WHAT IS FINANCIAL

FORECASTING?

Afinancial forecast is a fiscal management tool

that presents estimated information based on

past, current, and projected financial conditions.

3

4.

OBJECTIVES OF FORECASTING

●To reduce cost of responding to emergencies by

anticipating the future occurrences

● Prepare to take advantage of future

opportunities

● Prepare contingency and emergency plans

● Prepare to deal with the possible outcomes

4

6

Decide what needsto be forecast

Evaluate and analyze appropriate data

Select and test the forecasting model

Generate the forecast

Monitor the forecast accuracy overtime

Historical data from

timeseries or

correlation

information

8

Opinions from

experts, decision

makers, or

customers

QUANTITAT

IVE

QUALITATIV

E

TWO GENERAL CATEGORIES OF

FORECASTING

9.

9

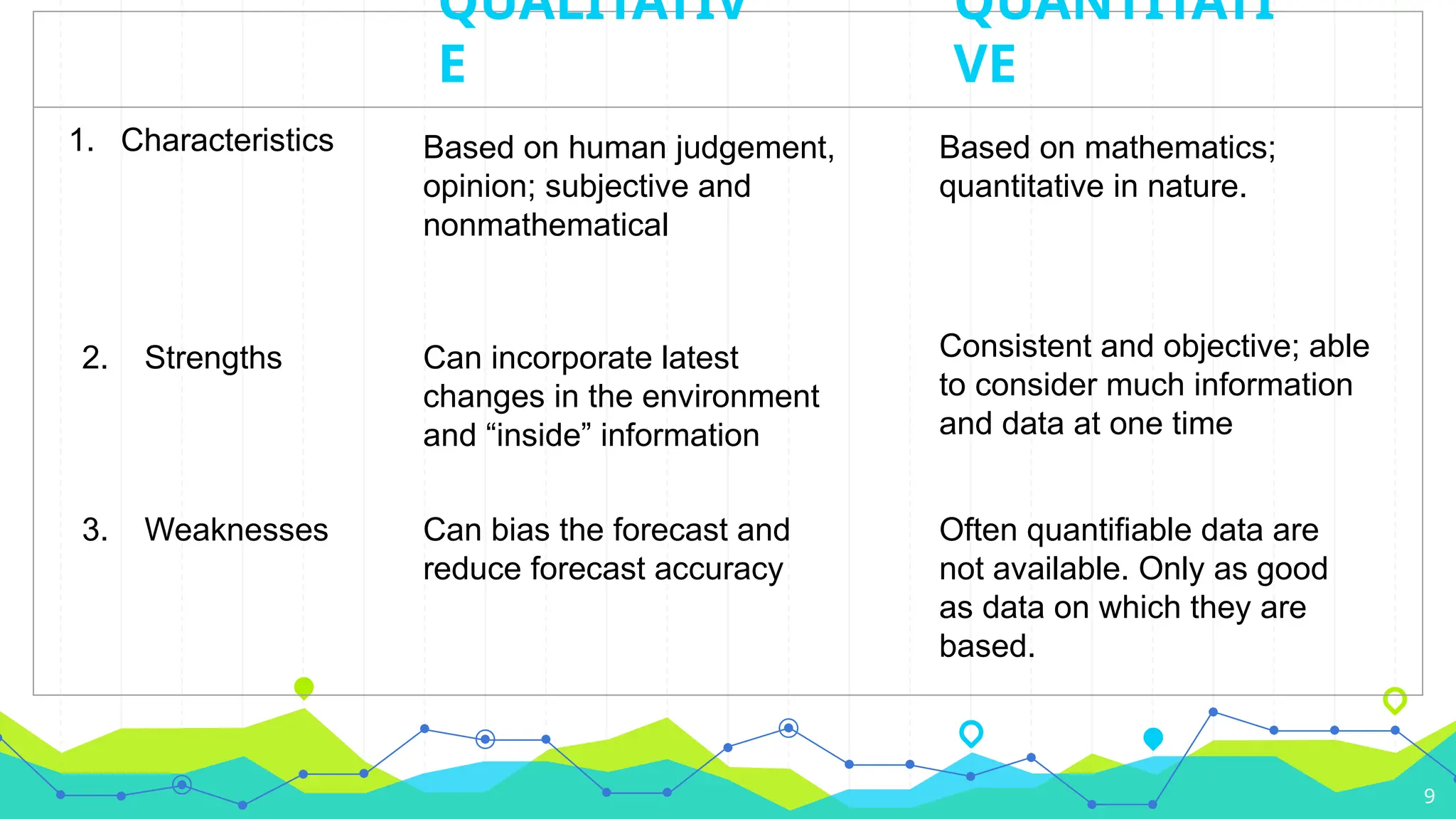

1. Characteristics Basedon human judgement,

opinion; subjective and

nonmathematical

Based on mathematics;

quantitative in nature.

2. Strengths Can incorporate latest

changes in the environment

and “inside” information

Consistent and objective; able

to consider much information

and data at one time

3. Weaknesses Can bias the forecast and

reduce forecast accuracy

Often quantifiable data are

not available. Only as good

as data on which they are

based.

QUANTITATI

VE

QUALITATIV

E

11

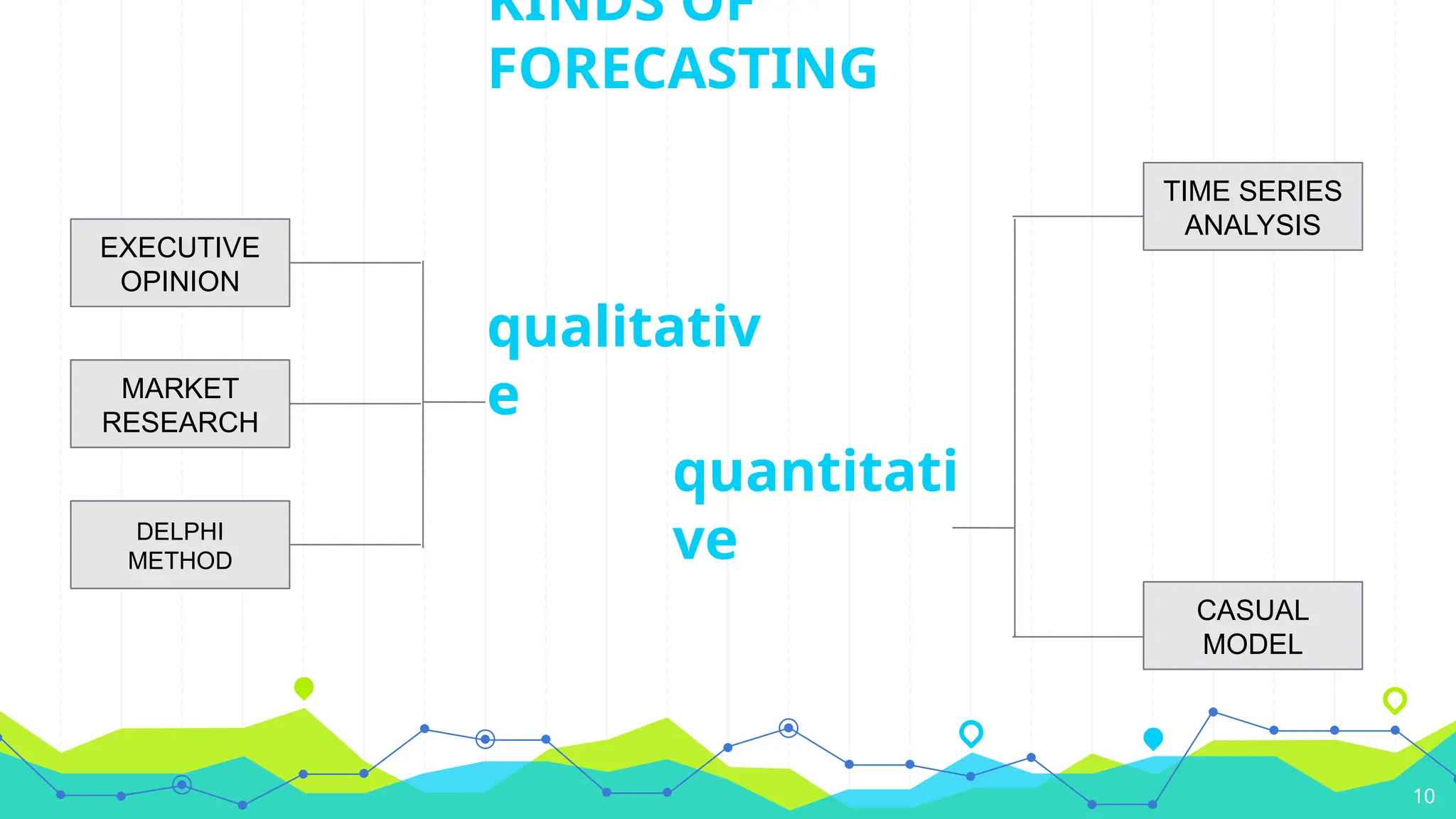

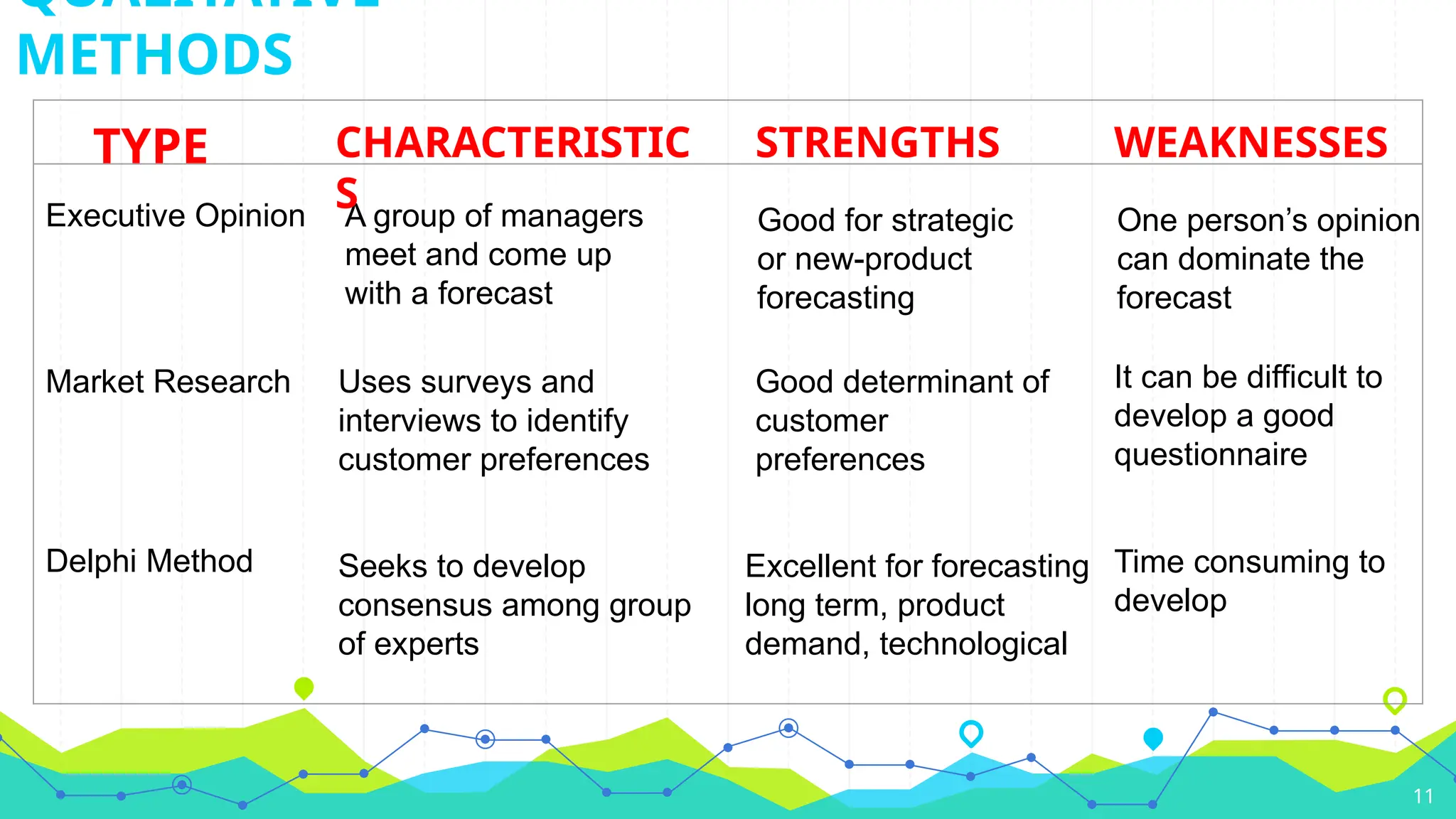

QUALITATIVE

METHODS

A group ofmanagers

meet and come up

with a forecast

Good for strategic

or new-product

forecasting

Market Research Uses surveys and

interviews to identify

customer preferences

Good determinant of

customer

preferences

Delphi Method Seeks to develop

consensus among group

of experts

Excellent for forecasting

long term, product

demand, technological

TYPE CHARACTERISTIC

S

STRENGTHS WEAKNESSES

Executive Opinion One person’s opinion

can dominate the

forecast

It can be difficult to

develop a good

questionnaire

Time consuming to

develop

12.

12

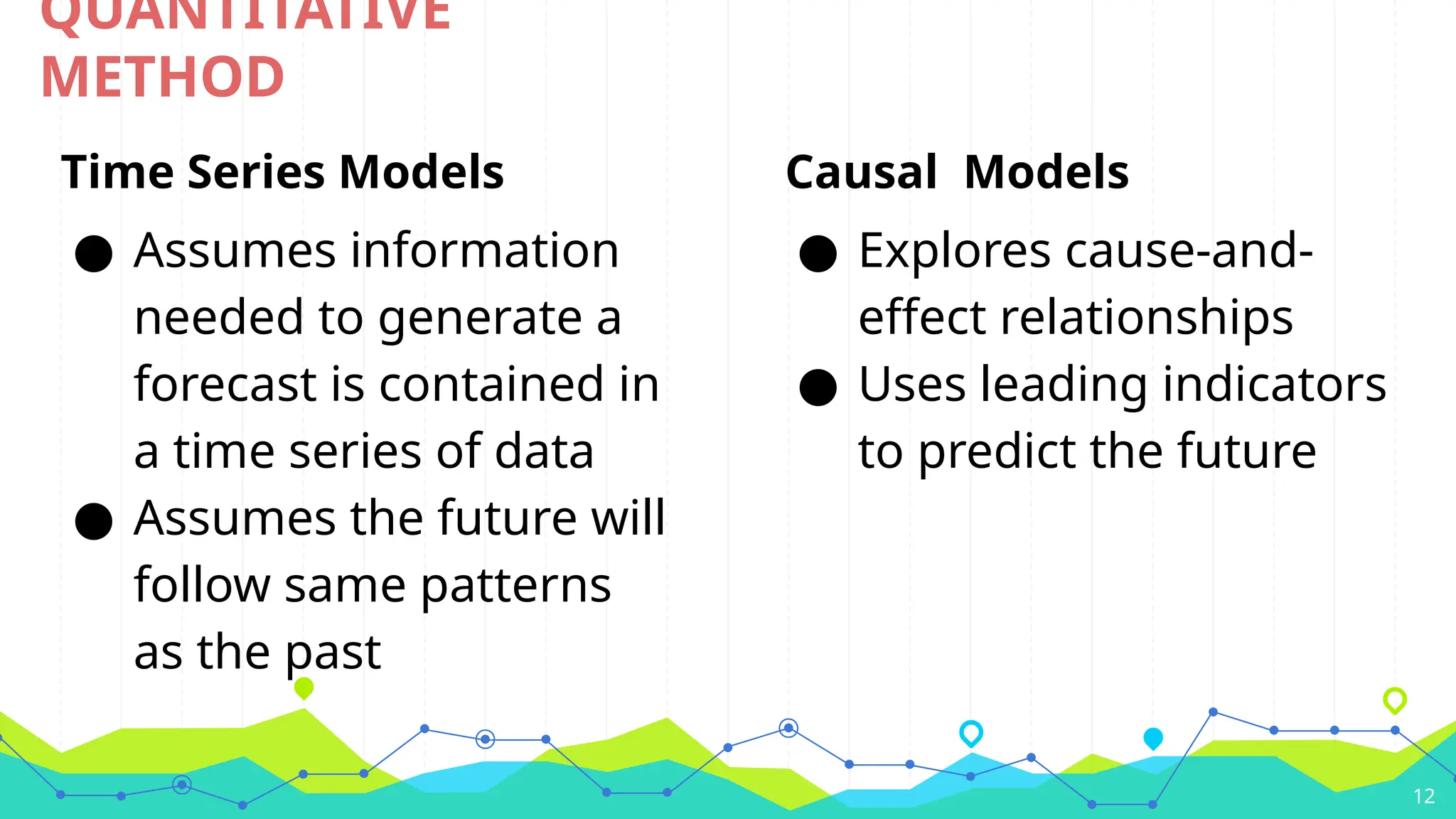

QUANTITATIVE

METHOD

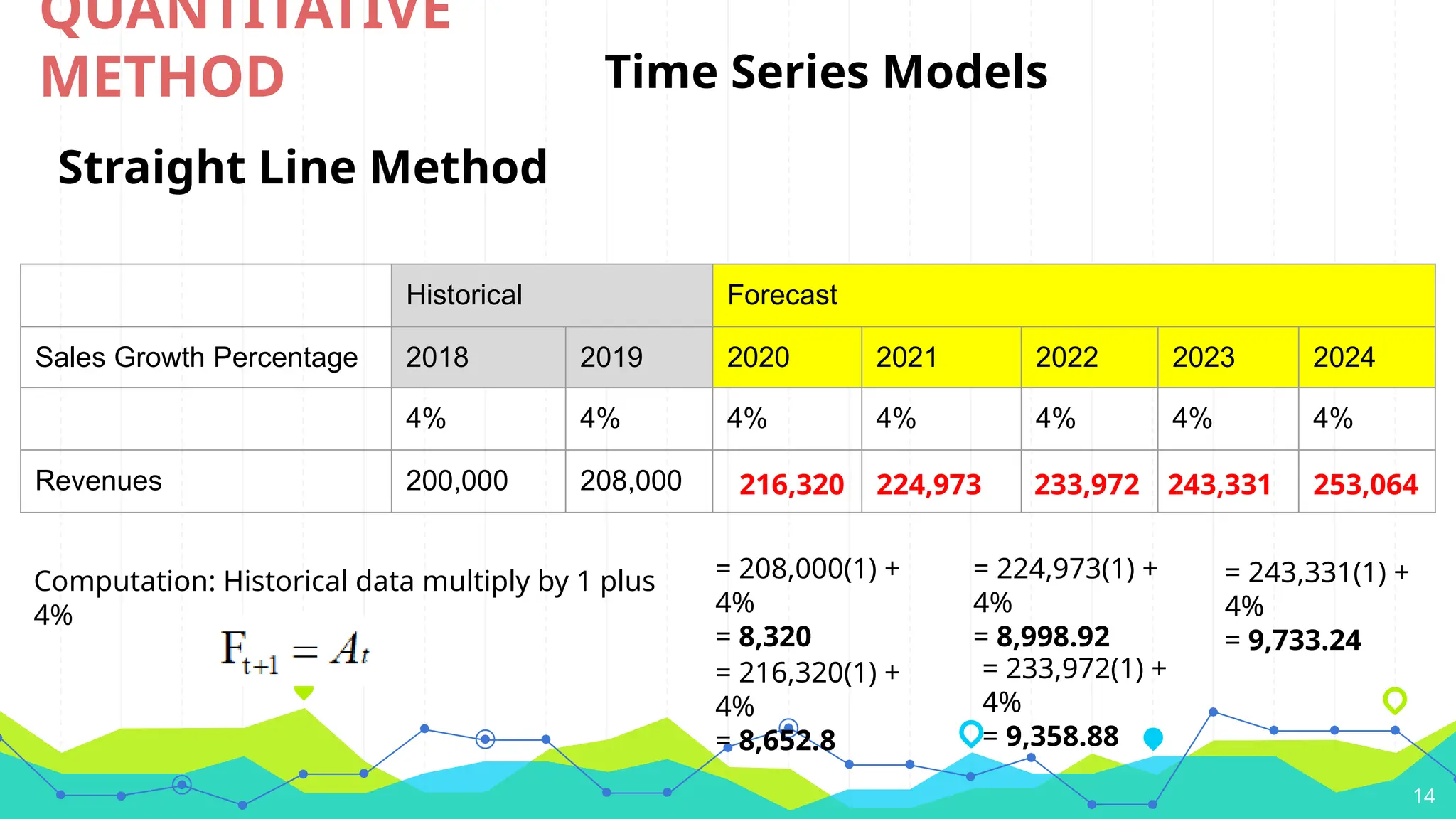

Time Series Models

●Assumes information

needed to generate a

forecast is contained in

a time series of data

● Assumes the future will

follow same patterns

as the past

Causal Models

● Explores cause-and-

effect relationships

● Uses leading indicators

to predict the future

15

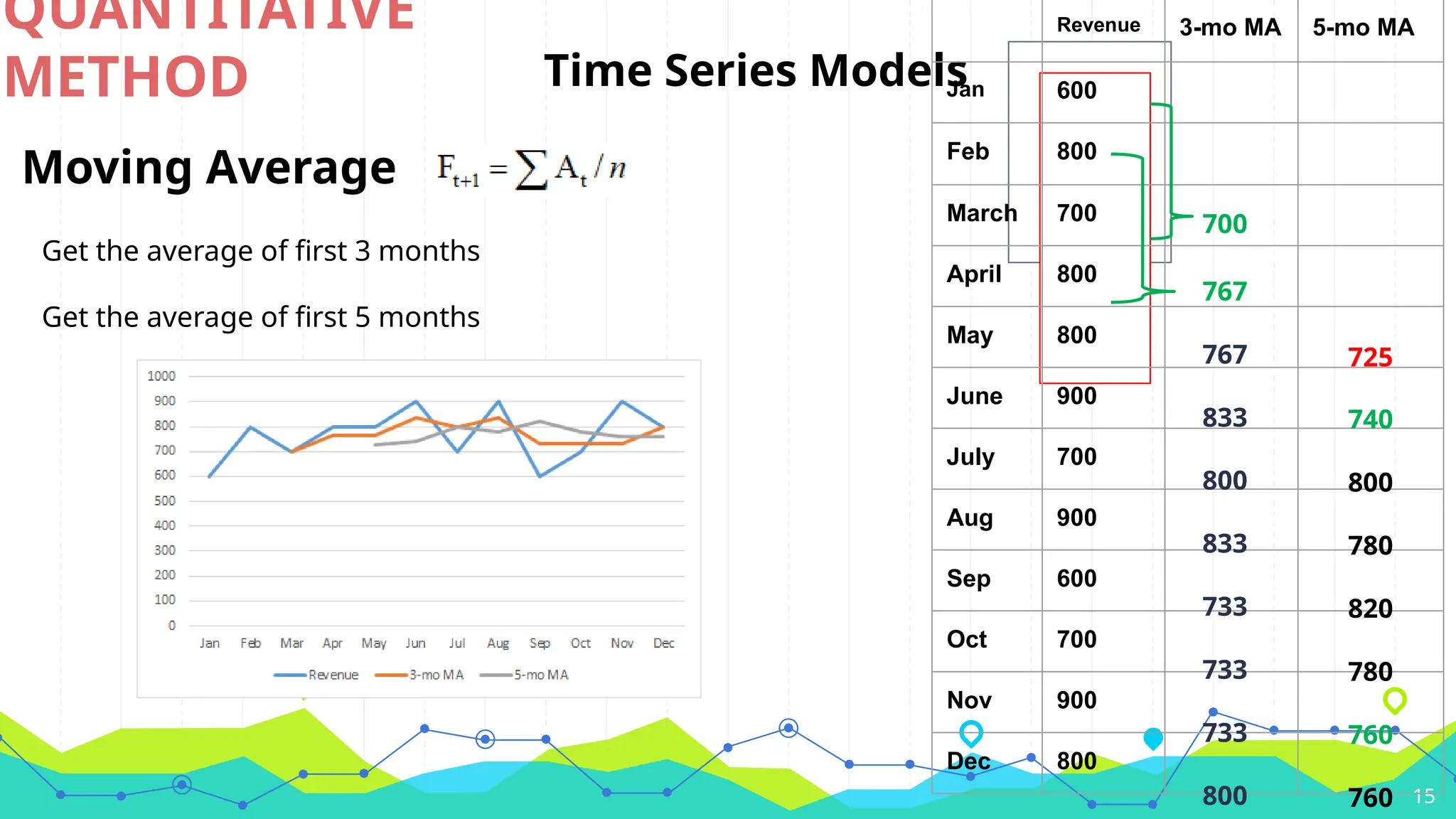

QUANTITATIVE

METHOD Time SeriesModels

Moving Average

Revenue 3-mo MA 5-mo MA

Jan 600

Feb 800

March 700

April 800

May 800

June 900

July 700

Aug 900

Sep 600

Oct 700

Nov 900

Dec 800

Get the average of first 3 months

700

Get the average of first 5 months

725

767

767

833

800

833

733

733

733

800

740

800

780

820

780

760

760

16.

16

QUANTITATIVE

METHOD

Causal Models

● Acommon tool of causal modeling is linear

regression:

● Casual models establish a cause-and-effect

relationship between independent and dependent

variables

17.

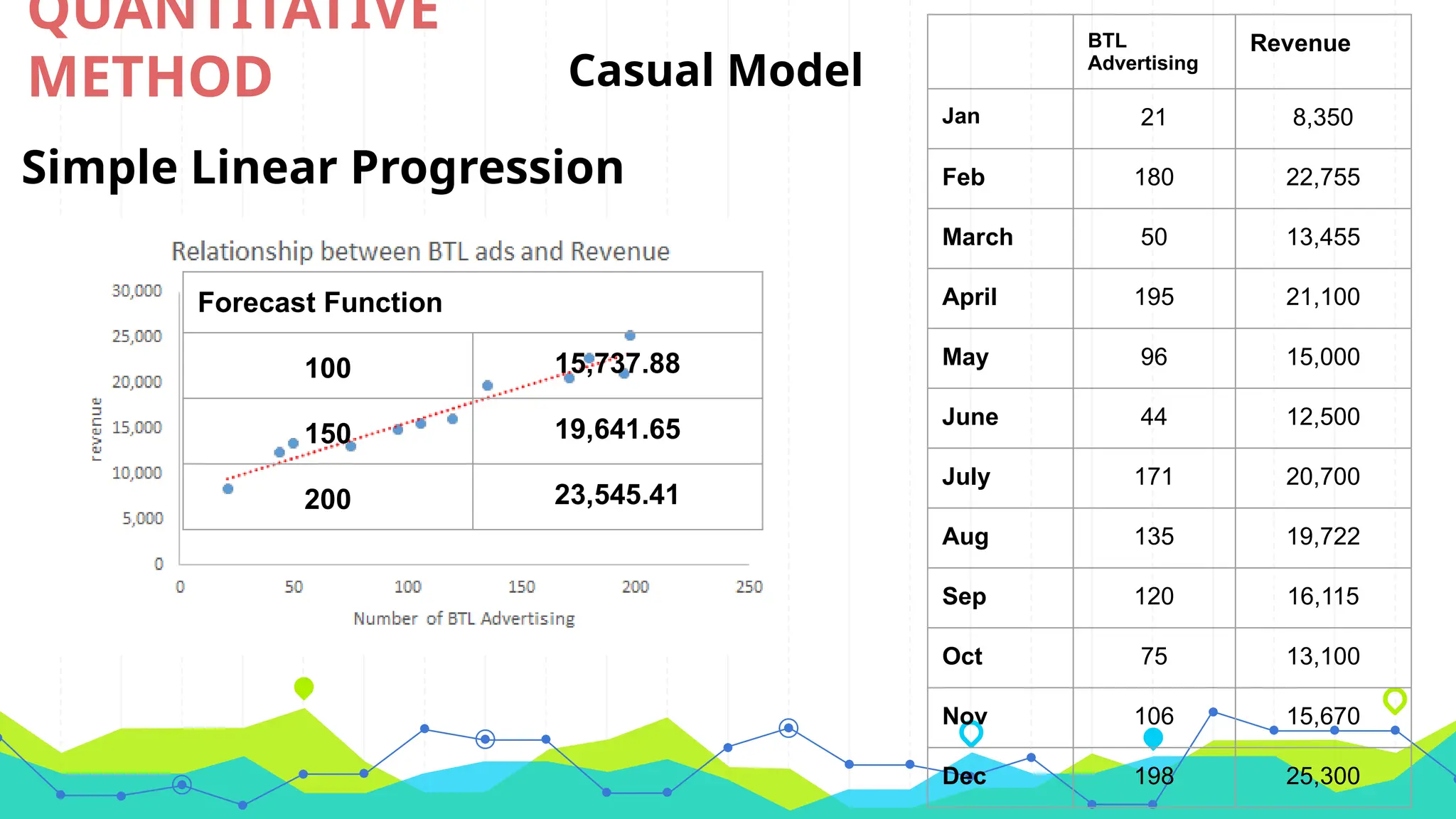

QUANTITATIVE

METHOD Casual Model

SimpleLinear Progression

BTL

Advertising

Revenue

Jan 21 8,350

Feb 180 22,755

March 50 13,455

April 195 21,100

May 96 15,000

June 44 12,500

July 171 20,700

Aug 135 19,722

Sep 120 16,115

Oct 75 13,100

Nov 106 15,670

Dec 198 25,300

Forecast Function

100 15,737.88

150 19,641.65

200 23,545.41

WHAT IS FINANCIALPLANNING?

Financial Planning is the process of estimating the

capital required and determining its competition. It is

the process of framing financial policies in relation to

procurement, investment and administration of funds

of an enterprise.

19

20.

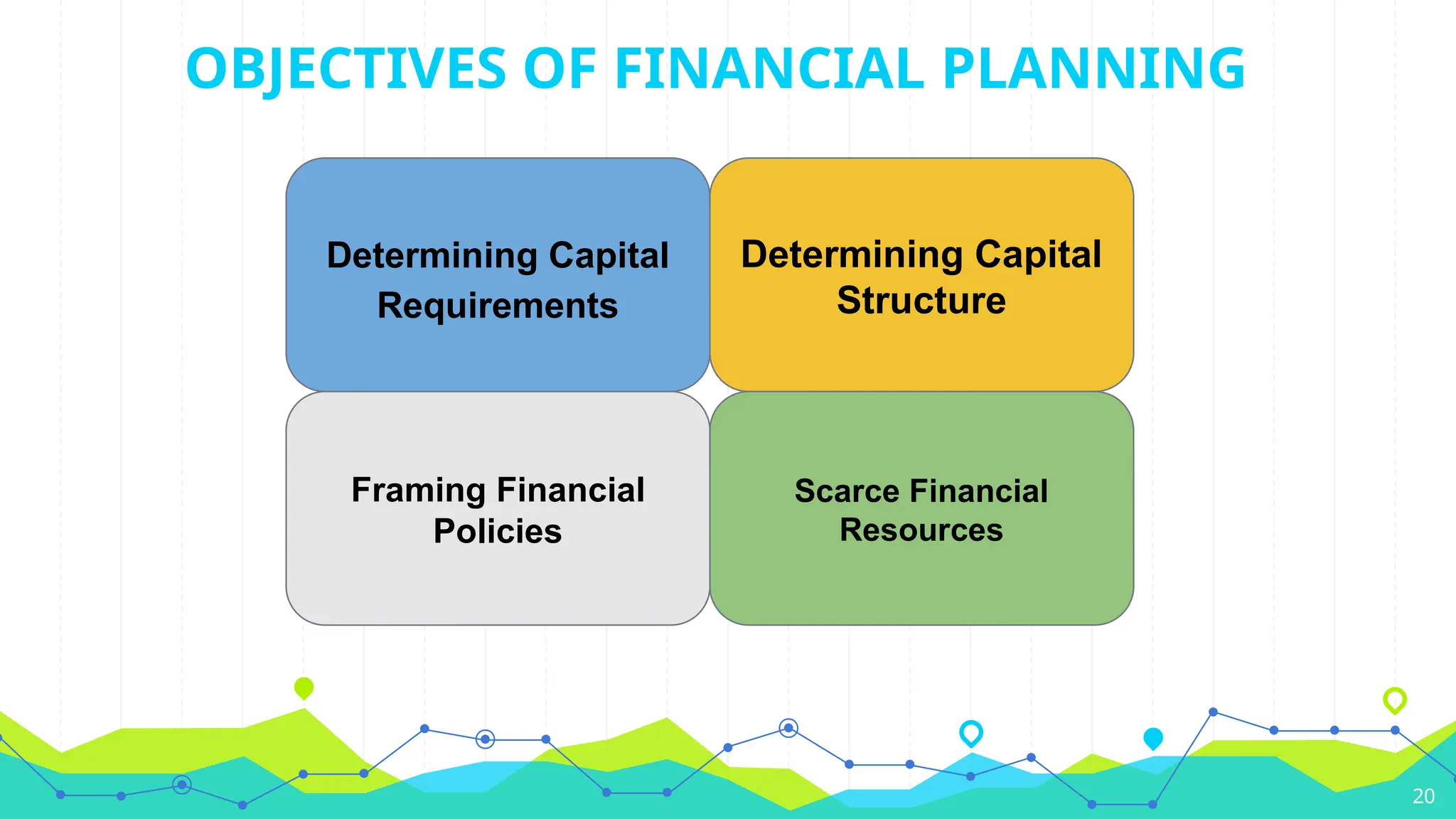

OBJECTIVES OF FINANCIALPLANNING

20

Determining Capital

Requirements

Determining Capital

Structure

Framing Financial

Policies

Scarce Financial

Resources

21.

IMPORTANCE OF FINANCIAL

PLANNING

1.Adequate funds have to be ensured.

2. Helps in ensuring a reasonable balance between outflow

and inflow of funds so that stability is maintained.

3. Ensures that the suppliers of funds are easily investing

in companies which exercise financial planning.

21

22.

IMPORTANCE OF FINANCIAL

PLANNING

4.Helps in making growth and expansion programmes which

helps in long-run survival of the company.

5. Reduces uncertainties with regards to changing market trends

which can be faced easily through enough funds.

6. Helps in reducing the uncertainties which can be a hindrance

to growth of the company. This helps in ensuring stability and

profitability in concern.

22

24

WHAT IS FINANCIALPROCEDURES?

Financial procedures are a set of instructions that any

stakeholder, including new members of the committee or staff,

can use to find out exactly: what tasks need to be done; who will

do these tasks; and who will ensure the tasks are done properly.

25.

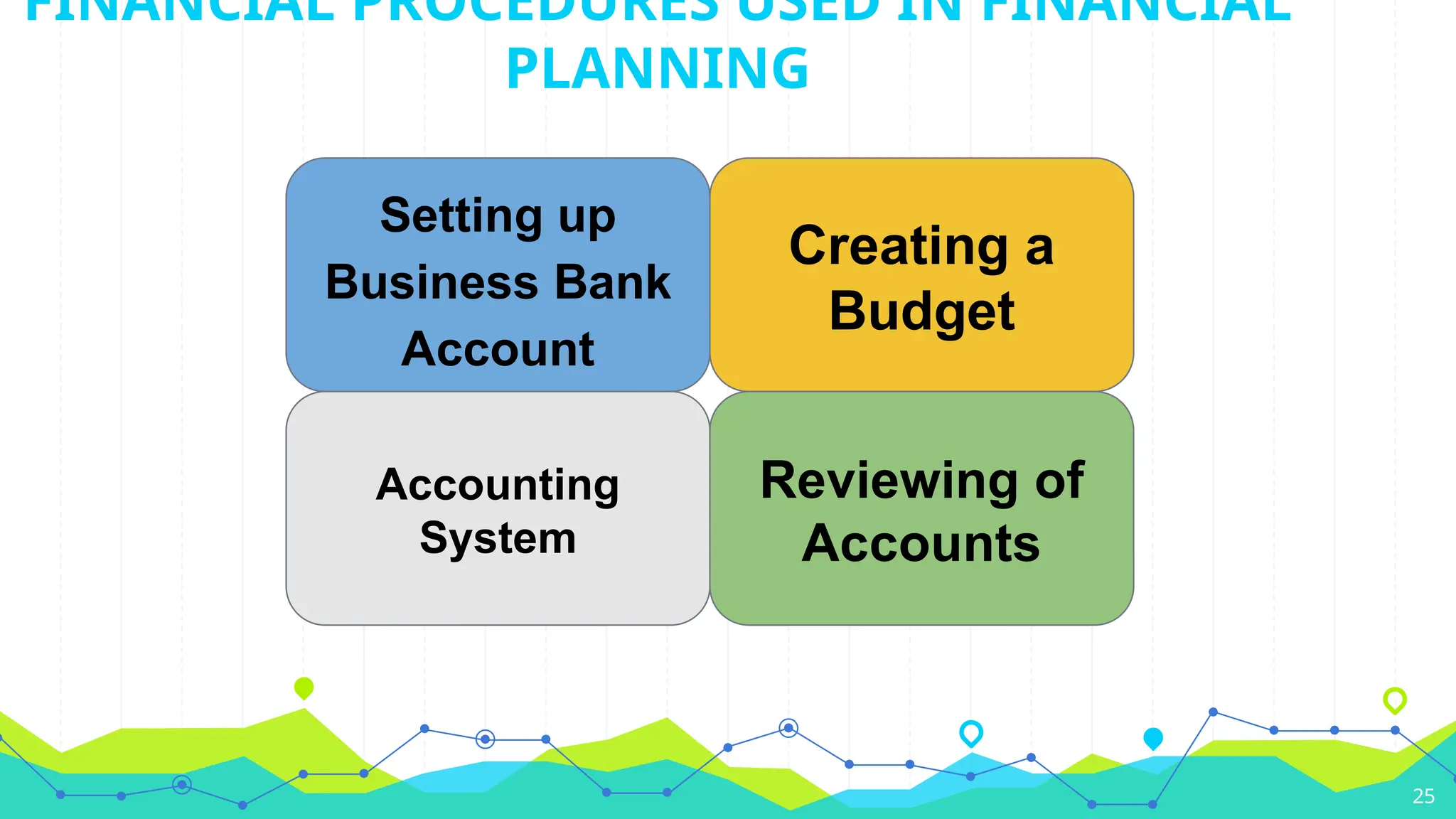

FINANCIAL PROCEDURES USEDIN FINANCIAL

PLANNING

25

Setting up

Business Bank

Account

Creating a

Budget

Accounting

System

Reviewing of

Accounts

27

FINANCIAL CONTROL

● Theprocedures, policies, and means by which an organization

monitors and controls the direction, allocation, and usage of its

financial resources.

● It is the very core of resource management and operational

efficiency in any organization.

30

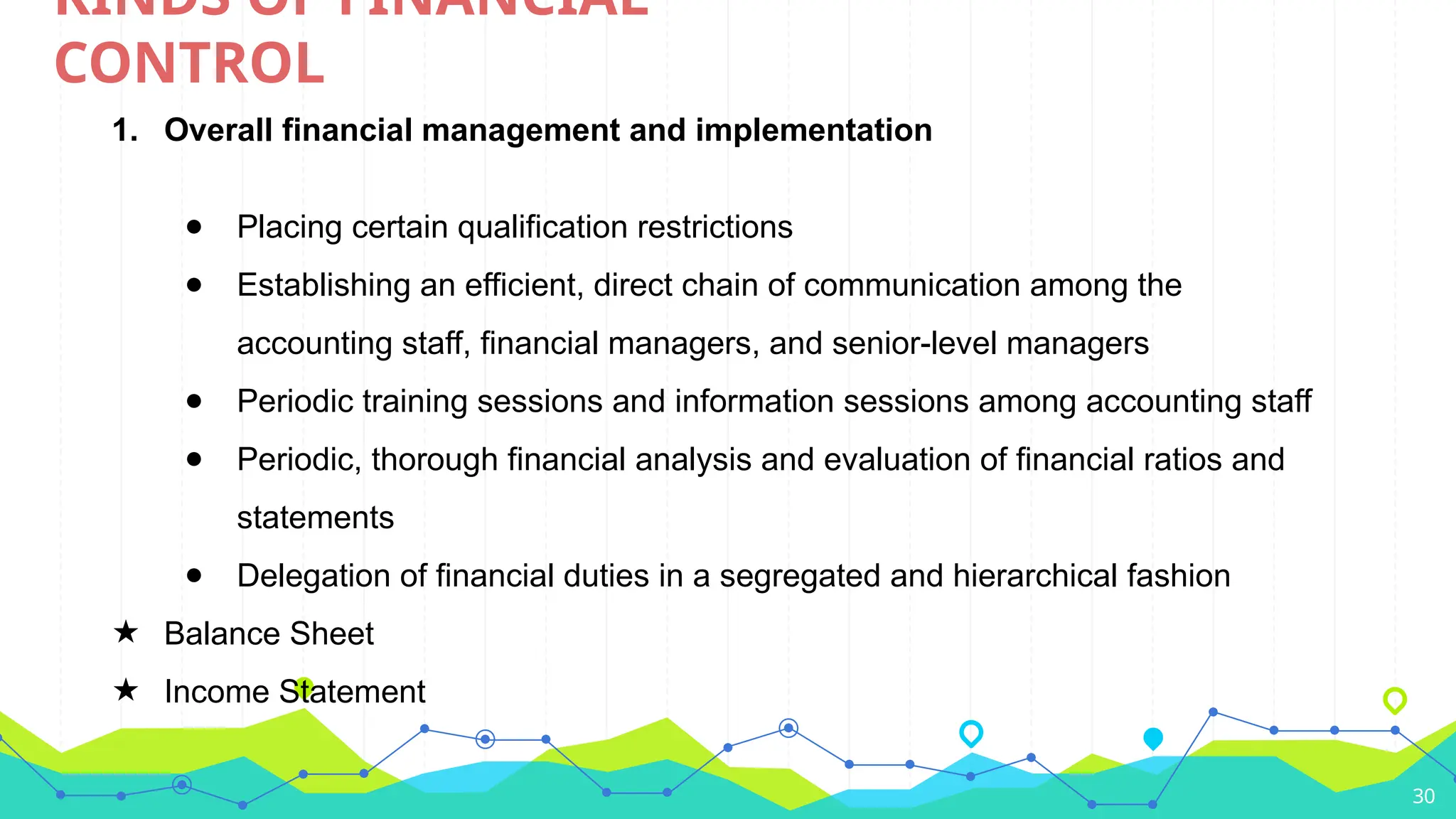

KINDS OF FINANCIAL

CONTROL

1.Overall financial management and implementation

● Placing certain qualification restrictions

● Establishing an efficient, direct chain of communication among the

accounting staff, financial managers, and senior-level managers

● Periodic training sessions and information sessions among accounting staff

● Periodic, thorough financial analysis and evaluation of financial ratios and

statements

● Delegation of financial duties in a segregated and hierarchical fashion

★ Balance Sheet

★ Income Statement

31.

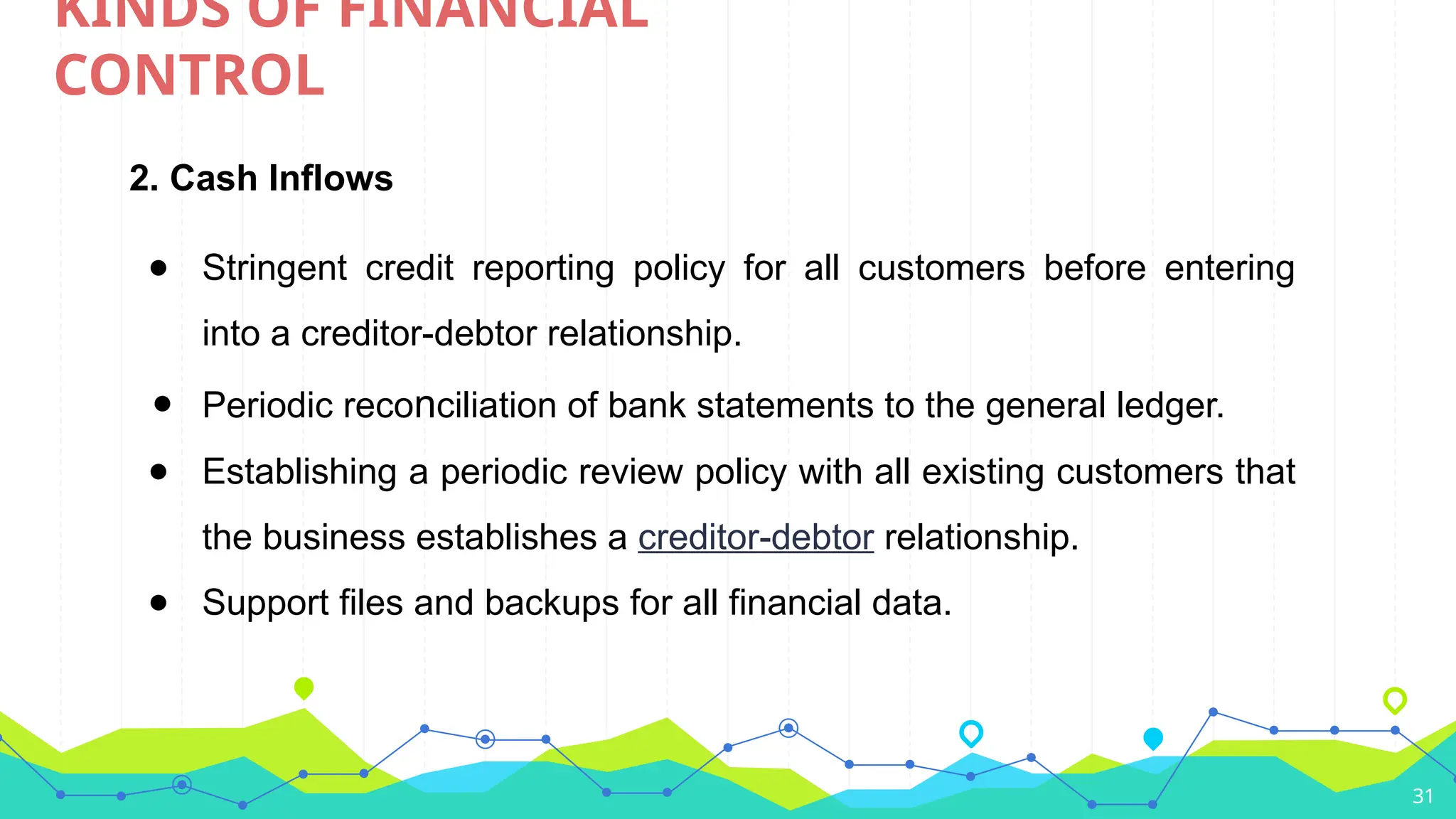

2. Cash Inflows

●Stringent credit reporting policy for all customers before entering

into a creditor-debtor relationship.

● Periodic reconciliation of bank statements to the general ledger.

● Establishing a periodic review policy with all existing customers that

the business establishes a creditor-debtor relationship.

● Support files and backups for all financial data.

31

KINDS OF FINANCIAL

CONTROL

32.

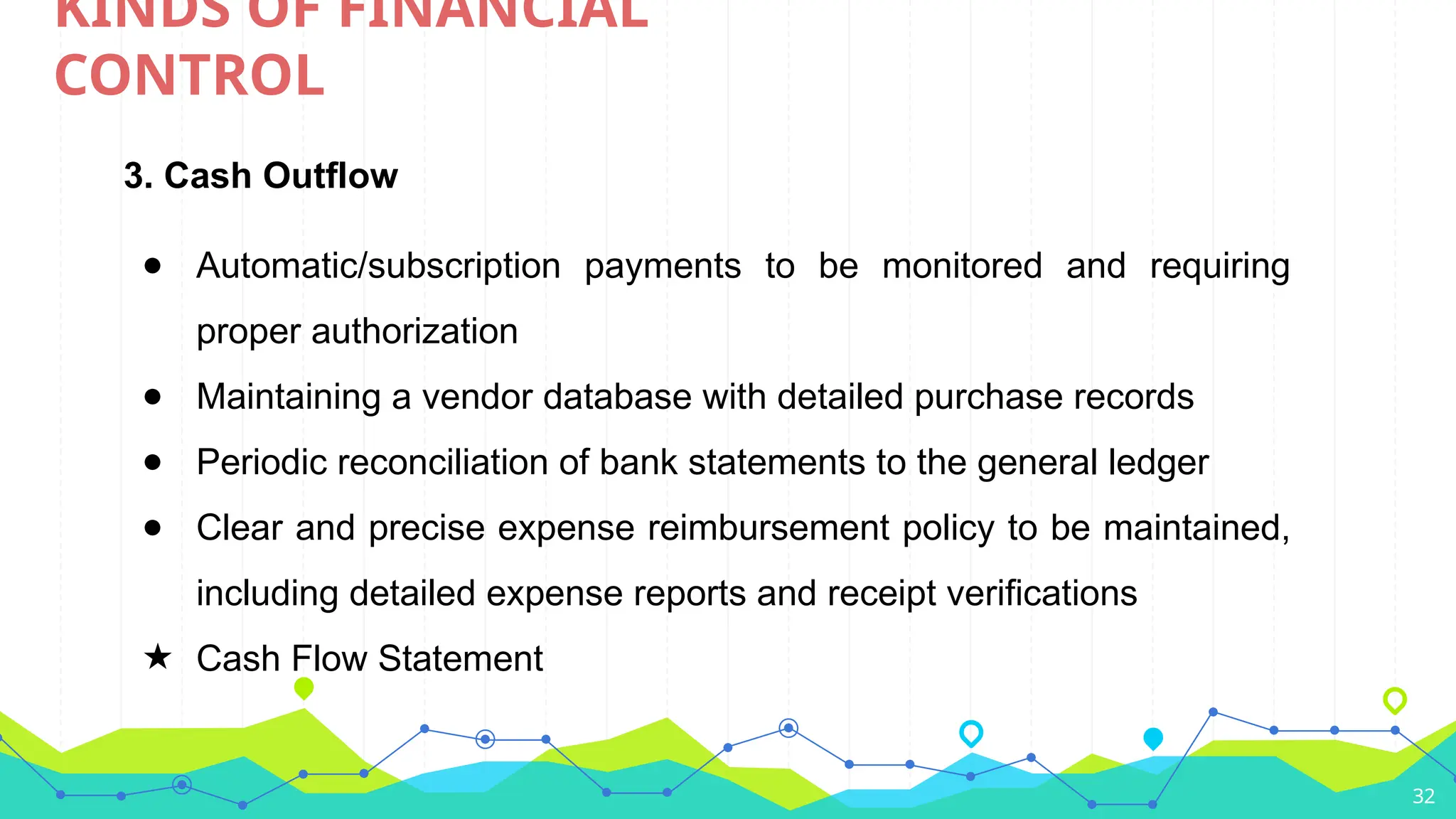

3. Cash Outflow

●Automatic/subscription payments to be monitored and requiring

proper authorization

● Maintaining a vendor database with detailed purchase records

● Periodic reconciliation of bank statements to the general ledger

● Clear and precise expense reimbursement policy to be maintained,

including detailed expense reports and receipt verifications

★ Cash Flow Statement

32

KINDS OF FINANCIAL

CONTROL

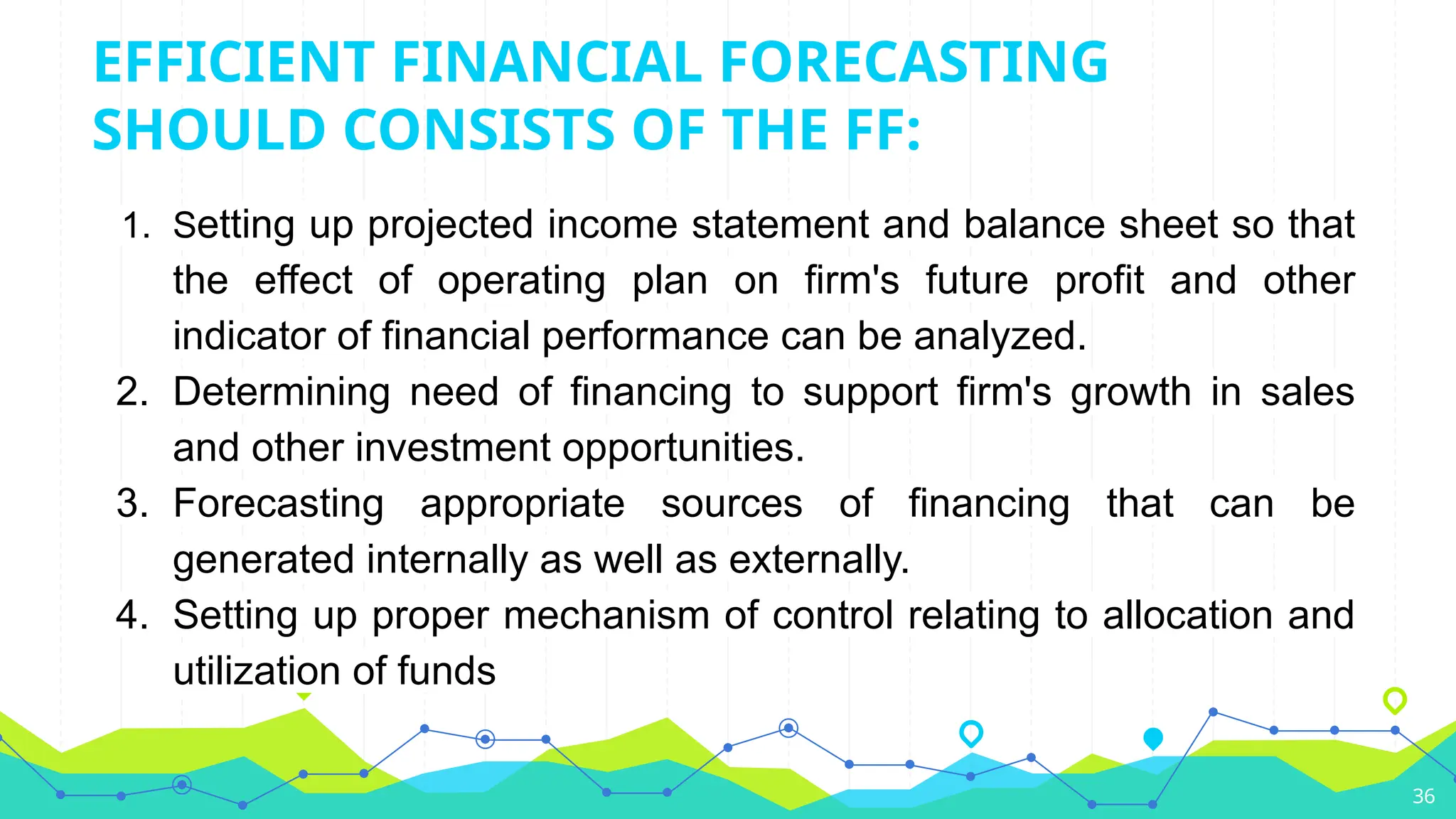

EFFICIENT FINANCIAL FORECASTING

SHOULDCONSISTS OF THE FF:

1. Setting up projected income statement and balance sheet so that

the effect of operating plan on firm's future profit and other

indicator of financial performance can be analyzed.

2. Determining need of financing to support firm's growth in sales

and other investment opportunities.

3. Forecasting appropriate sources of financing that can be

generated internally as well as externally.

4. Setting up proper mechanism of control relating to allocation and

utilization of funds

36

37.

● The appropriategoal for the financial manager is

to increase the market value of the owner’s equity

and not just growth.

● Growth may thus be a desirable consequence of

good decision making but it is not an end unto

itself.

37

GROWTH AS FINANCIAL

MANAGEMENT GOAL

38.

● It helpsto set the standard of performances and act as a

base to evaluate real-time results.

● It helps in the timely arrangement of funds as a result of

the financial projection of funds needs and revenue

potential.

● It helps in the optimum utilization of resources and reduces

the non-performing resources of the organization.

38

BENEFITS OF FINANCIAL

FORECASTING

● Forecasting providesrelevant and reliable information about the past

and present events and likely the future events.

● It gives confidence to the managers for making important decisions.

● It is the basis for making planning premises.

● It keeps managers active and alert to face the challenges of the

future events and the changes in environment.

40

41.

1. Financial ForecastsCreate a Clear Path to Achieve

Your Goals

2. A Financial Forecast Creates Trust and Confidence

in Raising Funds

3. A Financial Forecast Tells you What Resources

You Need (and When)

41

3 REASONS WHY YOU NEED A FINANCIAL

FORECAST:

43

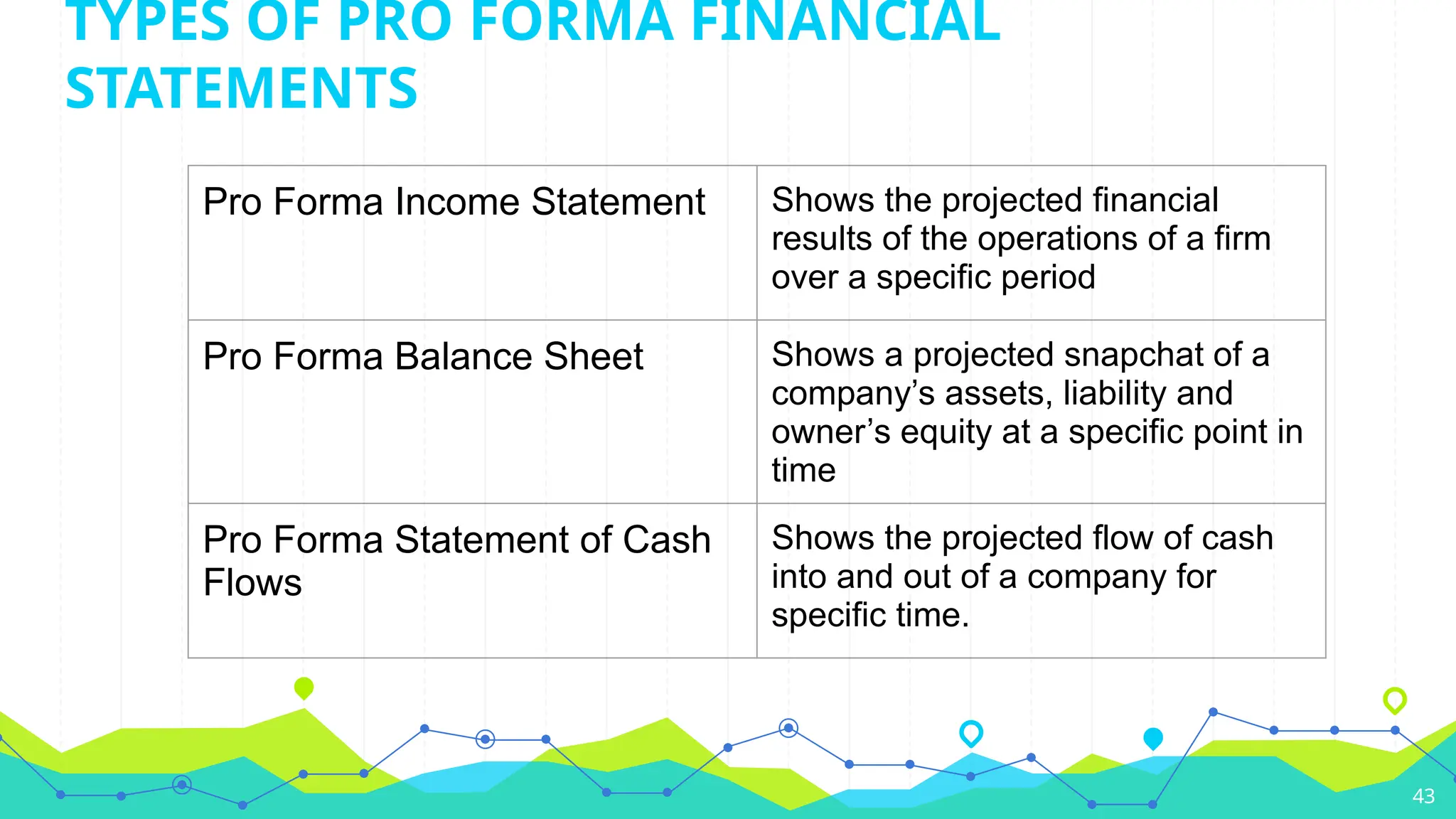

Pro Forma IncomeStatement Shows the projected financial

results of the operations of a firm

over a specific period

Pro Forma Balance Sheet Shows a projected snapchat of a

company’s assets, liability and

owner’s equity at a specific point in

time

Pro Forma Statement of Cash

Flows

Shows the projected flow of cash

into and out of a company for

specific time.

TYPES OF PRO FORMA FINANCIAL

STATEMENTS

44.

1. The futureprofitability based on projected sales level

2. How much and what type financing will be needed.

3. Whether the firm will have adequate cash flows.

44

PURPOSE OF PRO FORMA FINANCIAL

STATEMENTS

45.

45

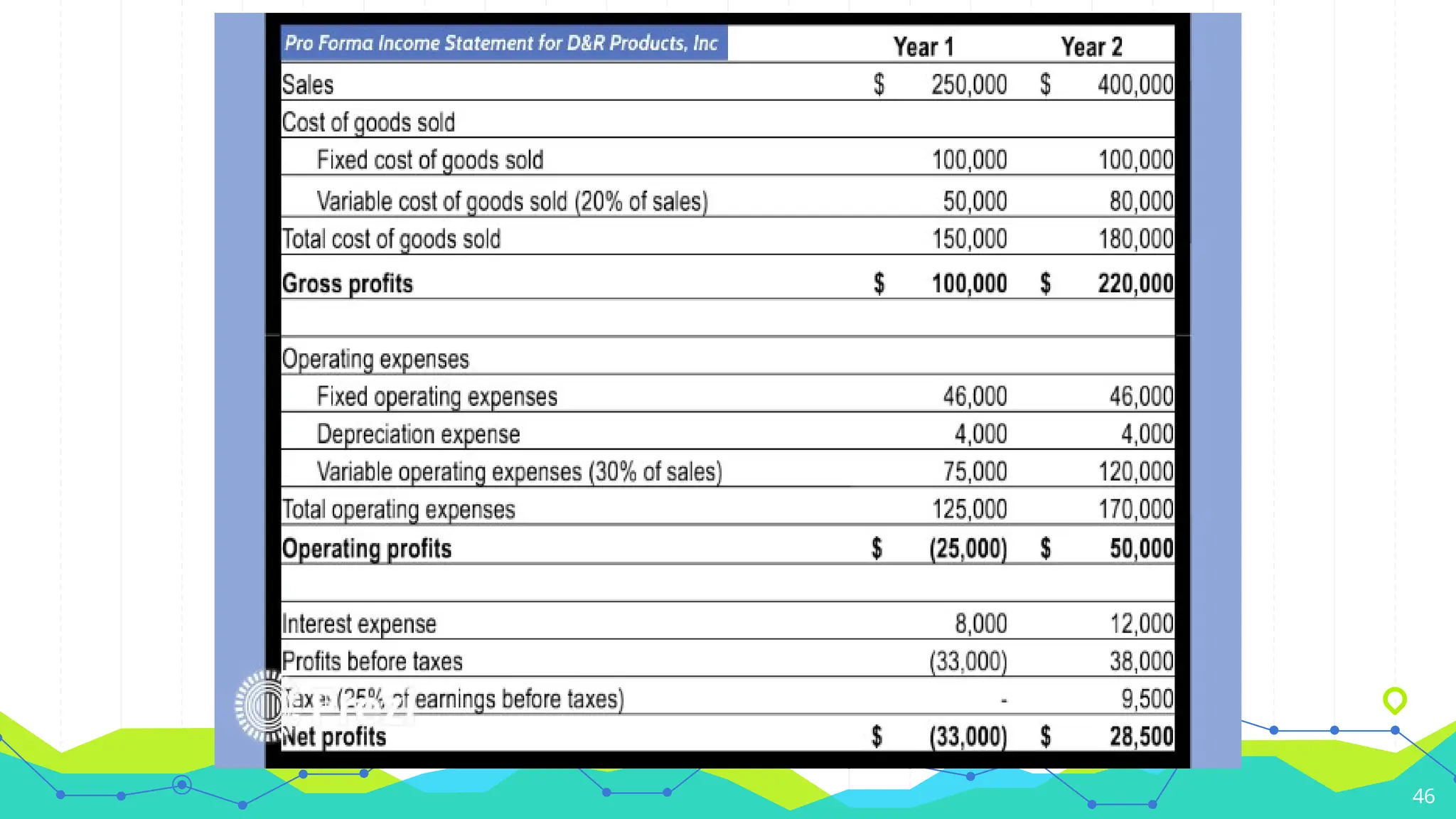

Develop a proforma income statement to forecast a new venture’s profitability

● Amount of Sales= Price x Number units sold

❏ Much that we project about a company's financial future is driven by the

assumptions we make regarding future sales

● Cost of Good Sold= cost producing the firm's products

(fixed or variable)

● Operating Expenses= expenses relate to marketing and

distributing the product.

● Interest expense= interest on loan principal

● Taxes= figured as a percentage of taxable income

FORECASTING PROFITABILITY

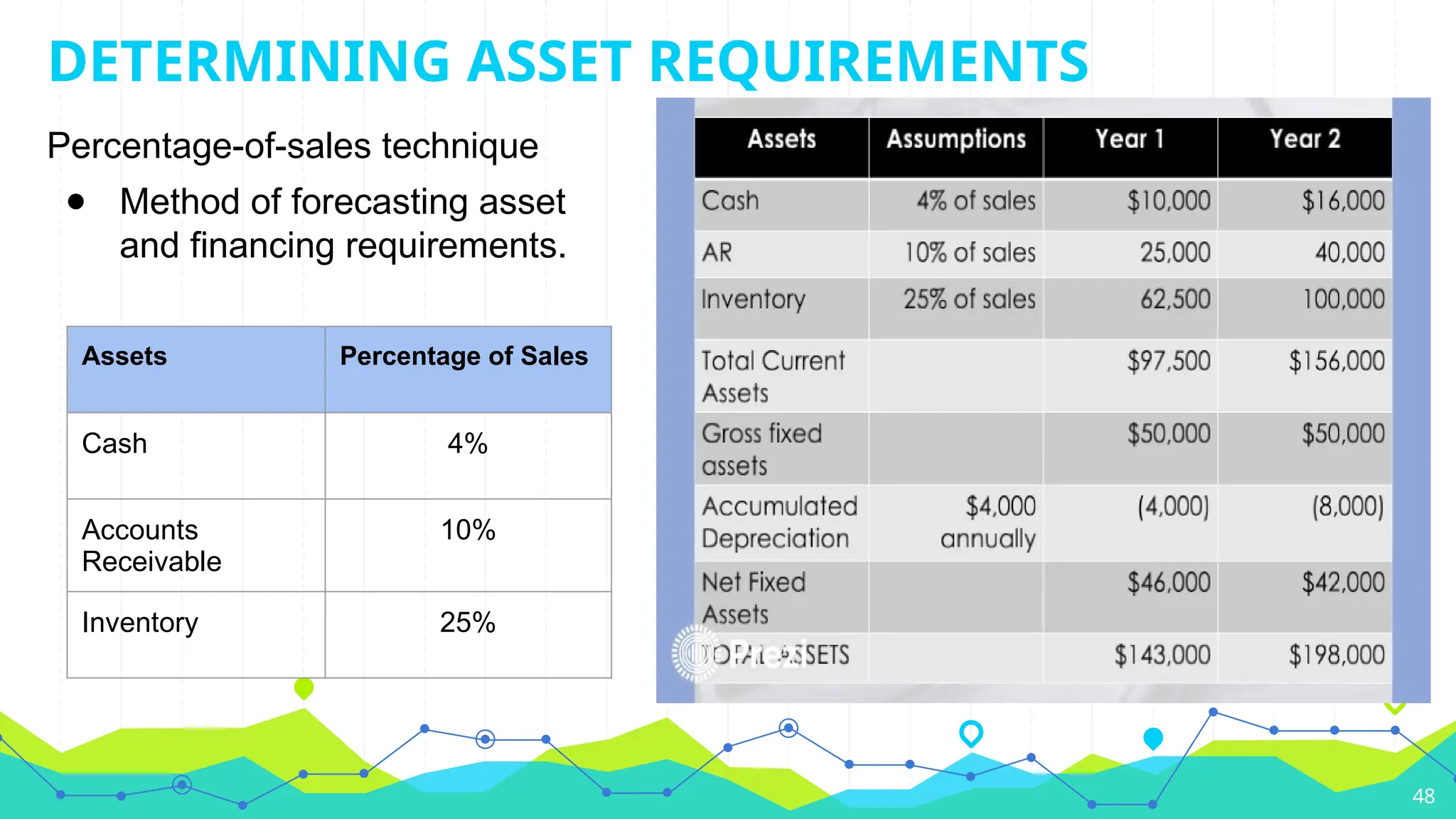

● Working Capital

-cash,accounts receivable, and inventory

required in day to day operations.

● Net working capital

- current assets -current liabilities.

47

FORECASTING ASSET AND FINANCING

REQUIREMENTS

49

● The moreassets a firm's needs the greater the firms financial

requirements

● A firm should finance its growth in a such a way as to maintain

adequate liquidity.

● The amount of total debt that can be used in financing a

business is limited by the funds provided by the owners

● Some types of short-term debt maintain a relatively constant

relationship with sales

● Equity ownership in a business

DETERMINING FINANCING REQUIREMENTS

50.

● Profits andcash flows are not

the same thing

Can be accomplished in one of 2

ways

1. Information from the pro forma

income statement and balance

sheets to develop a pro forma

cash flows

2. Prepare a cash budget

Pro Forma Statement of Cash

Flows

● Change from working with

historical numbers to

projections of numbers.

50

FORECASTING CASH

FLOWS

51.

51

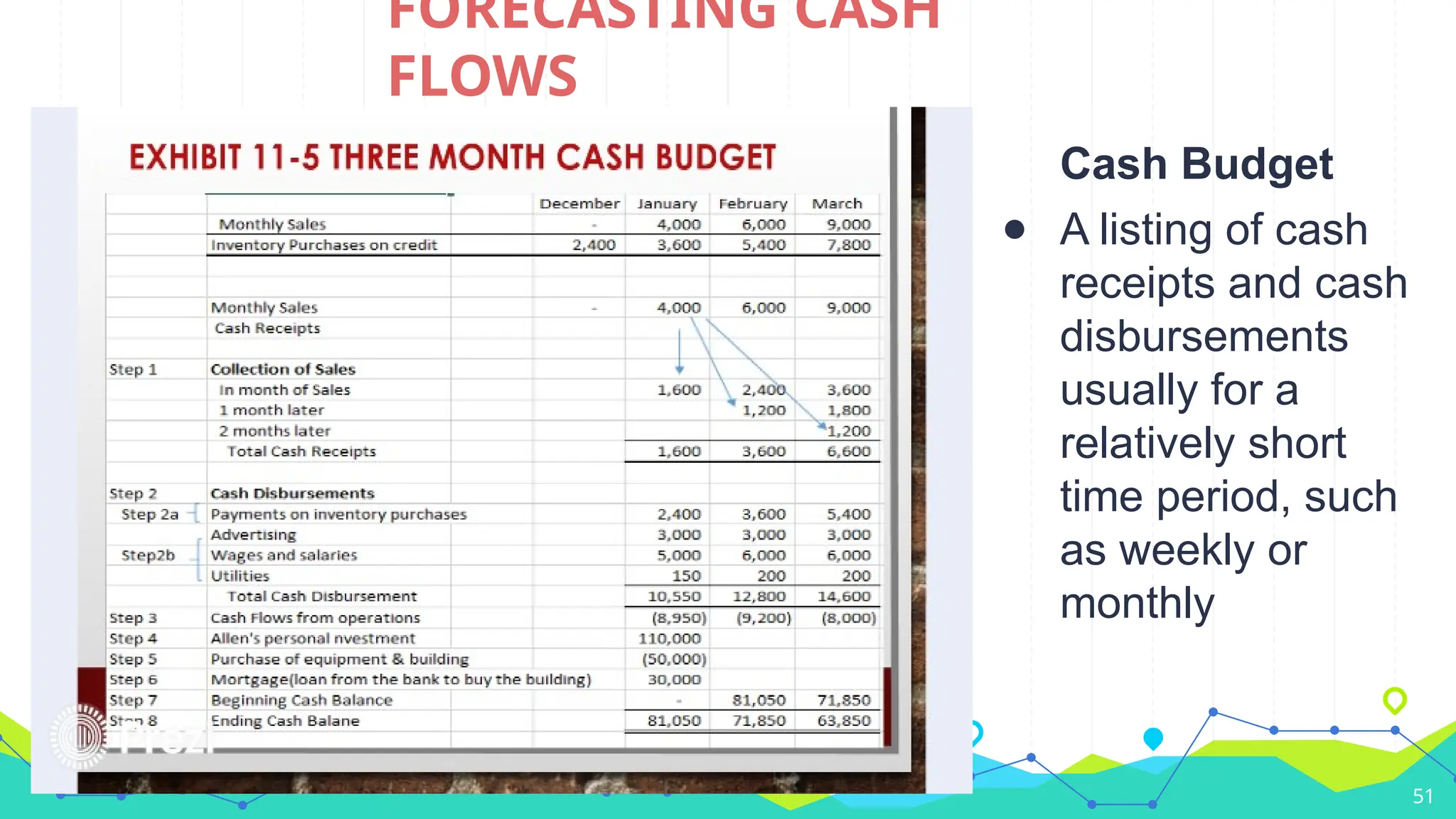

Cash Budget

● Alisting of cash

receipts and cash

disbursements

usually for a

relatively short

time period, such

as weekly or

monthly

FORECASTING CASH

FLOWS

52.

Financial Forecast Suggestion

●Develop realistic sales projections

● Build projections from clear assumptions about marketing and pricing

plans

● Do not use unrealistic profit margins

● Don't limit your projections to an income statement

● Provide monthly data for upcoming year and annual data for

succeeding years

● Avoid providing too much financial information

● Be certain that the numbers reconcile and not by simply plugging in a

figure

● Follow the plan

52

USE JUDGEMENT WHEN FORECASTING

- Provide some suggestions for effective financial forecasting

Editor's Notes

#3 It is the process of analyzing what happened in the past, what is happening now, and using that information to determine what is going to happen in the future. Businesses use financial forecasting as a tool for planning and adapting to uncertainty by more effectively predicting risks, opportunities and challenges that the business could encounter.

#4 1. An example of this is having fire insurance for your property. This covers damage and losses caused by fire and lightning to protect you against financial loss from property damages.

2. For example, a company might forecast an increase in demand for its products during the holiday season. As a result, it may decide to increase production before Christmas so that there aren't any shortages.

3. Contingency planning is the preparation to respond effectively to a significant future incident, event or situation. Also known colloquially as “Plan B”, this is a plan devised for dealing with an emergency, or with something that might possibly happen and cause problems in the future.

#6 The level of detail required for the forecast (what product or product group), units of analysis (pieces, boxes) and time horizon (such as monthly, quarterly, etc.)

Identify needed data and if it is available

Cost, ease of use & accuracy

#8 Qualitative methods: Judgmental methods

Forecasts generated subjectively by the forecaster

Educated guesses

Quantitative methods:

- Forecasts generated through mathematical modeling

#9 [READ NOTES ONLY]

To compare the two general categories of forecasting;

For characteristics,

Qualitative is based on human judgement, opinion; subjective and nonmathematical

While Quantitative is based on mathematics.

For their strengths,

Qualitative can incorporate latest changes in the environment and “inside” information

While Quantitative is consistent and objective; and is able to consider much information and data at one time

For weaknesses,

Qualitative can bias the forecast and reduce forecast accuracy

While for Quantitative, Oftentimes, quantifiable data are not available.

#10 [READ NOTES ONLY]

For the Kinds of Forecasting,

For Qualitative Methods, there are 3 kinds:

The jury of executive opinion is a method of forecasting using a composite forecast from the combined opinions of individual experts.

Market research evaluates the success of a company's services or products by introducing them to potential customers and recording details about how they react.

The Delphi method involves questioning a panel of experts individually to collect their opinions. Interviewing or gathering information from the experts one at a time rather than in a group can help to prevent bias and ensure that any consensus about business predictions stems from the expert opinions on their own.

While for Quantitative Methods, there are 2 kinds:

If data uses time, use time series models. Time series analysis assumes that the future will follow the same patterns as in the past, but not in all cases.

If data uses cause-and-effect relationships, use causal models. This uses leading indicators to predict the future.

![MBA_653_PPT [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/mba653pptautosaved-230605133633-db3c46cc-thumbnail.jpg?width=640&height=640&fit=bounds)