Downloaded 80 times

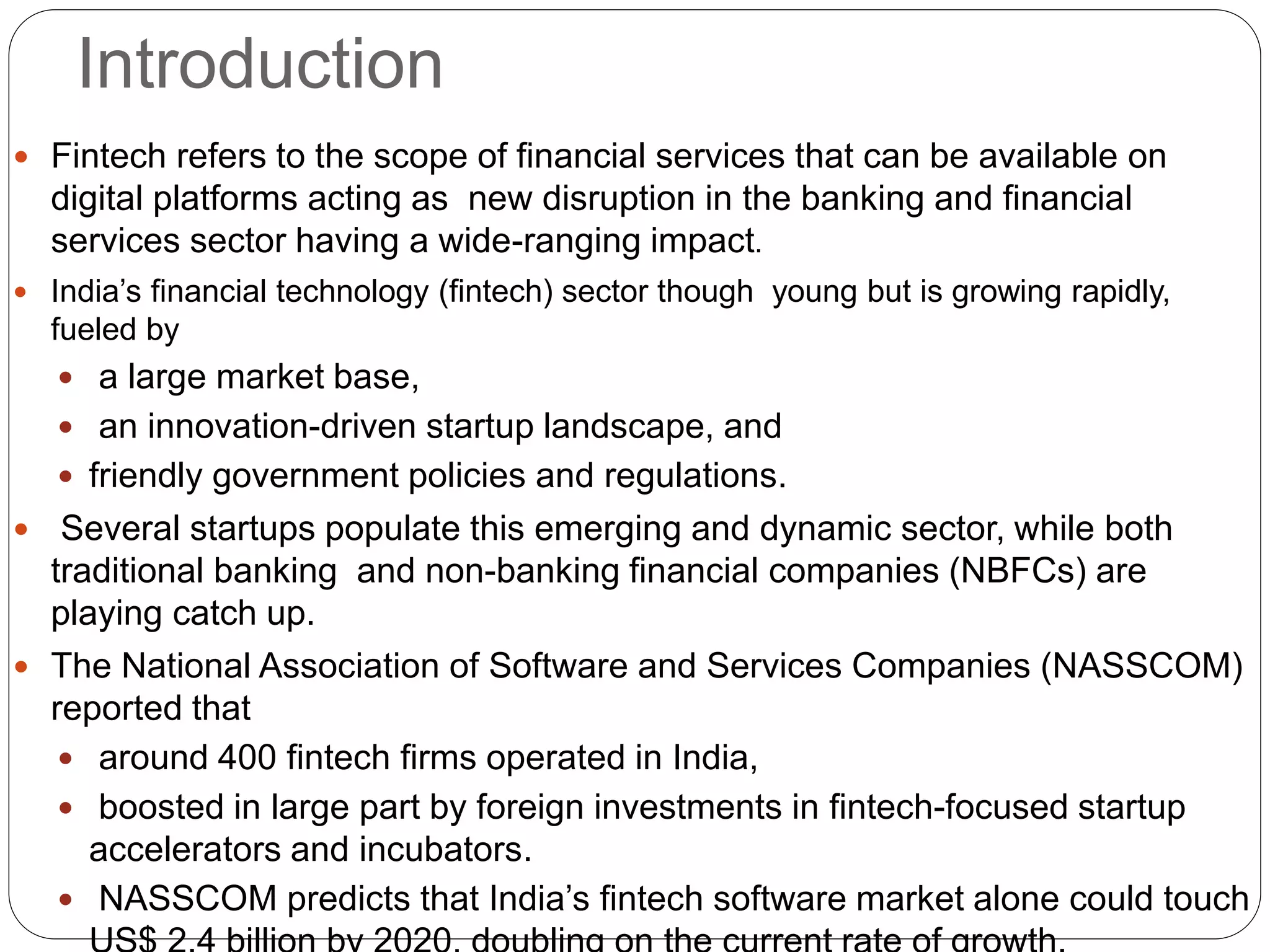

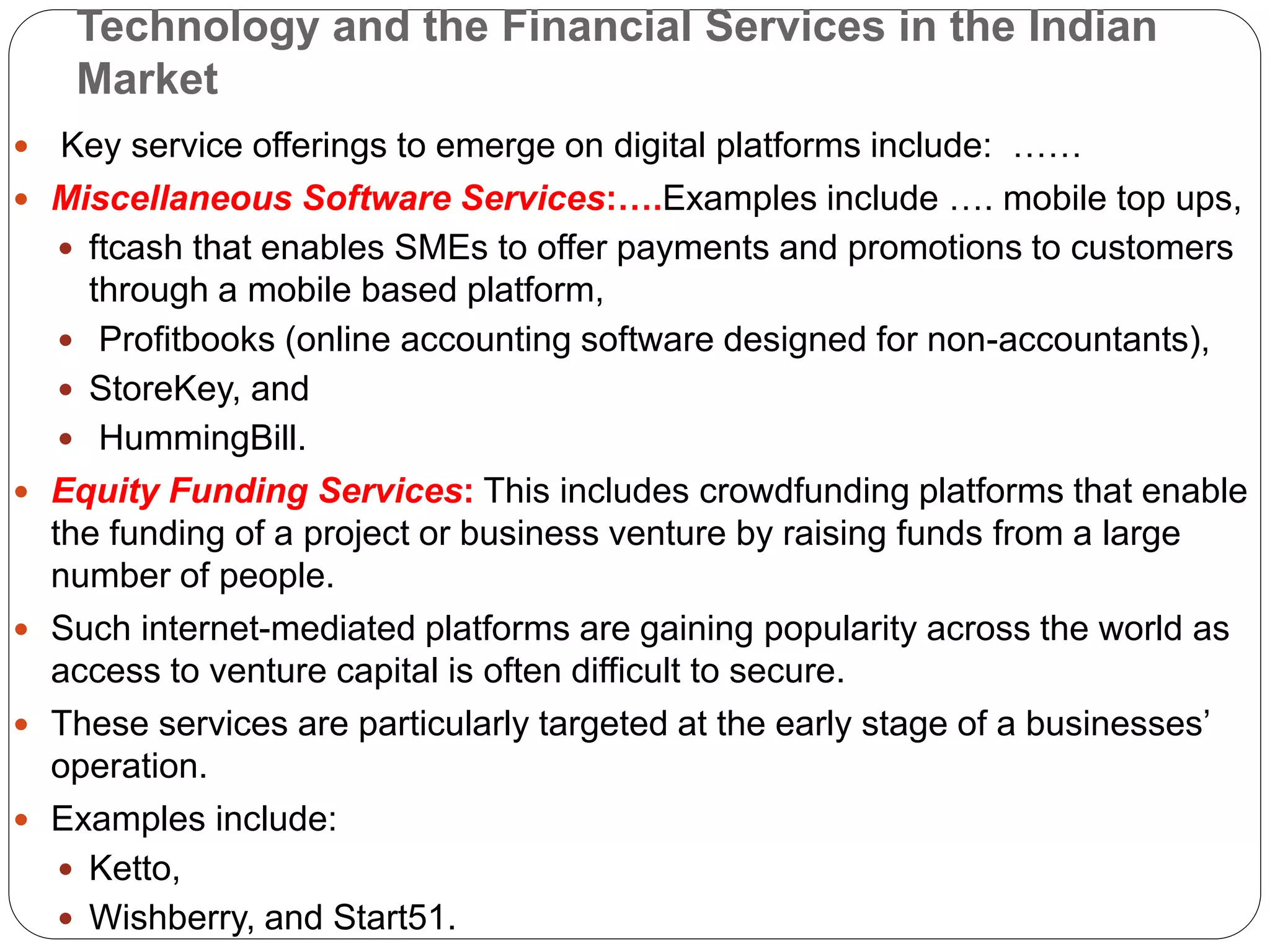

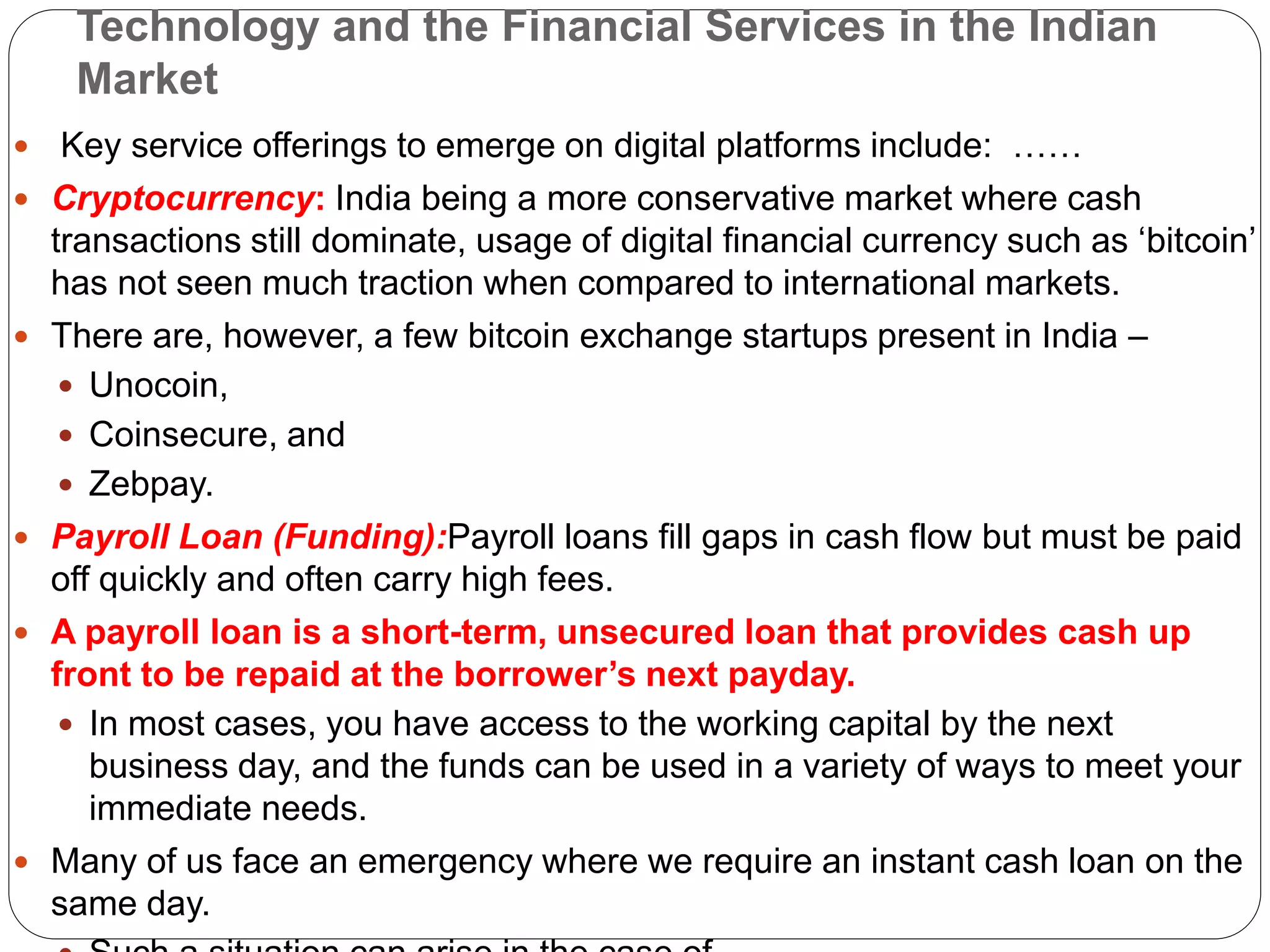

India's fintech sector is growing rapidly, fueled by a large market base, innovation, and supportive government policies. Several startups offer fintech services like peer-to-peer lending, payments, remittances, and personal finance management. Both traditional banks and new fintech companies are disrupting the financial sector by using technology to improve access and efficiency of financial services. While fintech startups face challenges in scaling up, the large untapped market and supportive regulations provide opportunities for expansion. Collaboration between fintech and traditional banks also has potential to foster innovation and inclusion.