contract of Al-Bay’ Bithaman Ajil (BBA) had always been used for long time duration of financing. For example, home financing. In Malaysia also, this concept is popular and it showed that at the Kuala Lumpur High Court alone, 90% of the 3,200 Muamalat cases registered between 2003 to 2009 concerns BBA . While the BBA is popular, it has proven to be quite unsatisfactory to the customers and bankers. That’s why Musharakah Mutanaqisah concept is being argued as a better contract than BBA for long time duration.

THIS PAPER DISCUSSED ON THE ISSUES AND RECOMS OF MM.

Credit Risk

This document discusses credit risk in Islamic finance. It begins by defining credit risk as the potential financial loss from a counterparty failing to meet contractual obligations. It then outlines the various types of credit risk exposures that can occur in common Islamic financing contracts such as mudarabah, musharakah, murabahah, ijarah, salam and istisna. The document also discusses IFSB guiding principles for credit risk management, including conducting due diligence reviews and having appropriate risk mitigation techniques. It emphasizes the importance of effective credit risk management for ensuring the financial stability and growth of Islamic banks.

What's hot (20)

ISSUES AND RECOMMENDATIONS IN MUSHARAKAH MUTANAQISAH HOUSE FINANCING

ISSUES AND RECOMMENDATIONS IN MUSHARAKAH MUTANAQISAH HOUSE FINANCING

Similar to Presentation Mudarabah And Agency Costs

Collateral Management and Market Developments - Whitepaper

1) Collateral management has become increasingly important for financial institutions due to market developments like increased collateral circulation and new regulations requiring more collateral. It is no longer a back office function but a major challenge.

should build or buy systems that can integrate with existing

2) Key features of collateral management include bi-party agreements between two parties, tri-party agreements involving a third party custodian, collateral trading and re-hypothecation, and repurchase (repo) agreements.

infrastructure and provide a centralized view of collateral across

3) Best practices for financial institutions include regularly revaluing collateral, maintaining relationships with key clients, performing regular portfolio reconciliations, considering outsourcing collateral

Credit Risk of UAE banks

This document analyzes the credit risk of UAE banks and corporations. It discusses research methodology, hypotheses, types of credit risk, and principles of managing credit risk. Cross-sectional analysis of corporate financial ratios is used to assess creditworthiness. The empirical analysis finds Etisalat and Surooh to have the lowest credit risk among corporations, while Citibank and HSBC are found to have the lowest risk among banks. Conclusions state that analysis of financial ratios can help identify firms and banks with the highest and lowest credit risk.

2015 WACHA Hot Regulatory Exam Issues 03202015

This document summarizes a presentation given by two experts on cyber security and vendor management from a regulator and auditor perspective. It discusses key expectations regulators have for financial institutions (FIs) in managing third-party vendors, including conducting thorough due diligence prior to vendor selection, properly scoping vendor contracts, implementing strong oversight of vendors after onboarding, and ensuring policies are in place for monitoring vendor compliance on an ongoing basis. The top 10 expectations called out include conducting due diligence on vendors, selecting vendors based on certain criteria, negotiating contracts to address audit rights and penalties, properly defining contract scope, implementing strong access controls when vendors are onboarded, conducting regular audits and reviewing vendor-provided SOC reports, and continuously monitoring vendors.

Credit Risk Management Presentation

This document provides an overview of credit risk management practices from a banker's perspective. It discusses the key types of banking risks including credit, market, and operational risk. It describes credit risk measurement techniques such as credit scoring models and models based on stock prices. It also outlines the importance of internal credit risk rating processes and how rating systems can be used for risk-based pricing, portfolio management, and capital allocation. Finally, it discusses lessons learned from bank failures during the financial crisis, including the need for effective liquidity and balance sheet management and stress testing.

Effective Risk Management Strategies for Factoring Success.pptx

Factoring, which involves the purchase of accounts receivable to provide businesses with quick access to working capital, is a powerful financial tool that can fuel growth and stability. However, it comes with its own set of risks and challenges.

Visit: https://m1nxt.blogspot.com/2023/12/effective-risk-management-strategies.html

Small Business Risk Factors in Today's Market

This document discusses small business risk factors in today's market. It begins by defining small businesses as those with annual revenue less than $5 million or $50 million and fewer than 10 or 100 employees. It then introduces macroeconomic risk factors like credit risk, interest rate risk, and industry demand. Microeconomic risk factors include transaction risk. The document also discusses how small businesses and credit providers can protect against risks like liquidity risk, price risk, and compliance risk in a down market. It stresses the importance of assessing small business risk factors, owners, and the credit provider's own risks and staff.

F6003Ch 10.php(1)

This document discusses credit analysis and financial distress prediction. It covers key topics including why firms use debt financing, potential downsides of debt financing, and differences in debt financing practices internationally. It also describes the credit analysis process in private debt markets, including conducting financial analysis and assembling loan structures. Methods of predicting financial distress like Altman's Z-score model are also discussed.

Adapting To A Rapidly Changing Work Profile: HR Strategic Risk

Mohammad Fheili has over 30 years of experience in banking. He has delivered over 1,500 hours of training to professional bankers and has held senior roles at several Lebanese banks. Fheili received his undergraduate and graduate degrees from LSU and has taught economics and finance at LSU and LAU for over 25 years. He has published over 25 articles in refereed journals on topics related to money laundering, operational risk, law and economics. Fheili currently works as an executive at JTB Bank in Lebanon.

Rating risk

This document discusses risk management practices in the Indian banking system and supervision by the Reserve Bank of India (RBI). It provides an overview of the types of risks banks face, including credit, market, and operational risks. The document also summarizes several academic studies that have examined relationships between macroeconomic variables, bank performance, and risk. Overall, the document analyzes current risk management practices of banks in India as directed by RBI guidelines and regulations.

risk management in banks

The document provides an overview of risk management in the Indian banking sector. It discusses various types of risks banks face, including credit, market, liquidity, operational, and solvency risks. It describes the risk management process and approaches to capital allocation for operational risk under the Basel accords. The document aims to educate readers on identifying and mitigating risks to enhance efficiency and governance in Indian banks.

A safe approach to growing your loan book in wealth management

A white paper on a safe approach to increasing your loan book in wealth management. The paper will discuss the ways in which your loan book can be increased salely and in line with regulation and compliance.

For more information please see: http://www.rockalltech.com/banking/wealth-management

Credit risk management presentation

This presentation provides complete study ofcredit risk management,how it was performed in yester years ,how it is taken care nowadays and what is the road ahead in future

How We Got Here

The document proposes reforms to address the mortgage crisis and prevent future financial catastrophes. It recommends mandating third-party oversight of financial transactions to ensure objective risk ratings and valuations. Appraisals and income verification should be independently verified. Regulations should strengthen penalties for fraudulent behavior and improve transparency through a centralized registry and mandatory reporting of commercial loan data.

Factoring and Forfaiting

This document presents information on factoring and forfaiting. It defines factoring as the conversion of credit sales into cash by selling accounts receivable to a financial institution. It describes the parties involved as the supplier, buyer, and financial intermediary (factor). It then explains the steps in factoring, types of factoring, costs, and compares factoring to loans and bills discounting. Forfaiting is described as purchasing export receivables without recourse to the exporter. The document outlines the forfaiting process, costs, and compares forfaiting to factoring. It provides a comparative analysis of bills discounting, factoring and forfaiting.

Credit risk management lecture

This document discusses various types of risks faced by banks, including credit risk, market risk, operational risk, liquidity risk, and reputation risk. It provides definitions of different risk types such as credit risk, concentration risk, and interest rate risk. The document also covers topics like the importance of credit risk management, factors to consider in credit risk analysis, and modern approaches to assessing and managing credit risk in the banking industry.

The Hazards of Vendor Management - presented to NC Bankers Association by Ric...

The Hazards of Vendor Management - presented to NC Bankers Association by Ric...Poyner Spruill LLP, Attorneys

This document discusses bank vendor management and the vendor risk management life cycle. It provides an overview of understanding vendor risks and regulatory requirements. It describes the categories of vendor risks such as reputation, operational, transaction, financial, legal and compliance, and other risks. It discusses identifying critical vendors and outlines the vendor risk management life cycle, including planning and risk assessment, due diligence and selection, contract review, ongoing monitoring, termination, accountability, documentation, independent reviews, and regulatory reporting.Credit management

The document discusses credit risk management and outlines steps for managing a credit portfolio to minimize risk and optimize returns. It emphasizes formulating flexible credit policies, conducting target market planning and risk assessments, performing periodic reviews, and establishing a system to balance risk and revenue through various risk management objectives and capital adequacy requirements.

Bridging Finance Guide-20 Steps to Bridging Finance Success by Blueray Capital

20 key steps, important terminology and metrics to secure bridging finance in the UK. A helpful guide for property investors by Blueray Capital.

Capitalmarkets

The document discusses capital markets and the bank loan syndication process. It describes two types of loan markets - the investment grade loan market and leveraged loan market. It then details the typical steps in the loan syndication process, including the roles of the issuer/company, arrangers, agents, and lenders. It provides an example of a large syndicated loan for Harrah's Entertainment.

De risking

The document discusses Mohammad Fheili, who has over 30 years of banking experience and currently works as an executive at JTB Bank in Lebanon. He has delivered over 1,500 hours of training to bankers and has published over 25 articles. The main document appears to be about an upcoming forum on de-risking that Fheili will be speaking at, as it covers topics like the challenges in compliance that are driving banks to de-risk, the implications of de-risking, and strategies for managing risk while continuing to serve clients.

Similar to Presentation Mudarabah And Agency Costs (20)

Collateral Management and Market Developments - Whitepaper

Collateral Management and Market Developments - Whitepaper

Effective Risk Management Strategies for Factoring Success.pptx

Effective Risk Management Strategies for Factoring Success.pptx

Adapting To A Rapidly Changing Work Profile: HR Strategic Risk

Adapting To A Rapidly Changing Work Profile: HR Strategic Risk

A safe approach to growing your loan book in wealth management

A safe approach to growing your loan book in wealth management

The Hazards of Vendor Management - presented to NC Bankers Association by Ric...

The Hazards of Vendor Management - presented to NC Bankers Association by Ric...

Bridging Finance Guide-20 Steps to Bridging Finance Success by Blueray Capital

Bridging Finance Guide-20 Steps to Bridging Finance Success by Blueray Capital

Recently uploaded

1. Elemental Economics - Introduction to mining.pdf

After this first you should: Understand the nature of mining; have an awareness of the industry’s boundaries, corporate structure and size; appreciation the complex motivations and objectives of the industries’ various participants; know how mineral reserves are defined and estimated, and how they evolve over time.

2. Elemental Economics - Mineral demand.pdf

After this second you should be able to: Explain the main determinants of demand for any mineral product, and their relative importance; recognise and explain how demand for any product is likely to change with economic activity; recognise and explain the roles of technology and relative prices in influencing demand; be able to explain the differences between the rates of growth of demand for different products.

1:1制作加拿大麦吉尔大学毕业证硕士学历证书原版一模一样

原版一模一样【微信:741003700 】【加拿大麦吉尔大学毕业证硕士学历证书】【微信:741003700 】学位证,留信认证(真实可查,永久存档)offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原海外各大学 Bachelor Diploma degree, Master Degree Diploma

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

1.2 Business Ideas Business Ideas Busine

Business Ideas PowerpointBusiness Ideas PowerpointBusiness Ideas PowerpointBusiness Ideas PowerpointBusiness Ideas PowerpointBusiness Ideas PowerpointBusiness Ideas PowerpointBusiness Ideas PowerpointBusiness Ideas PowerpointBusiness Ideas PowerpointBusiness Ideas PowerpointBusiness Ideas PowerpointBusiness Ideas PowerpointBusiness Ideas PowerpointBusiness Ideas Powerpoint

Solution Manual For Financial Accounting, 8th Canadian Edition 2024, by Libby...

Solution Manual For Financial Accounting, 8th Canadian Edition 2024, by Libby, Hodge, Verified Chapters 1 - 13, Complete Newest Version Solution Manual For Financial Accounting, 8th Canadian Edition by Libby, Hodge, Verified Chapters 1 - 13, Complete Newest Version Solution Manual For Financial Accounting 8th Canadian Edition Pdf Chapters Download Stuvia Solution Manual For Financial Accounting 8th Canadian Edition Ebook Download Stuvia Solution Manual For Financial Accounting 8th Canadian Edition Pdf Solution Manual For Financial Accounting 8th Canadian Edition Pdf Download Stuvia Financial Accounting 8th Canadian Edition Pdf Chapters Download Stuvia Financial Accounting 8th Canadian Edition Ebook Download Stuvia Financial Accounting 8th Canadian Edition Pdf Financial Accounting 8th Canadian Edition Pdf Download Stuvia

The Rise of Generative AI in Finance: Reshaping the Industry with Synthetic Data

In this presentation, we will explore the rise of generative AI in finance and its potential to reshape the industry. We will discuss how generative AI can be used to develop new products, combat fraud, and revolutionize risk management. Finally, we will address some of the ethical considerations and challenges associated with this powerful technology.

SWAIAP Fraud Risk Mitigation Prof Oyedokun.pptx

SWAIAP Fraud Risk Mitigation Prof Oyedokun.pptxGodwin Emmanuel Oyedokun MBA MSc PhD FCA FCTI FCNA CFE FFAR

Lecture slide titled Fraud Risk Mitigation, Webinar Lecture Delivered at the Society for West African Internal Audit Practitioners (SWAIAP) on Wednesday, November 8, 2023.

This assessment plan proposal is to outline a structured approach to evaluati...

This assessment plan proposal is to outline a structured approach to evaluati...lamluanvan.net Viết thuê luận văn

Luận Văn Group hỗ trợ viết luận văn thạc sĩ,chuyên đề,khóa luận tốt nghiệp, báo cáo thực tập, Assignment, Essay

Zalo/Sdt 0967 538 624/ 0886 091 915 Website:lamluanvan.net

Tham gia nhóm hỗ trợ viết bài fb: https://www.facebook.com/groups/285625754522599?locale=vi_VNSeminar: Gender Board Diversity through Ownership Networks

Seminar on gender diversity spillovers through ownership networks at FAME|GRAPE. Presenting novel research. Studies in economics and management using econometrics methods.

一比一原版(UCSB毕业证)圣芭芭拉分校毕业证如何办理

UCSB毕业证文凭证书【微信95270640】办理圣芭芭拉分校毕业证成绩单(Q微信95270640)毕业证学历认证OFFER专卖国外文凭学历学位证书办理澳洲文凭|澳洲毕业证,澳洲学历认证,澳洲成绩单 澳洲offer,教育部学历认证及使馆认证永久可查 ,国外毕业证|国外学历认证,国外学历文凭证书 UCSB毕业证,UCSB毕业证,UCSB毕业证,UCSB毕业证,UCSB毕业证,UCSB毕业证,UCSB毕业证,专业为留学生办理毕业证、成绩单、使馆留学回国人员证明、教育部学历学位认证、录取通知书、Offer、

【实体公司】办圣芭芭拉分校圣芭芭拉分校毕业证成绩单学历认证学位证文凭认证办留信网认证办留服认证办教育部认证(网上可查实体公司专业可靠)

— — — 留学归国服务中心 — — -

【主营项目】

一.圣芭芭拉分校毕业证成绩单使馆认证教育部认证成绩单等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

国外毕业证学位证成绩单办理流程:

1客户提供圣芭芭拉分校圣芭芭拉分校毕业证成绩单办理信息:姓名生日专业学位毕业时间等(如信息不确定可以咨询顾问:我们有专业老师帮你查询);

2开始安排制作毕业证成绩单电子图;

3毕业证成绩单电子版做好以后发送给您确认;

4毕业证成绩单电子版您确认信息无误之后安排制作成品;

5成品做好拍照或者视频给您确认;

6快递给客户(国内顺丰国外DHLUPS等快读邮寄)。

专业服务请勿犹豫联系我!本公司是留学创业和海归创业者们的桥梁。一次办理终生受用一步到位高效服务。详情请在线咨询办理,欢迎有诚意办理的客户咨询!洽谈。

招聘代理:本公司诚聘英国加拿大澳洲新西兰美国法国德国新加坡各地代理人员如果你有业余时间有兴趣就请联系我们咨询顾问:+微信:95270640田里逡巡一番抱起一只硕大的西瓜用石刀劈开抑或用拳头砸开每人抱起一大块就啃啃得满嘴满脸猴屁股般的红艳大家一个劲地指着对方吃吃地笑瓜裂得古怪奇形怪状却丝毫不影响瓜味甜丝丝的满嘴生津遍地都是瓜横七竖八的活像掷满了一地的大石块摘走二三只爷爷是断然发现不了的即便发现爷爷也不恼反而教山娃辨认孰熟孰嫩孰甜孰淡名义上是护瓜往往在瓜棚里坐上一刻饱吃一顿后山娃就领着阿黑漫山遍野地跑阿黑是一条黑色的大猎狗挺机灵的是山室

一比一原版(GWU,GW毕业证)加利福尼亚大学|尔湾分校毕业证如何办理

GWU,GW毕业证录取书【微信95270640】一比一伪造加利福尼亚大学|尔湾分校文凭@假冒GWU,GW毕业证成绩单+Q微信95270640办理GWU,GW学位证书@仿造GWU,GW毕业文凭证书@购买加利福尼亚大学|尔湾分校毕业证成绩单GWU,GW真实使馆认证/真实留信认证回国人员证明

全套服务:加利福尼亚大学|尔湾分校加利福尼亚大学|尔湾分校毕业证成绩单真实回国人员证明 #真实教育部认证。让您回国发展信心十足#铸就十年品质!信誉!实体公司!可以视频看办公环境样板如需办理真实可查可以先到公司面谈勿轻信小中介黑作坊!

可以提供加利福尼亚大学|尔湾分校钢印 #水印 #烫金 #激光防伪 #凹凸版 #最新版的毕业证 #百分之百让您绝对满意

印刷DHL快递毕业证 #成绩单7个工作日真实大使馆教育部认证1个月。为了达到高水准高效率

请您先以qq或微信的方式对我们的服务进行了解后如果有加利福尼亚大学|尔湾分校加利福尼亚大学|尔湾分校毕业证成绩单帮助再进行电话咨询。

国外毕业证学位证成绩单如何办理:

1客户提供办理信息:姓名生日专业学位毕业时间等(如信息不确定可以咨询顾问:我们有专业老师帮你查询);

2开始安排制作加利福尼亚大学|尔湾分校毕业证成绩单电子图;

3毕业证成绩单电子版做好以后发送给您确认;

4毕业证成绩单电子版您确认信息无误之后安排制作成品;

5成品做好拍照或者视频给您确认;

6快递给客户(国内顺丰国外DHLUPS等快读邮寄)。口水苦涩无比山娃一边游泳一边念念不忘那元门票尤令山娃气愤的是泳池老板居然硬让父亲买了一大一小二条巴掌般大的裤衩衩走出泳池山娃感觉透身粘粘乎乎散发着药水味有点痒山娃顿时留恋起家乡的小河潺潺活水清凉无比日子就这样孤寂而快乐地过着寂寞之余山娃最神往最开心就是晚上无论多晚多累父亲总要携山娃出去兜风逛夜市流光溢彩人潮涌动的都市夜生活总让山娃目不暇接惊叹不已父亲老问山娃想买什么想吃什么山娃知道父亲赚钱很辛苦在

Abhay Bhutada Leads Poonawalla Fincorp To Record Low NPA And Unprecedented Gr...

Under the leadership of Abhay Bhutada, Poonawalla Fincorp has achieved record-low Non-Performing Assets (NPA) and witnessed unprecedented growth. Bhutada's strategic vision and effective management have significantly enhanced the company's financial health, showcasing a robust performance in the financial sector. This achievement underscores the company's resilience and ability to thrive in a competitive market, setting a new benchmark for operational excellence in the industry.

Eco-Innovations and Firm Heterogeneity.

Evidence from Italian Family and Nonf...

Eco-Innovations and Firm Heterogeneity.

Evidence from Italian Family and Nonf...University of Calabria

The study analyzes differences and primary drivers of green performance between family firms and non-family firms

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...AntoniaOwensDetwiler

"Does Foreign Direct Investment Negatively Affect Preservation of Culture in the Global South? Case Studies in Thailand and Cambodia."

Do elements of globalization, such as Foreign Direct Investment (FDI), negatively affect the ability of countries in the Global South to preserve their culture? This research aims to answer this question by employing a cross-sectional comparative case study analysis utilizing methods of difference. Thailand and Cambodia are compared as they are in the same region and have a similar culture. The metric of difference between Thailand and Cambodia is their ability to preserve their culture. This ability is operationalized by their respective attitudes towards FDI; Thailand imposes stringent regulations and limitations on FDI while Cambodia does not hesitate to accept most FDI and imposes fewer limitations. The evidence from this study suggests that FDI from globally influential countries with high gross domestic products (GDPs) (e.g. China, U.S.) challenges the ability of countries with lower GDPs (e.g. Cambodia) to protect their culture. Furthermore, the ability, or lack thereof, of the receiving countries to protect their culture is amplified by the existence and implementation of restrictive FDI policies imposed by their governments.

My study abroad in Bali, Indonesia, inspired this research topic as I noticed how globalization is changing the culture of its people. I learned their language and way of life which helped me understand the beauty and importance of cultural preservation. I believe we could all benefit from learning new perspectives as they could help us ideate solutions to contemporary issues and empathize with others.一比一原版(IC毕业证)帝国理工大学毕业证如何办理

IC毕业证文凭证书【微信95270640】一比一伪造帝国理工大学文凭@假冒IC毕业证成绩单+Q微信95270640办理IC学位证书@仿造IC毕业文凭证书@购买帝国理工大学毕业证成绩单IC真实使馆认证/真实留信认证回国人员证明

如果您是以下情况,我们都能竭诚为您解决实际问题:【公司采用定金+余款的付款流程,以最大化保障您的利益,让您放心无忧】

1、在校期间,因各种原因未能顺利毕业,拿不到官方毕业证+微信95270640

2、面对父母的压力,希望尽快拿到帝国理工大学帝国理工大学毕业证学历书;

3、不清楚流程以及材料该如何准备帝国理工大学帝国理工大学毕业证学历书;

4、回国时间很长,忘记办理;

5、回国马上就要找工作,办给用人单位看;

6、企事业单位必须要求办理的;

面向美国乔治城大学毕业留学生提供以下服务:

【★帝国理工大学帝国理工大学毕业证学历书毕业证、成绩单等全套材料,从防伪到印刷,从水印到钢印烫金,与学校100%相同】

【★真实使馆认证(留学人员回国证明),使馆存档可通过大使馆查询确认】

【★真实教育部认证,教育部存档,教育部留服网站可查】

【★真实留信认证,留信网入库存档,可查帝国理工大学帝国理工大学毕业证学历书】

我们从事工作十余年的有着丰富经验的业务顾问,熟悉海外各国大学的学制及教育体系,并且以挂科生解决毕业材料不全问题为基础,为客户量身定制1对1方案,未能毕业的回国留学生成功搭建回国顺利发展所需的桥梁。我们一直努力以高品质的教育为起点,以诚信、专业、高效、创新作为一切的行动宗旨,始终把“诚信为主、质量为本、客户第一”作为我们全部工作的出发点和归宿点。同时为海内外留学生提供大学毕业证购买、补办成绩单及各类分数修改等服务;归国认证方面,提供《留信网入库》申请、《国外学历学位认证》申请以及真实学籍办理等服务,帮助众多莘莘学子实现了一个又一个梦想。

专业服务,请勿犹豫联系我

如果您真实毕业回国,对于学历认证无从下手,请联系我,我们免费帮您递交

诚招代理:本公司诚聘当地代理人员,如果你有业余时间,或者你有同学朋友需要,有兴趣就请联系我

你赢我赢,共创双赢

你做代理,可以帮助帝国理工大学同学朋友

你做代理,可以拯救帝国理工大学失足青年

你做代理,可以挽救帝国理工大学一个个人才

你做代理,你将是别人人生帝国理工大学的转折点

你做代理,可以改变自己,改变他人,给他人和自己一个机会美景更增添一份性感夹杂着一份纯洁的妖娆毫无违和感实在给人带来一份悠然幸福的心情如果说现在的审美已经断然拒绝了无声的话那么在树林间飞掠而过的小鸟叽叽咋咋的叫声是否就是这最后的点睛之笔悠然走在林间的小路上宁静与清香一丝丝的盛夏气息吸入身体昔日生活里的繁忙与焦躁早已淡然无存心中满是悠然清淡的芳菲身体不由的轻松脚步也感到无比的轻快走出这盘栾交错的小道眼前是连绵不绝的山峦浩荡天地间大自然毫无吝啬的展现它的达

Recently uploaded (20)

1. Elemental Economics - Introduction to mining.pdf

1. Elemental Economics - Introduction to mining.pdf

Solution Manual For Financial Accounting, 8th Canadian Edition 2024, by Libby...

Solution Manual For Financial Accounting, 8th Canadian Edition 2024, by Libby...

Applying the Global Internal Audit Standards_AIS.pdf

Applying the Global Internal Audit Standards_AIS.pdf

The Rise of Generative AI in Finance: Reshaping the Industry with Synthetic Data

The Rise of Generative AI in Finance: Reshaping the Industry with Synthetic Data

G20 summit held in India. Proper presentation for G20 summit

G20 summit held in India. Proper presentation for G20 summit

This assessment plan proposal is to outline a structured approach to evaluati...

This assessment plan proposal is to outline a structured approach to evaluati...

Seminar: Gender Board Diversity through Ownership Networks

Seminar: Gender Board Diversity through Ownership Networks

Abhay Bhutada Leads Poonawalla Fincorp To Record Low NPA And Unprecedented Gr...

Abhay Bhutada Leads Poonawalla Fincorp To Record Low NPA And Unprecedented Gr...

Eco-Innovations and Firm Heterogeneity.

Evidence from Italian Family and Nonf...

Eco-Innovations and Firm Heterogeneity.

Evidence from Italian Family and Nonf...

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...

Presentation Mudarabah And Agency Costs

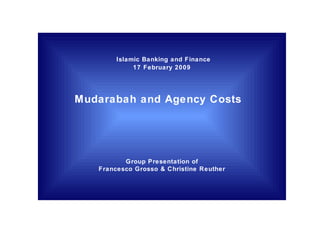

- 1. Islamic Banking and Finance 17 February 2009 Mudarabah and Agency Costs Group Presentation of Francesco Grosso & Christine Reuther

- 8. Main reasons that prevent Islamic banks from entering mudarabah contracts (range from 0 to 1) Reasons preventing Islamic banks from entering mudarabah contracts (range from 0 to1) Problem of Moral Hazard in Mudarabah Contract The combination of unilateral risk bearing and asymmetric information on the side of the Islamic bank provide the agent with the incentive to conceal actions taken and underreport profits made after the contract has been Completed. Level of the agent’s effort and his investment decisions determine the outcome of the investment; however, both may be unobservable to the Islamic bank.

- 12. Mudarabah contracts in practice: case study of Bank Islam Malaysia Berhard (2005) Customer deposits by type of contract 3.Q 2005 (in USD) Performing financing by type of contract 3.Q 2005 (in USD) Performing financing by type of contract 3.Q 2005 (in %) Customer deposits by type of contract 3.Q 2005 (in %) Non-Mudarabah contract Mudarabah contract 43% 57% 70% 15% Bai’ Bithaman Ajil Murabahah Qard al-Hasan Musharakah: 0.5% Mudarabah: 0.1% Others: 0.4% Ijarah Bai al-Inah 9% 3% 2%

- 13. Case study of Bank Islam Malaysia Berhard (continued): Performing Financing by sector of investment 3.Q 2005 (in USD)