Downloaded 321 times

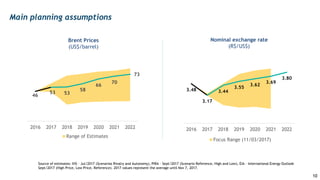

The document contains forward-looking statements regarding the company's performance and economic conditions, highlighting potential risks and uncertainties that could affect actual results. It outlines strategic initiatives aimed at improving financial management, optimizing operations, and transitioning towards a low-carbon economy through investments and divestments. Additionally, it describes specific projects and metrics related to oil and gas production and financial targets through 2022.