Downloaded 74 times

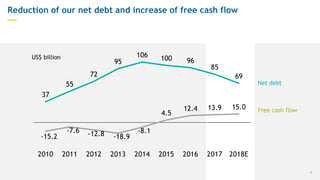

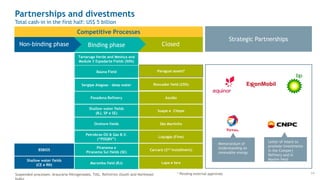

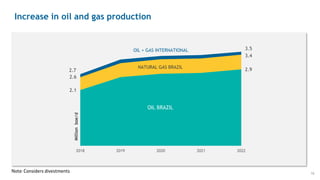

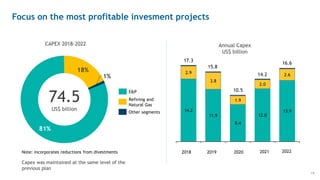

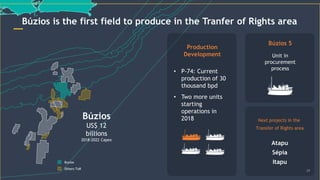

Petrobras provides an overview and highlights of its operations in the first half of 2018. Key points include a net income of $17 billion, an 18% increase in operating income, and starting production from the first system in the Transfer of Rights area of the Buzios field. Petrobras also anticipates increasing production through 2022 by starting up 19 new production units and expanding its exploratory portfolio by 31% since 2017. The company aims to reduce debt levels through divestments and maintain its 2018-2022 capex at $74.5 billion, focusing investments on pre-salt areas and projects with higher profitability.