Downloaded 1,313 times

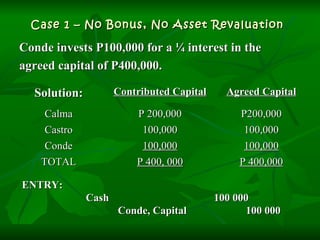

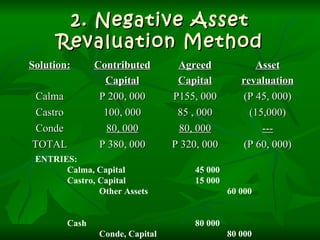

The document discusses the dissolution of partnerships through changes in ownership. It defines dissolution as a change in the relationship between partners caused by any partner ceasing to be involved in the business. Dissolution is distinguished from liquidation, which ends the business operations. Causes of dissolution include the admission, withdrawal, death, or incorporation of a partner. A new partner can be admitted through purchasing an interest from existing partners or investing new assets, with the consent of continuing partners. Accounting entries are provided to record various scenarios of partner admission.

![Oblicon essential notes_2015[1]-1](https://cdn.slidesharecdn.com/ss_thumbnails/obliconessentialnotes20151-1-180120161144-thumbnail.jpg?width=640&height=640&fit=bounds)