Downloaded 40 times

![1

REGULATION (EU) [2018/XX*] OF THE

EUROPEAN CENTRAL BANK

of [date Month 2018]

exercising a discretion under Article

178(2)(d) of Regulation (EU) No 575/2013

in relation to the threshold for assessing

the materiality of credit obligations past

due

delegated regulation

Guidelines on the application of the

definition of default under Article 178 of

Regulation (EU) No

575/2013(EBA/GL/2016/07)

guidelines

COMMISSION DELEGATED

REGULATION (EU) 2018/171 of 19

October 2017 on supplementing

Regulation (EU) No 575/2013 of the

European Parliament and of the Council

with regard to regulatory technical

standards for the materiality threshold for

credit obligations past due

RTS

Sources](https://image.slidesharecdn.com/dod-180713203018/85/New-Definition-of-Default-2-320.jpg)

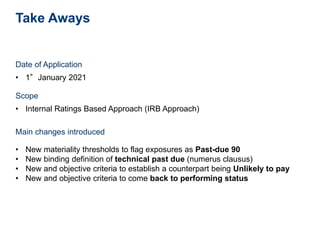

The document outlines a new definition of default sources and the main changes introduced, effective January 1, 2021, regarding credit obligations past due. It establishes new materiality thresholds for classifying exposures as past-due and provides objective criteria for determining when a party is unlikely to pay. Additionally, it details conditions under which a defaulted obligor can return to performing status and introduces specific calculations for loss and diminished financial obligations.