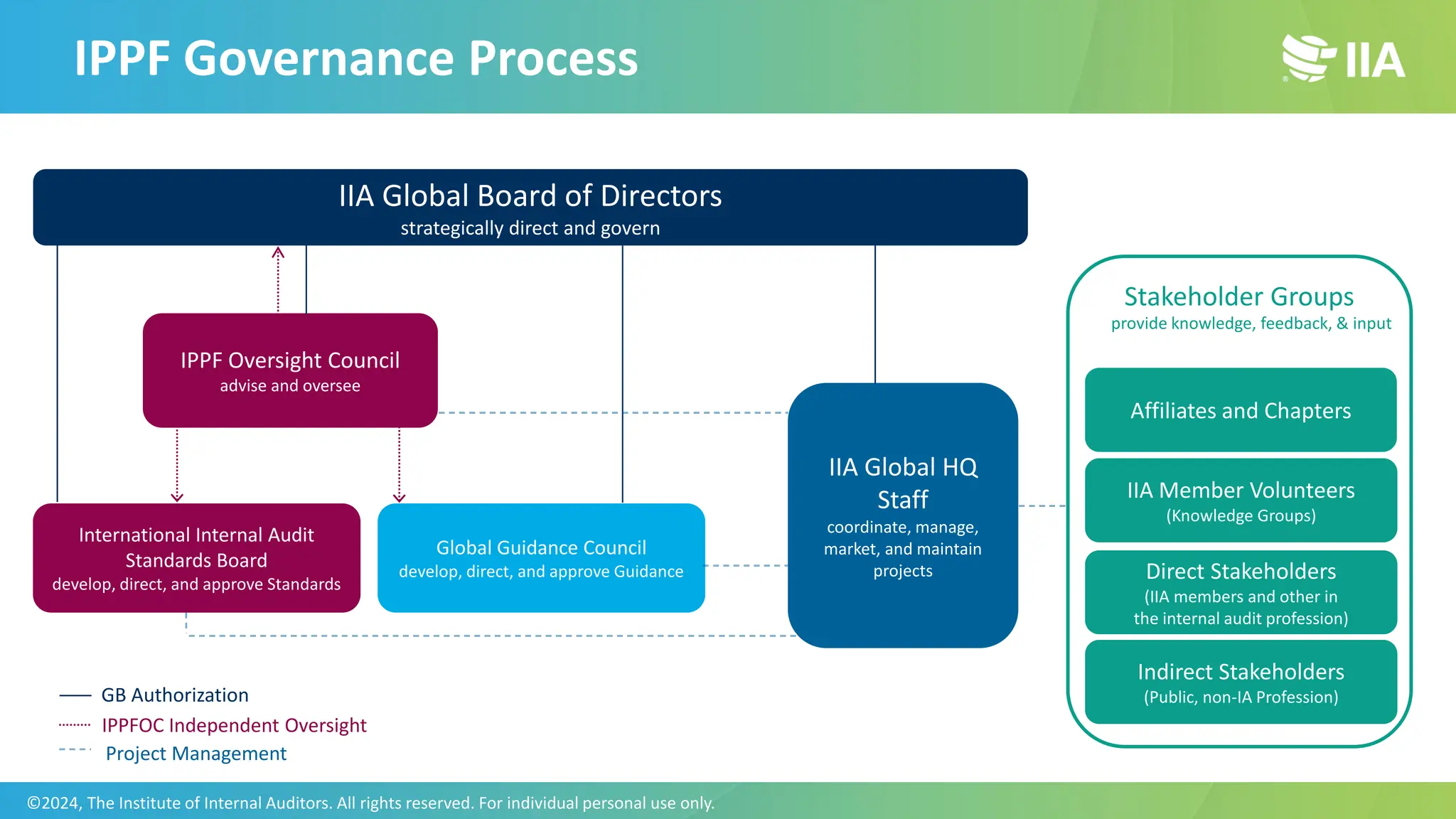

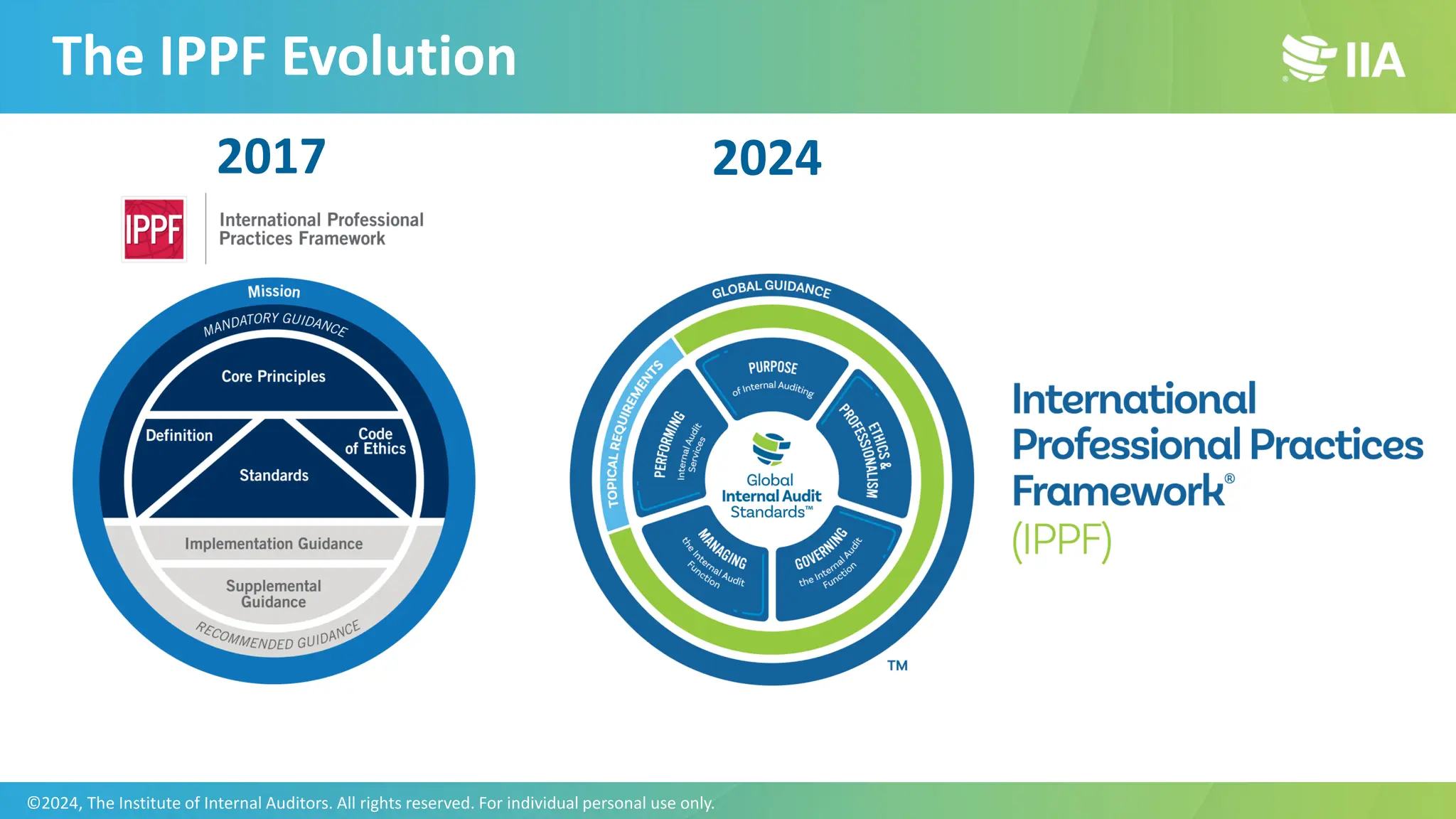

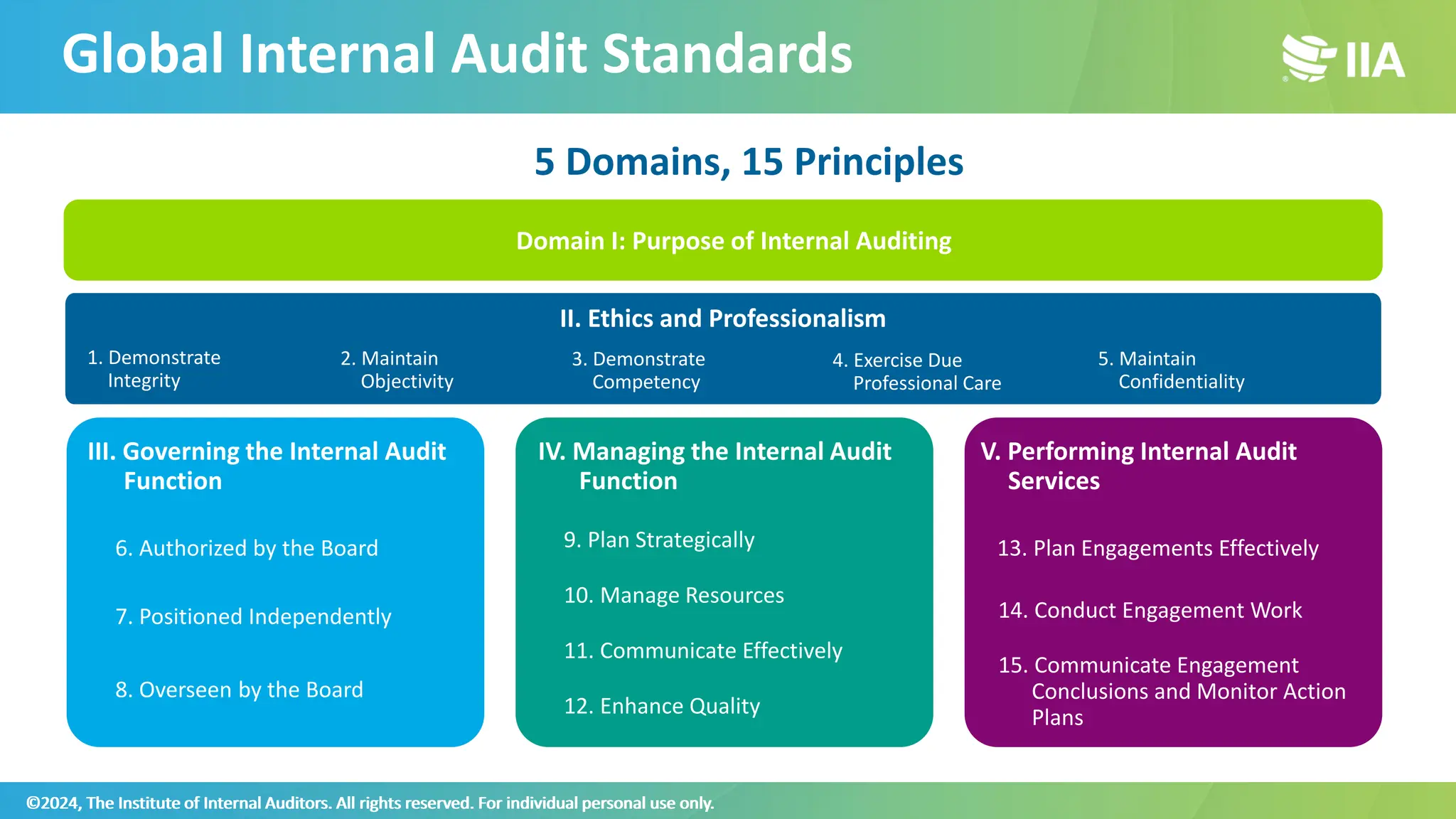

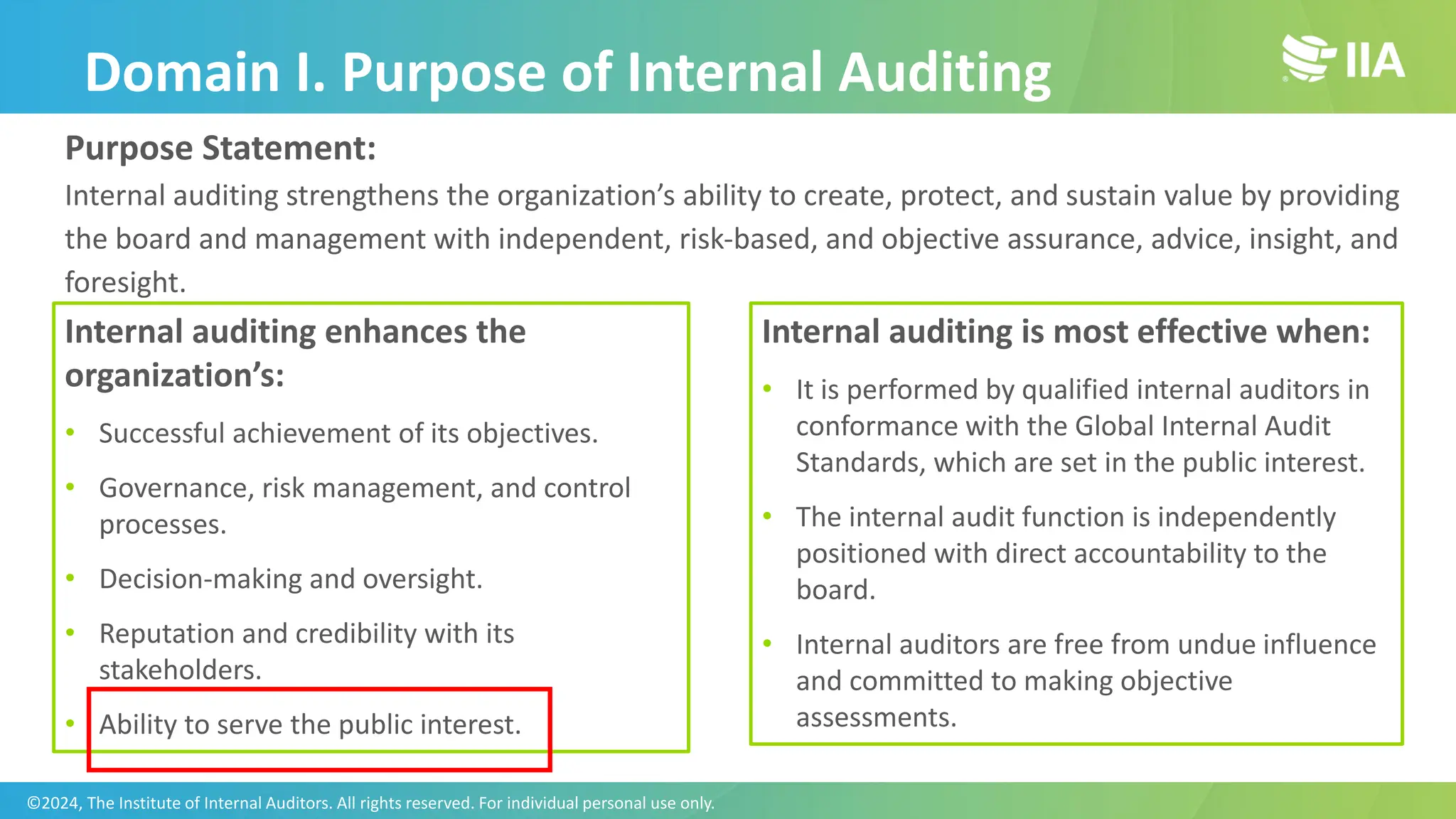

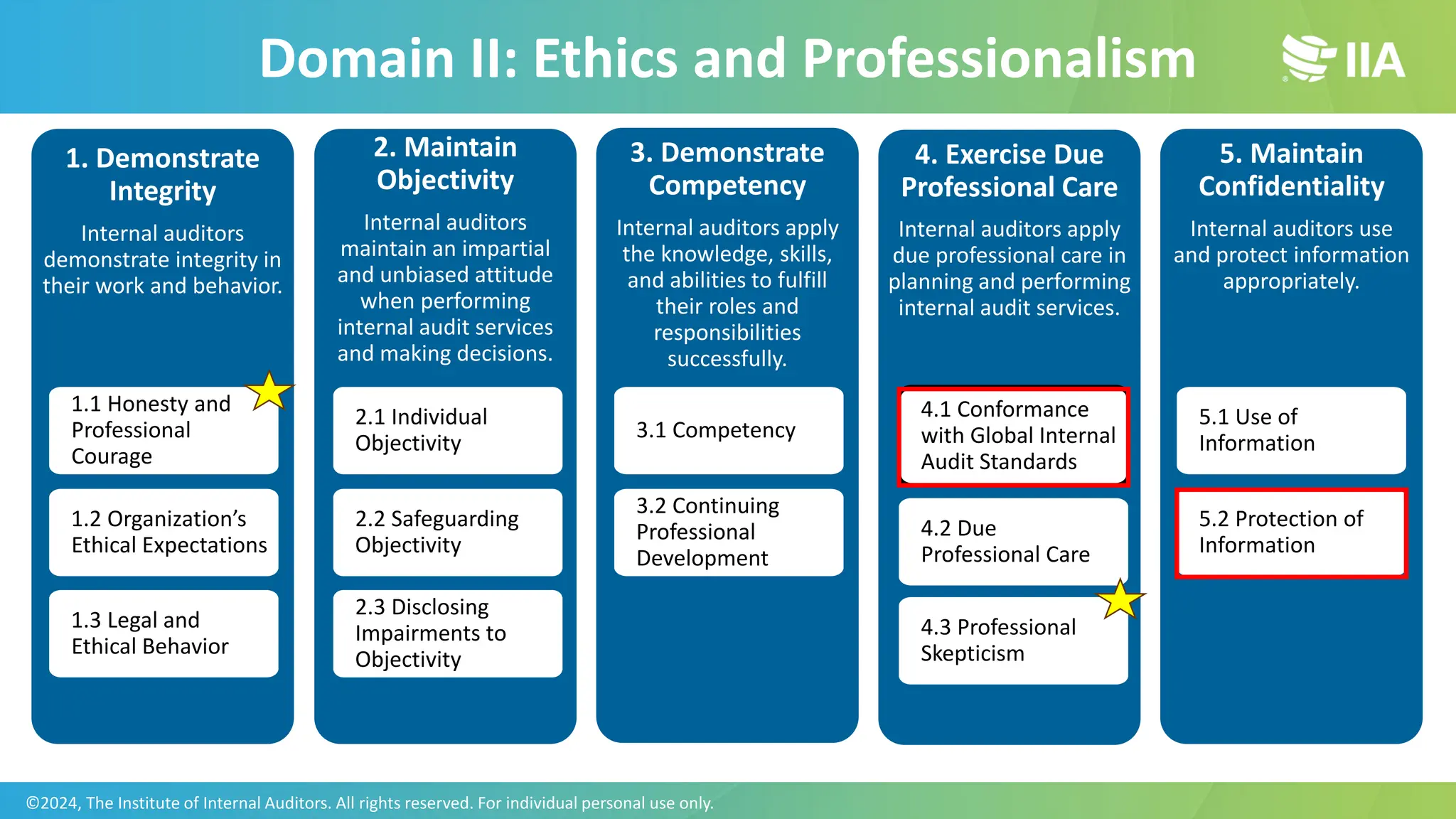

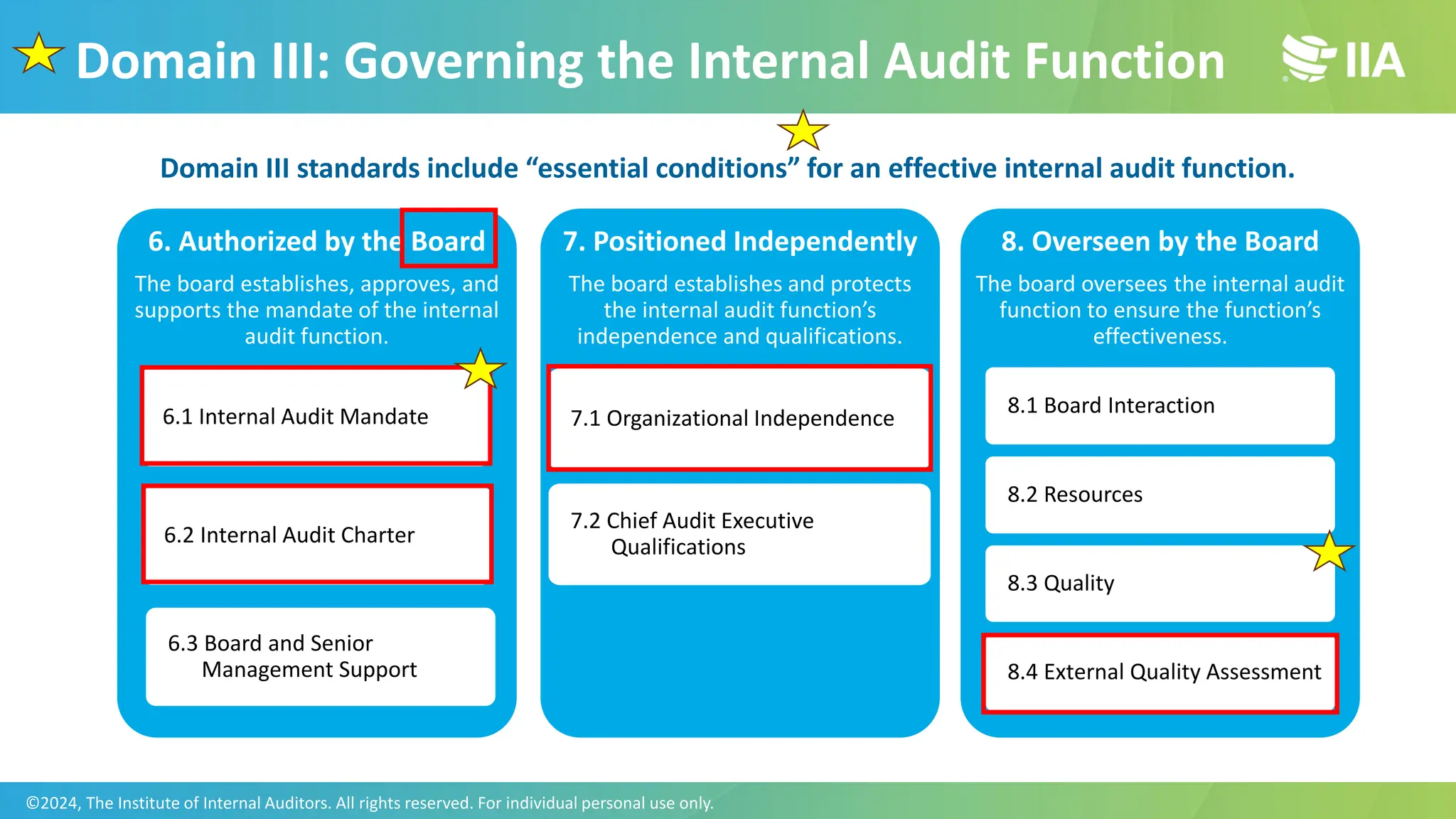

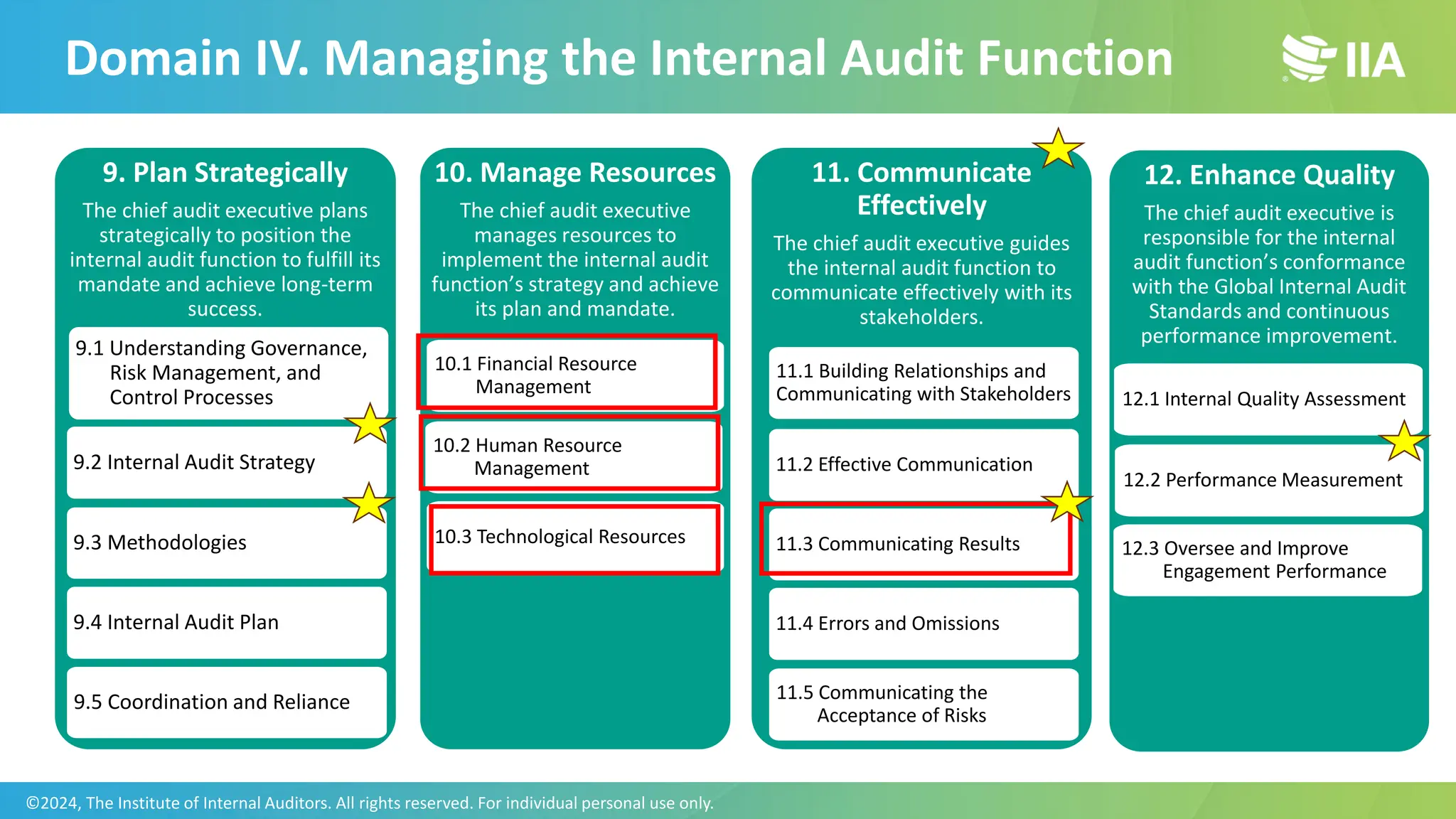

The document presents an overview of the global internal audit standards and their application by the Institute of Internal Auditors Indonesia, detailing the governance and standard-setting process as well as recommendations for public sector implementation. It outlines the evolution of global standards and provides resources available for stakeholders, including a new structure with defined domains, principles, and standards. The document emphasizes the importance of internal auditing in supporting organizational value creation and accountability in the public sector.

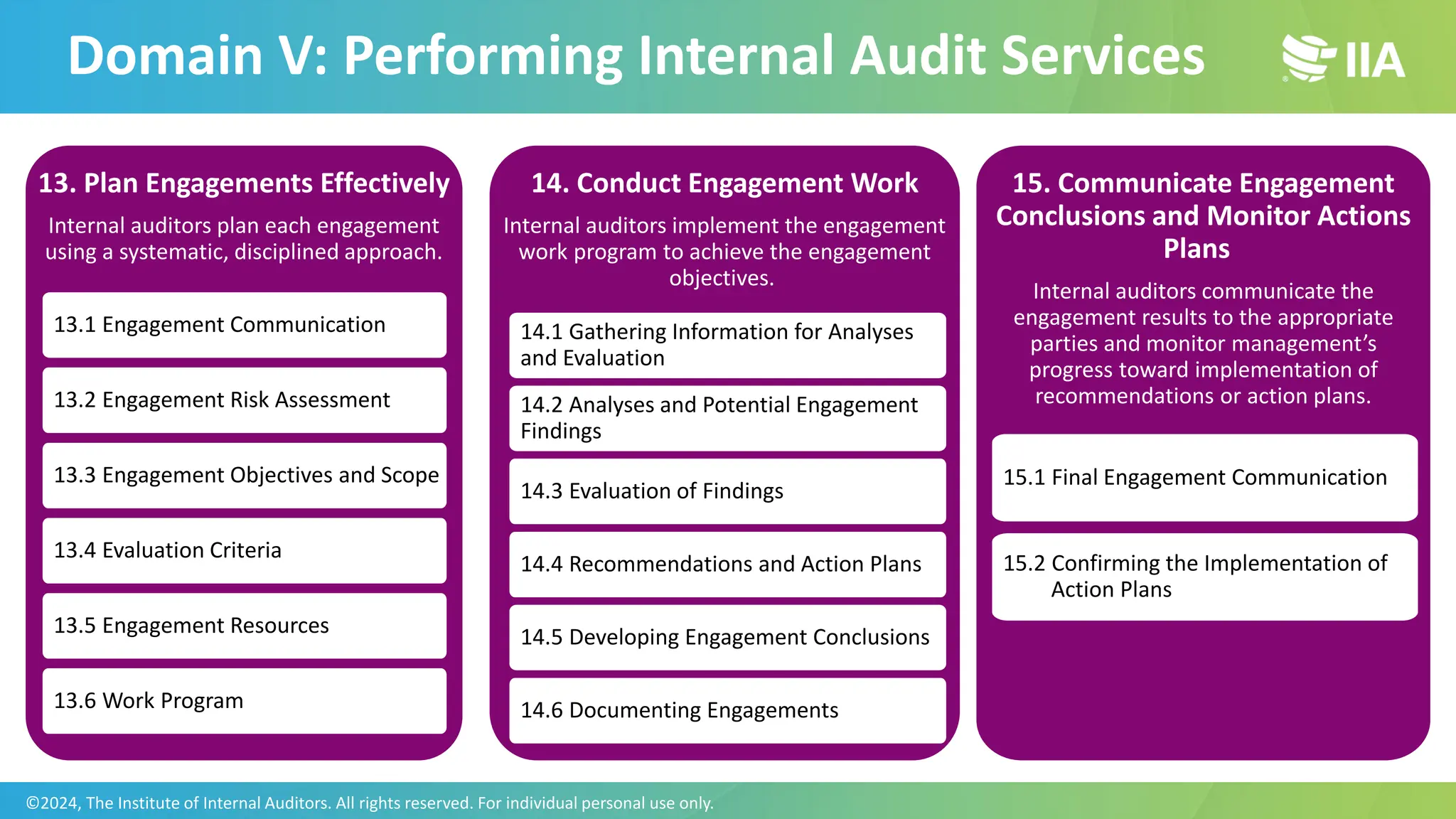

![IIA Indonesia Recommends

Familiarize with the new

Standards

Refresh understanding on

organization values and

assess what value can

Internal Audit provides to

the organizations in

relation to GRC

Obtain feedback from key

stakeholders

Align actions and priorities

to the organization's

vision, strategy, and

governance model and

update the IA Strategic

Plan

Update the IA Charter to

incorporate the new ethics

and professionalism

Enforce ethics

Perform an IA Readiness

Assessment to identify

what needs to change to

conform with the new

Standards.

Assess Chief Audit

qualifications

Create plans to develop

coordination and

collaboration with the first

and second line

Develop Quality

Assurance and

Improvement Programme

(QAIP)

Develop IA strategic

plans: GRC-based plan,

IA strategy, restructuring

audit methodology.

Develop IA performance

measurements.

Reflect these changes in

your IA policies,

procedures, and

templates

Refresh your IA training

and development

programme

Socialize [new] IA

reporting and

communications approach

to all IA stakeholders

©2024, The Institute of Internal Auditors. All rights reserved. For individual personal use only.](https://image.slidesharecdn.com/applyingtheglobalinternalauditstandardsais-240607080046-da592d7c/75/Applying-the-Global-Internal-Audit-Standards_AIS-pdf-33-2048.jpg)