Downloaded 123 times

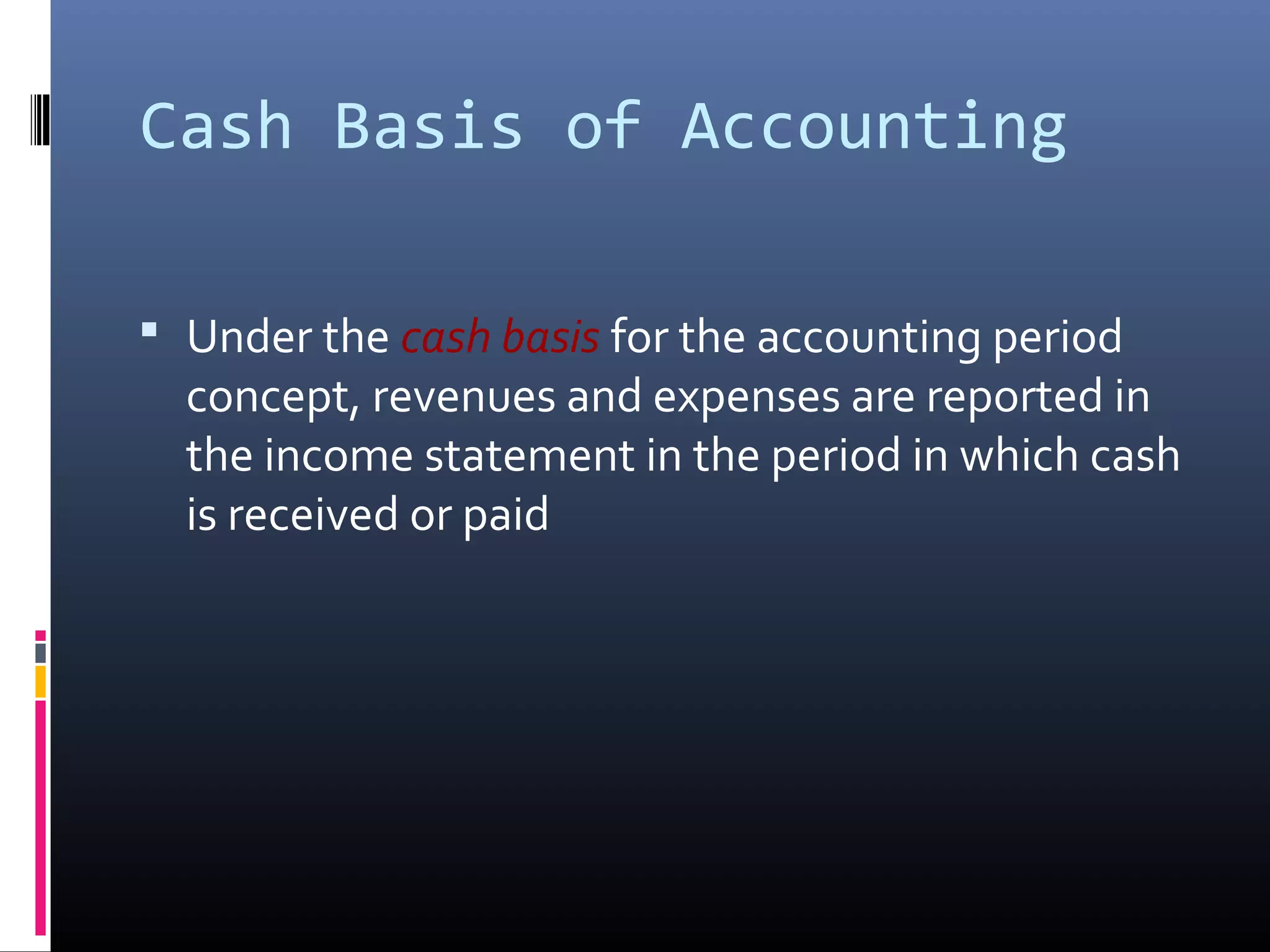

Adjusting entries are journal entries made at the end of an accounting period to allocate revenues and expenses to the appropriate period. This is necessary because under the accrual basis of accounting, revenues are reported in the period they are earned and expenses in the period they are incurred. Some accounts, like prepaid expenses and unearned revenue, require adjustment to adhere to the revenue recognition and matching principles. The document provides examples of accounts that need adjustment, the cash versus accrual accounting methods, and the purpose of adjusting entries in ensuring financial statements reflect the proper period's financial activity.