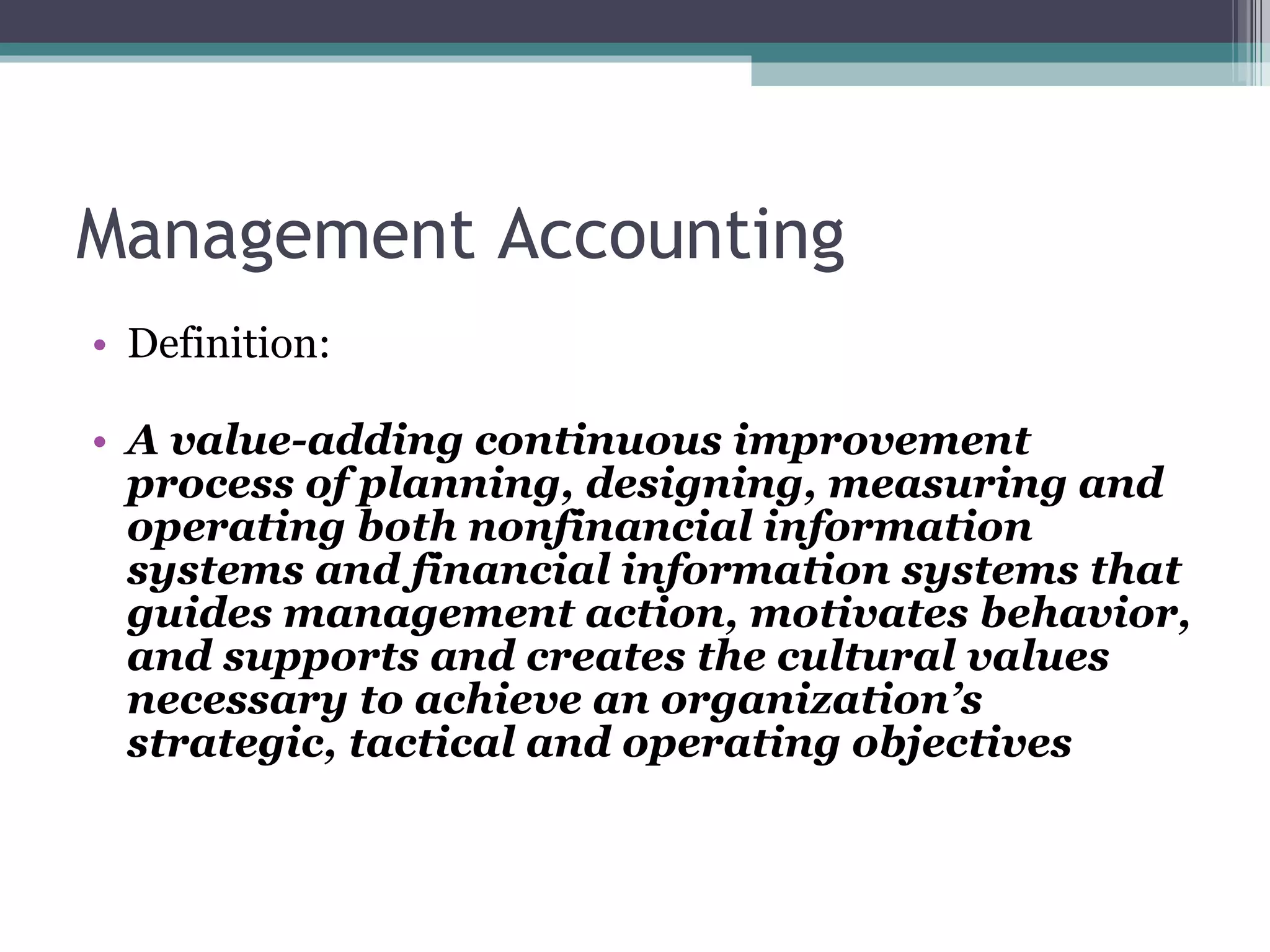

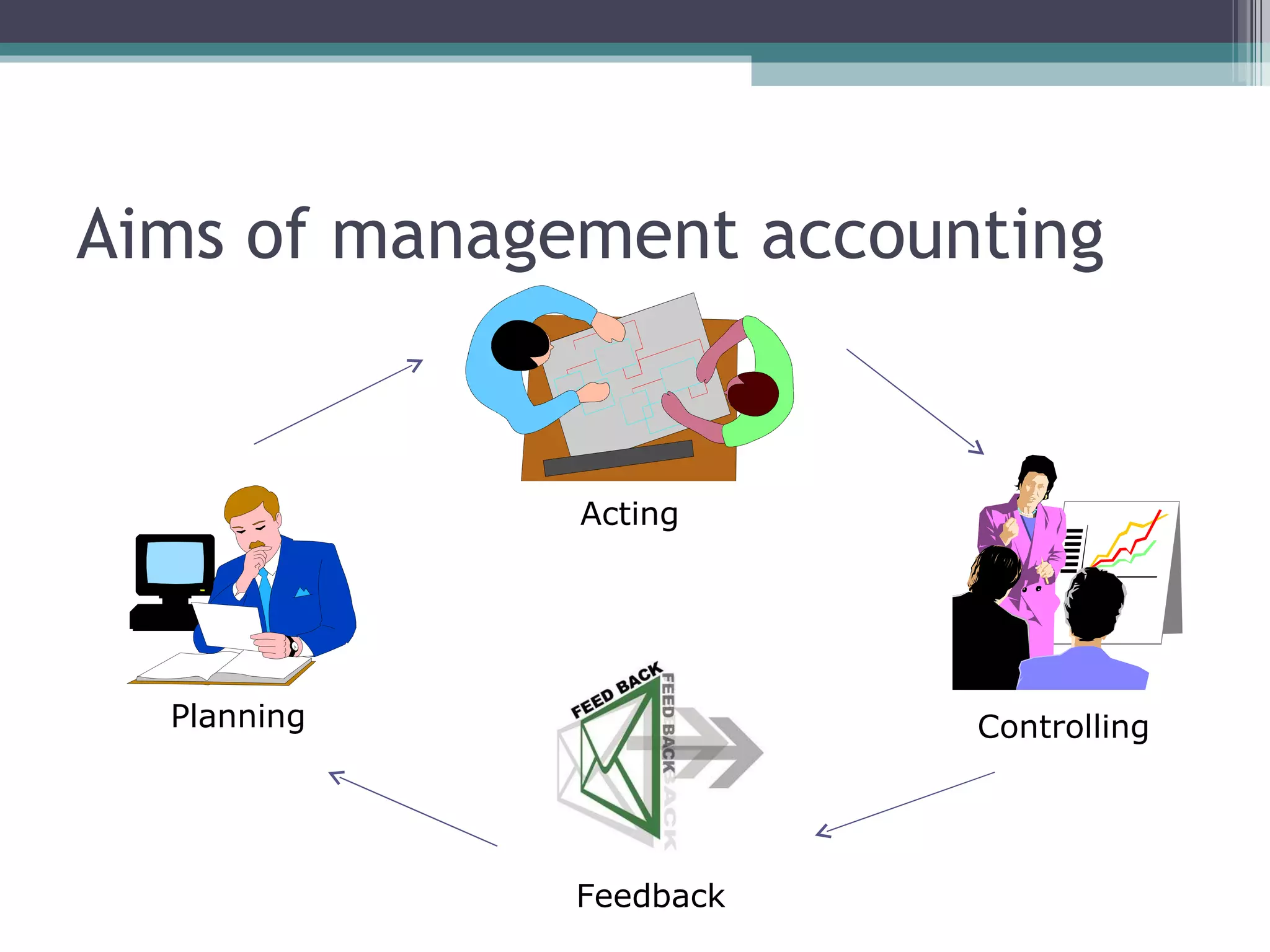

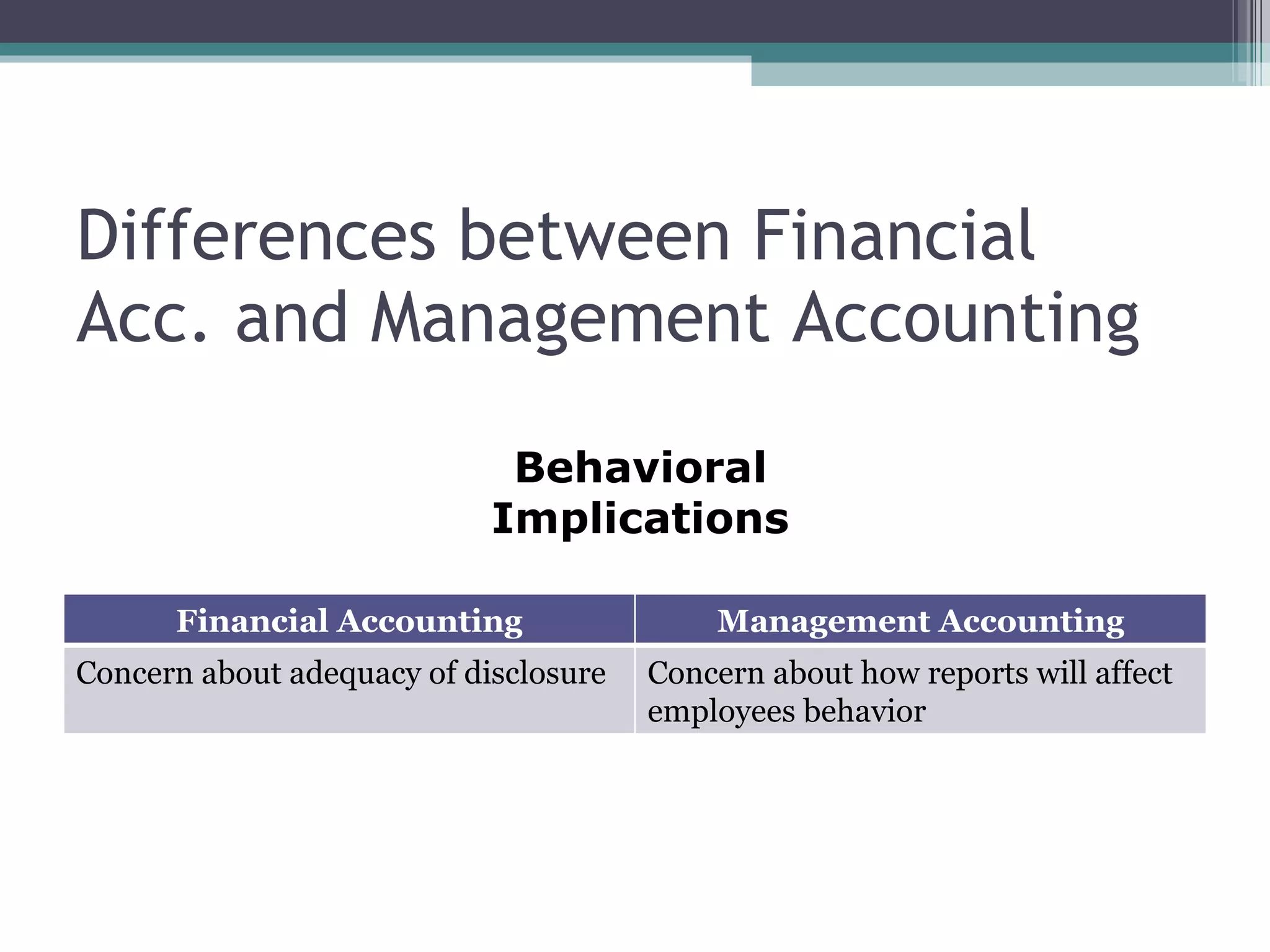

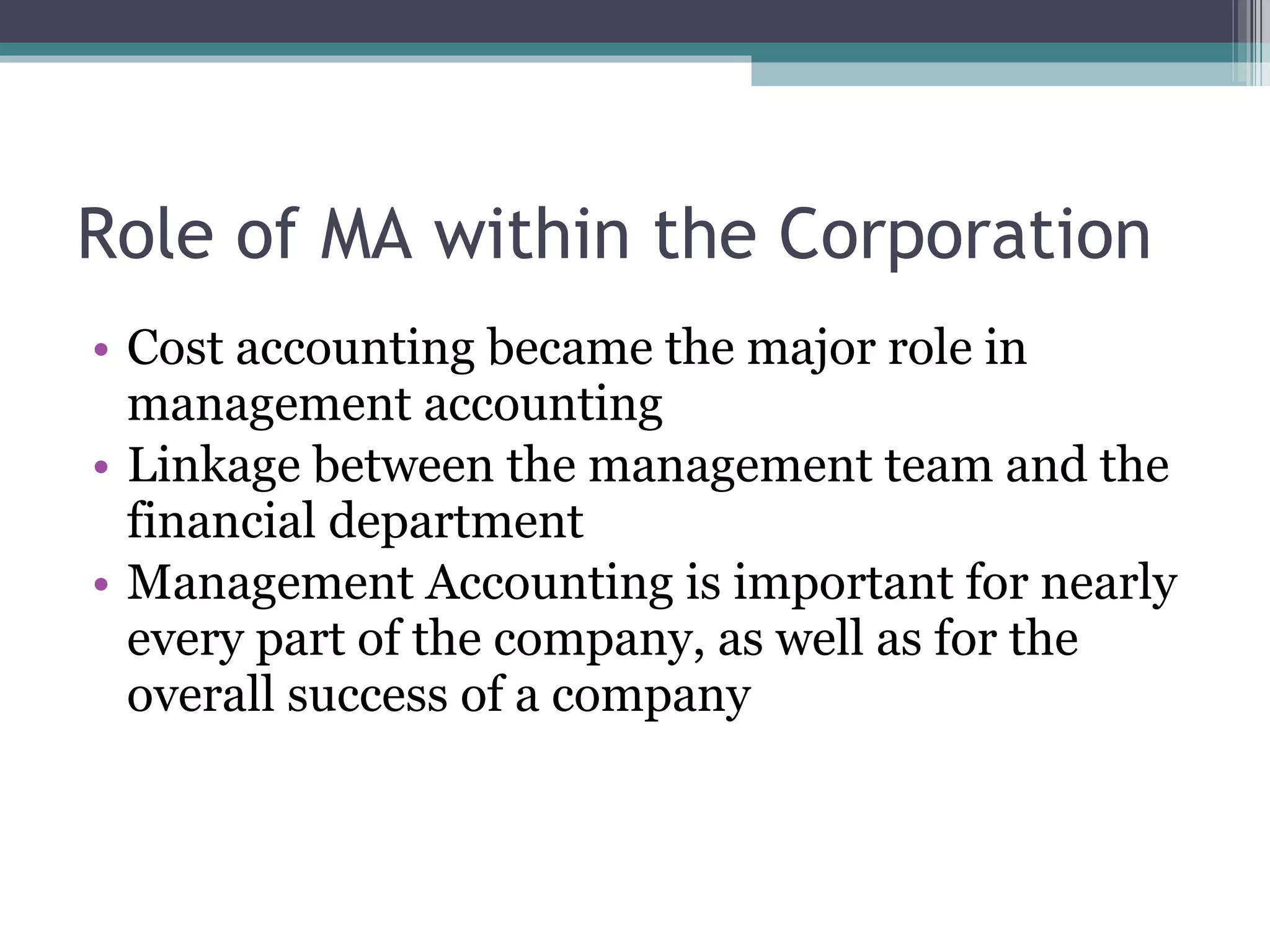

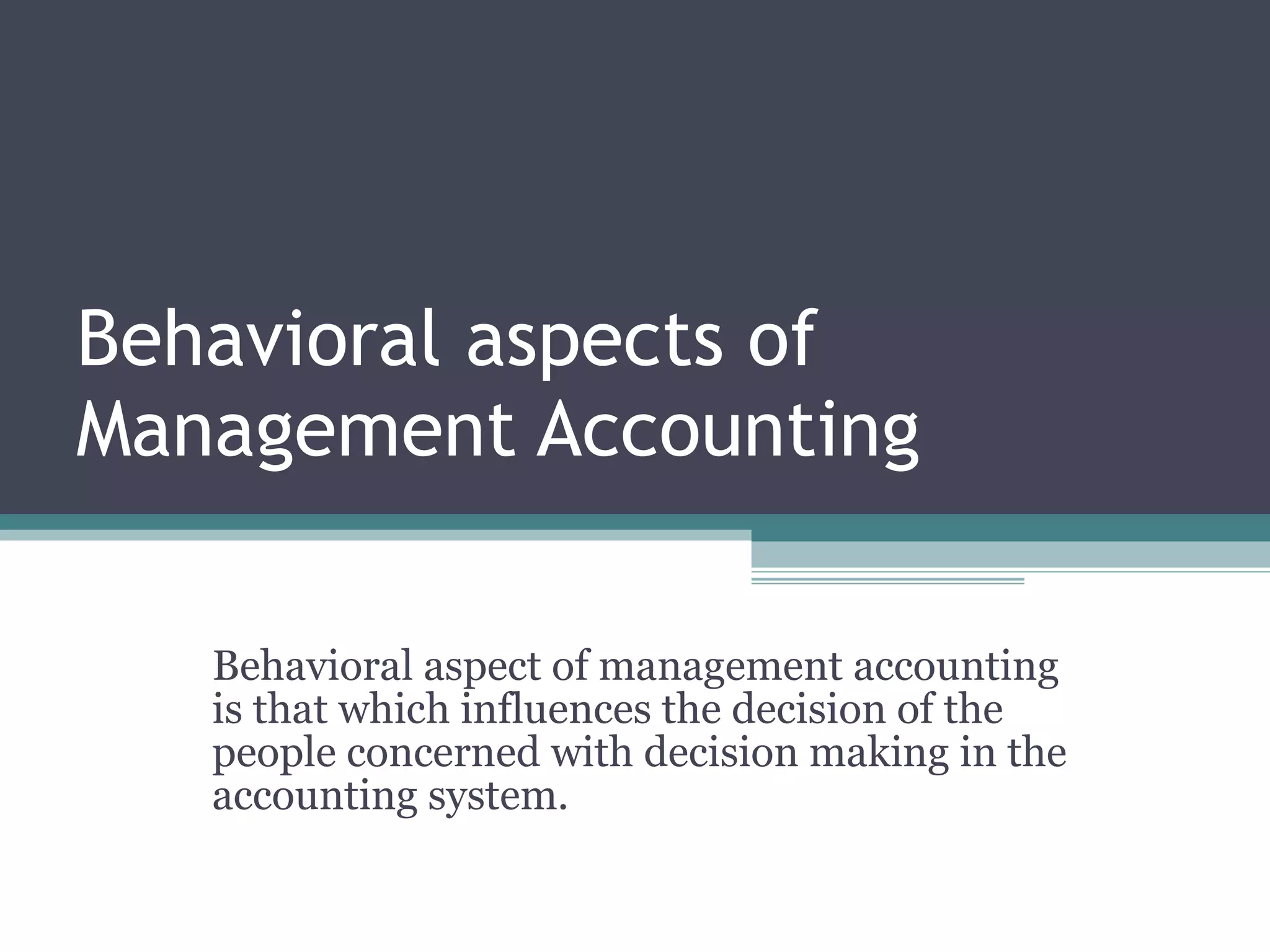

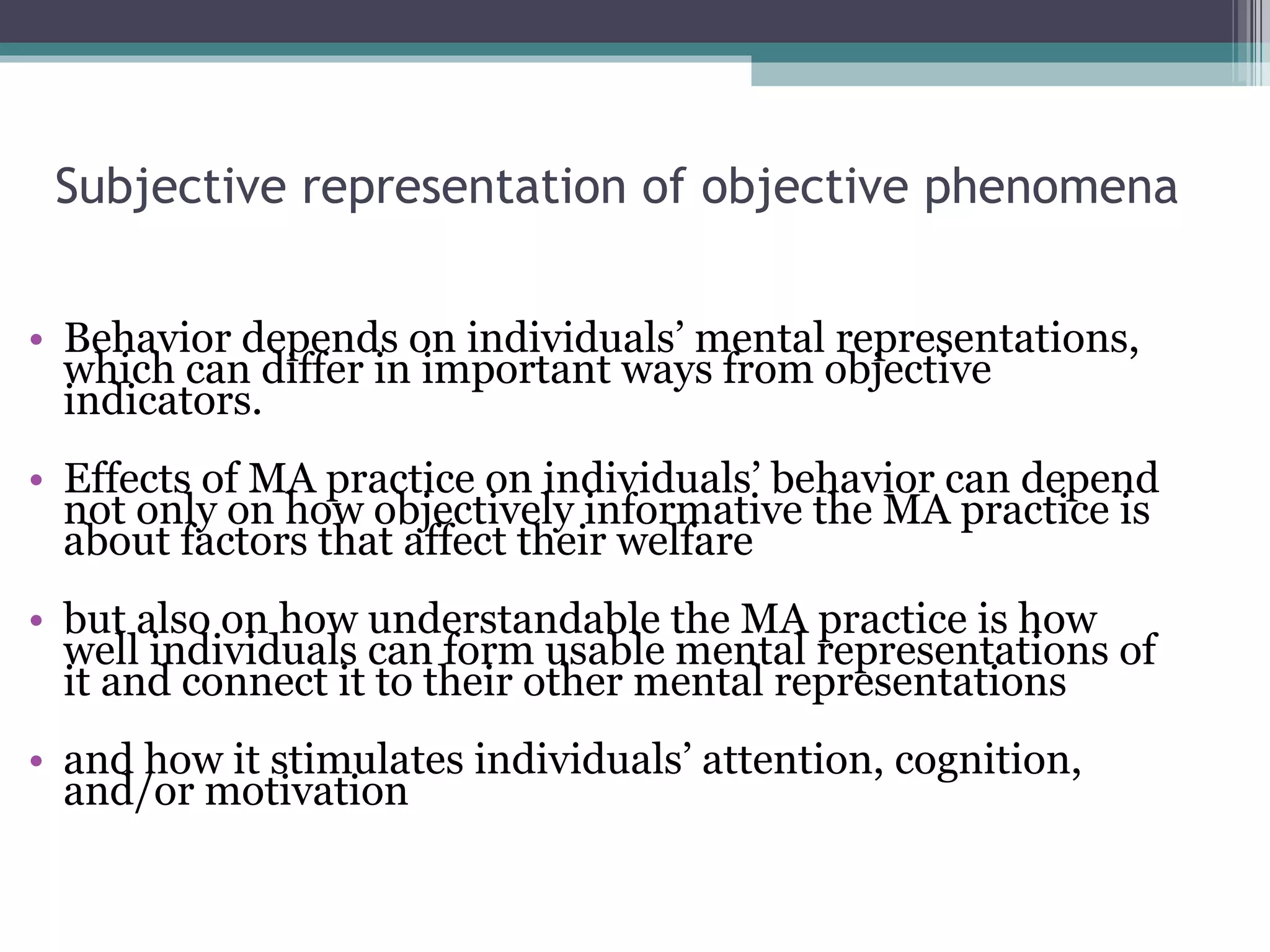

The document discusses behavioral aspects of management accounting. It outlines motivational theories like goal setting theory and organizational justice theory that are relevant to management accounting. It also discusses how management accounting systems can influence employee behavior, both positively and negatively, depending on how the systems are designed and implemented. Management accountants must consider behavioral implications to gain employee acceptance of new systems and avoid unintended consequences.