Downloaded 237 times

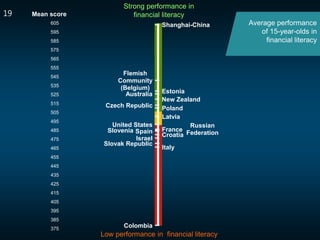

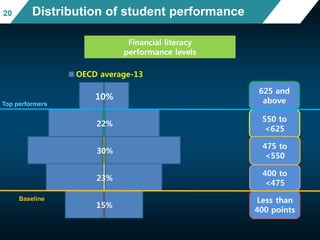

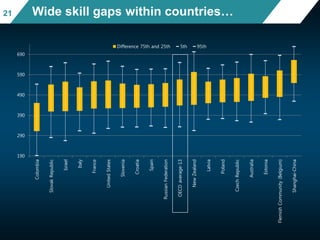

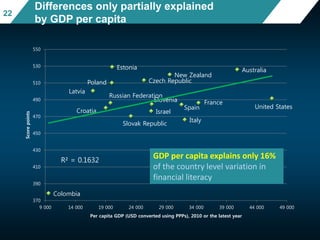

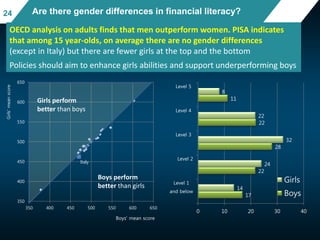

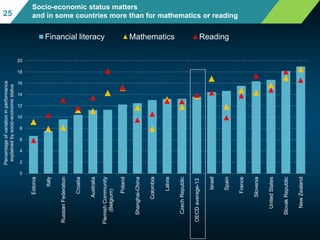

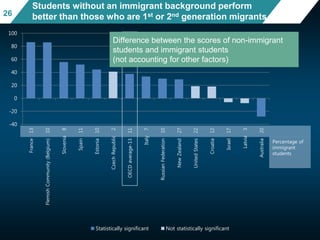

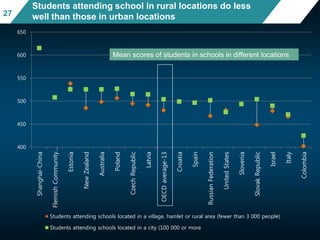

1) The document summarizes key findings from the PISA 2012 assessment of financial literacy among 15-year-old students in 18 countries. 2) On average, students performed between levels 2 and 3 on the PISA financial literacy scale, indicating they can interpret basic financial documents but have difficulty with more complex tasks. 3) Performance varied widely between and within countries and was strongly linked to socioeconomic status. Girls, immigrant students, and those from rural areas tended to perform worse.