Downloaded 47 times

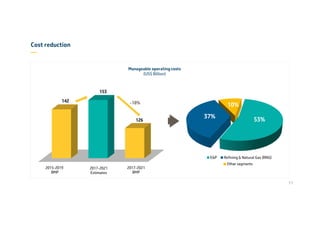

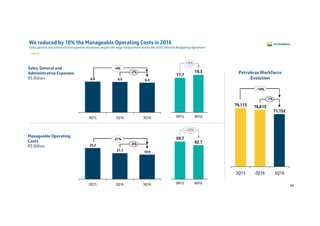

The document outlines Petrobras's strategic plan for 2017-2021, highlighting its focus on generating economic value while managing risks related to oil prices, government approvals, and operational costs. Key initiatives include cost management, increased production from pre-salt areas, and a comprehensive partnerships program aimed at bolstering investment capabilities. Financial estimates for the period suggest a strong emphasis on reducing leverage and improving safety metrics, along with a commitment to ethical governance and operational transparency.