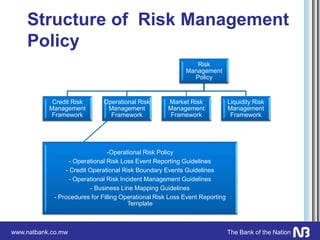

The document outlines the National Bank of Malawi's operational risk management framework. It discusses the operational risk policy, roles and responsibilities of the board, management, and risk division. It describes the bank's approach to identifying, assessing, monitoring, and controlling operational risk. The bank has adopted the Basic Indicator Approach to measure operational risk capital charge and has developed business continuity plans to prepare for disasters. The presentation also discusses operational risk incident management guidelines and roles in reporting and addressing incidents.