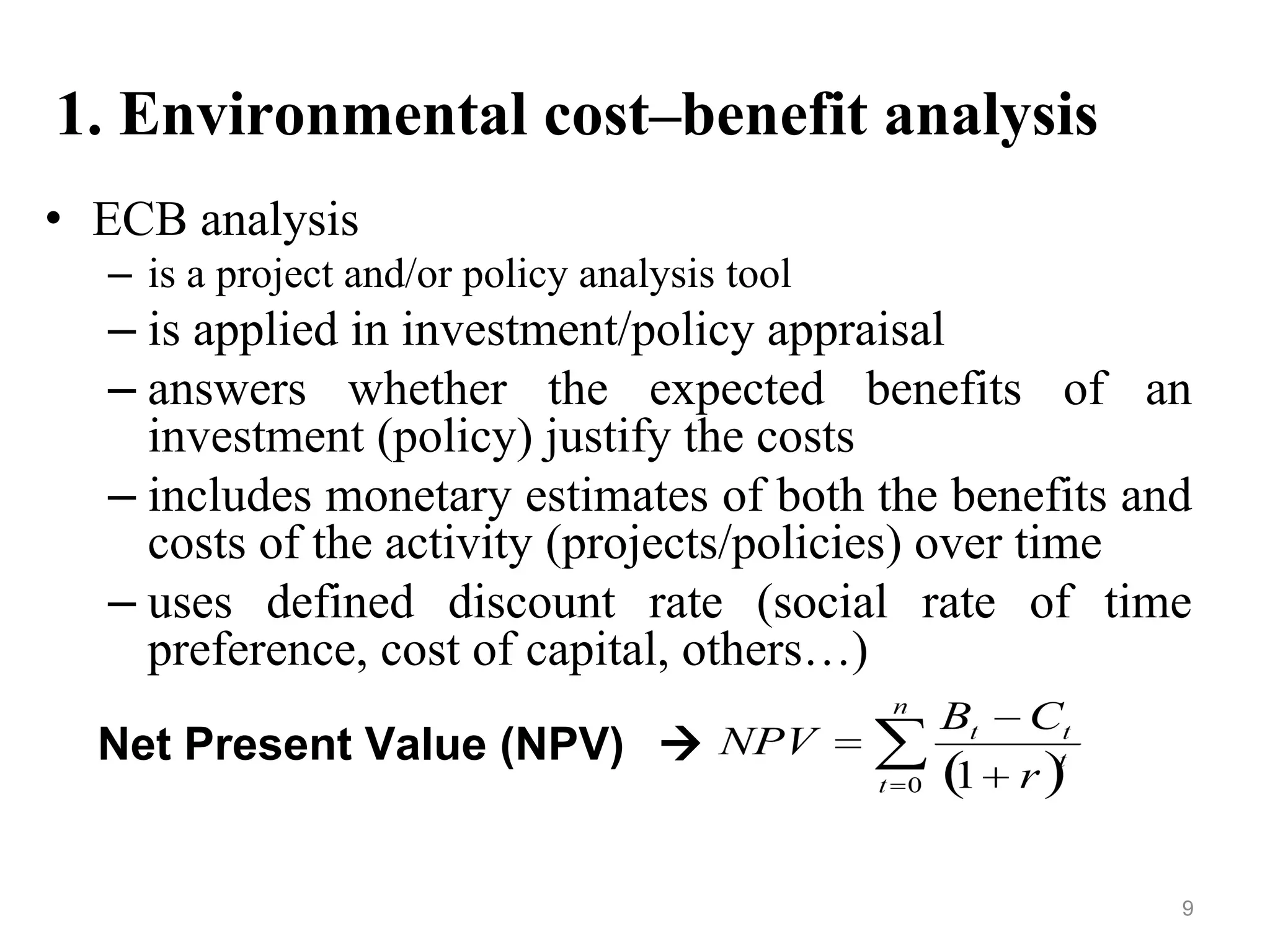

This document provides an overview of chapter six from a course on natural resource and environmental economics. It discusses the need to value environmental resources and classify their economic benefits. Techniques for measuring the economic value of non-market environmental goods include stated preference methods like contingent valuation and revealed preference methods like the travel cost approach. Environmental cost-benefit analysis balances monetary estimates of the benefits and costs of projects or policies over time. Valuing the environment helps incorporate important externalities, identify market failures, and propose solutions.