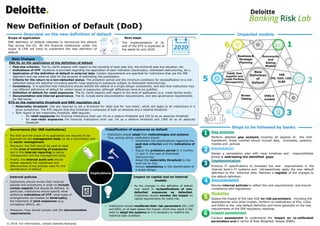

EBA definition of Default intended to harmonize the default flag across the EU. All the financial institutions under the scope of CRR will have to implement the new definition of default.

a short deck summarising the main aspects involved with the alignment to the EBA guidelines on the default definition application. Details are provided on:

the past due threshold,

the technical past due cases

the unlikely to pay indicators

the criteria for coming back to performing status

Cost of Capital- features of capital-meaning of cost of capital-factors affecting cost of capital-Computation of cost of capital-cost of equity capital-cost of preference capital-cost of debenture-weighted average cost of capital

Capital structure- Factors affecting capital structure- Problems on EPS- Capital structure theories

Bancassurance comprises of two words: bank and insurance. It is an agreement between bank and insurance companies where banks operate as intermediary between insurance company and its customers and sell insurance through their existing distribution network.

https://efinancemanagement.com/financial-management/bancassurance

a short deck summarising the main aspects involved with the alignment to the EBA guidelines on the default definition application. Details are provided on:

the past due threshold,

the technical past due cases

the unlikely to pay indicators

the criteria for coming back to performing status

Cost of Capital- features of capital-meaning of cost of capital-factors affecting cost of capital-Computation of cost of capital-cost of equity capital-cost of preference capital-cost of debenture-weighted average cost of capital

Capital structure- Factors affecting capital structure- Problems on EPS- Capital structure theories

Bancassurance comprises of two words: bank and insurance. It is an agreement between bank and insurance companies where banks operate as intermediary between insurance company and its customers and sell insurance through their existing distribution network.

https://efinancemanagement.com/financial-management/bancassurance

Given the recent financial crisis and the extended impact on global credit market and liquidity, it is imperative that financial institutions strengthen their market risk management capabilities to effectively meet compelling business objectives and challenges which include portfolio pricing and portfolio exposure management

This presentation is prepared by Toran Lal Verma. The presentation deals with the calculation of cost of debt, equity, preference share and retained earnings.

Binary Logistic Regression Classification makes use of one or more predictor variables that may be either continuous or categorical to predict target variable classes. This technique identifies important factors impacting the target variable and also the nature of the relationship between each of these factors and the dependent variable. It is useful in the analysis of multiple factors influencing an outcome, or other classification where there two possible outcomes.

Credit insurance is becoming increasingly important. Having the right payment terms with your customers is critical to your competitiveness and being able to grow your organisation with confidence. Ensuring that those terms of business are adhered to is not always in your control.

Without protection that your invoices will be paid, your business decisions are based on faith and past experience alone, which may not be the best grounds for ensuring business profitability.

According to the recent Atradius survey results for B2B payment practices, over 40% of invoices remain unpaid past due date.

This is where credit insurance and robust credit management policies can help. Credit insurance is as much about protection against bad debt as a facilitator for growth and maximising your profitability.

This short guide aims to help you understand how credit insurance can support your business, assess whether you really need it and give insight into why it is of growing importance.

The European Banking Authority (EBA) launched a consultation on its draft Regulatory Technical Standards on assessment methodology for internal ratings-based approach. These draft RTS are a key component of the EBA's work to ensure consistency in models outputs and comparability of risk-weighted exposures and will contribute to harmonize the supervisory assessment methodology across all EU Member States. The consultation runs until 12 March 2015.

Given the recent financial crisis and the extended impact on global credit market and liquidity, it is imperative that financial institutions strengthen their market risk management capabilities to effectively meet compelling business objectives and challenges which include portfolio pricing and portfolio exposure management

This presentation is prepared by Toran Lal Verma. The presentation deals with the calculation of cost of debt, equity, preference share and retained earnings.

Binary Logistic Regression Classification makes use of one or more predictor variables that may be either continuous or categorical to predict target variable classes. This technique identifies important factors impacting the target variable and also the nature of the relationship between each of these factors and the dependent variable. It is useful in the analysis of multiple factors influencing an outcome, or other classification where there two possible outcomes.

Credit insurance is becoming increasingly important. Having the right payment terms with your customers is critical to your competitiveness and being able to grow your organisation with confidence. Ensuring that those terms of business are adhered to is not always in your control.

Without protection that your invoices will be paid, your business decisions are based on faith and past experience alone, which may not be the best grounds for ensuring business profitability.

According to the recent Atradius survey results for B2B payment practices, over 40% of invoices remain unpaid past due date.

This is where credit insurance and robust credit management policies can help. Credit insurance is as much about protection against bad debt as a facilitator for growth and maximising your profitability.

This short guide aims to help you understand how credit insurance can support your business, assess whether you really need it and give insight into why it is of growing importance.

The European Banking Authority (EBA) launched a consultation on its draft Regulatory Technical Standards on assessment methodology for internal ratings-based approach. These draft RTS are a key component of the EBA's work to ensure consistency in models outputs and comparability of risk-weighted exposures and will contribute to harmonize the supervisory assessment methodology across all EU Member States. The consultation runs until 12 March 2015.

IFRS Implementation and How the Banks should approach itJAMES OKARIMIA

IFRS Implementation and how the banks should approach it.

Though the final version of IFRS came up in 2014, the banks across the globe have recently embarked the journey. Any new regulation requires significant effort to revisit its existing governance, policies & processes, data and the systems and IFRS 9 is no different.

IFRS Implementation and How the Banks should Approach It.JAMES OKARIMIA

IFRS Implementation and How the Banks should Approach It. A publication by James Okarimia

Managing Partner at RM associates

Partners in Enterprise Risk Managements

Resume

• Real GDP growth slowed down due to problems with access to electricity caused by the destruction of manoeuvrable electricity generation by Russian drones and missiles.

• Exports and imports continued growing due to better logistics through the Ukrainian sea corridor and road. Polish farmers and drivers stopped blocking borders at the end of April.

• In April, both the Tax and Customs Services over-executed the revenue plan. Moreover, the NBU transferred twice the planned profit to the budget.

• The European side approved the Ukraine Plan, which the government adopted to determine indicators for the Ukraine Facility. That approval will allow Ukraine to receive a EUR 1.9 bn loan from the EU in May. At the same time, the EU provided Ukraine with a EUR 1.5 bn loan in April, as the government fulfilled five indicators under the Ukraine Plan.

• The USA has finally approved an aid package for Ukraine, which includes USD 7.8 bn of budget support; however, the conditions and timing of the assistance are still unknown.

• As in March, annual consumer inflation amounted to 3.2% yoy in April.

• At the April monetary policy meeting, the NBU again reduced the key policy rate from 14.5% to 13.5% per annum.

• Over the past four weeks, the hryvnia exchange rate has stabilized in the UAH 39-40 per USD range.

NO1 Uk Rohani Baba In Karachi Bangali Baba Karachi Online Amil Baba WorldWide...Amil baba

Contact with Dawood Bhai Just call on +92322-6382012 and we'll help you. We'll solve all your problems within 12 to 24 hours and with 101% guarantee and with astrology systematic. If you want to take any personal or professional advice then also you can call us on +92322-6382012 , ONLINE LOVE PROBLEM & Other all types of Daily Life Problem's.Then CALL or WHATSAPP us on +92322-6382012 and Get all these problems solutions here by Amil Baba DAWOOD BANGALI

#vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore#blackmagicformarriage #aamilbaba #kalajadu #kalailam #taweez #wazifaexpert #jadumantar #vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore #blackmagicforlove #blackmagicformarriage #aamilbaba #kalajadu #kalailam #taweez #wazifaexpert #jadumantar #vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore #Amilbabainuk #amilbabainspain #amilbabaindubai #Amilbabainnorway #amilbabainkrachi #amilbabainlahore #amilbabaingujranwalan #amilbabainislamabad

Falcon stands out as a top-tier P2P Invoice Discounting platform in India, bridging esteemed blue-chip companies and eager investors. Our goal is to transform the investment landscape in India by establishing a comprehensive destination for borrowers and investors with diverse profiles and needs, all while minimizing risk. What sets Falcon apart is the elimination of intermediaries such as commercial banks and depository institutions, allowing investors to enjoy higher yields.

If you are looking for a pi coin investor. Then look no further because I have the right one he is a pi vendor (he buy and resell to whales in China). I met him on a crypto conference and ever since I and my friends have sold more than 10k pi coins to him And he bought all and still want more. I will drop his telegram handle below just send him a message.

@Pi_vendor_247

Empowering the Unbanked: The Vital Role of NBFCs in Promoting Financial Inclu...Vighnesh Shashtri

In India, financial inclusion remains a critical challenge, with a significant portion of the population still unbanked. Non-Banking Financial Companies (NBFCs) have emerged as key players in bridging this gap by providing financial services to those often overlooked by traditional banking institutions. This article delves into how NBFCs are fostering financial inclusion and empowering the unbanked.

What price will pi network be listed on exchangesDOT TECH

The rate at which pi will be listed is practically unknown. But due to speculations surrounding it the predicted rate is tends to be from 30$ — 50$.

So if you are interested in selling your pi network coins at a high rate tho. Or you can't wait till the mainnet launch in 2026. You can easily trade your pi coins with a merchant.

A merchant is someone who buys pi coins from miners and resell them to Investors looking forward to hold massive quantities till mainnet launch.

I will leave the telegram contact of my personal pi vendor to trade with.

@Pi_vendor_247

how to sell pi coins on Bitmart crypto exchangeDOT TECH

Yes. Pi network coins can be exchanged but not on bitmart exchange. Because pi network is still in the enclosed mainnet. The only way pioneers are able to trade pi coins is by reselling the pi coins to pi verified merchants.

A verified merchant is someone who buys pi network coins and resell it to exchanges looking forward to hold till mainnet launch.

I will leave the telegram contact of my personal pi merchant to trade with.

@Pi_vendor_247

US Economic Outlook - Being Decided - M Capital Group August 2021.pdfpchutichetpong

The U.S. economy is continuing its impressive recovery from the COVID-19 pandemic and not slowing down despite re-occurring bumps. The U.S. savings rate reached its highest ever recorded level at 34% in April 2020 and Americans seem ready to spend. The sectors that had been hurt the most by the pandemic specifically reduced consumer spending, like retail, leisure, hospitality, and travel, are now experiencing massive growth in revenue and job openings.

Could this growth lead to a “Roaring Twenties”? As quickly as the U.S. economy contracted, experiencing a 9.1% drop in economic output relative to the business cycle in Q2 2020, the largest in recorded history, it has rebounded beyond expectations. This surprising growth seems to be fueled by the U.S. government’s aggressive fiscal and monetary policies, and an increase in consumer spending as mobility restrictions are lifted. Unemployment rates between June 2020 and June 2021 decreased by 5.2%, while the demand for labor is increasing, coupled with increasing wages to incentivize Americans to rejoin the labor force. Schools and businesses are expected to fully reopen soon. In parallel, vaccination rates across the country and the world continue to rise, with full vaccination rates of 50% and 14.8% respectively.

However, it is not completely smooth sailing from here. According to M Capital Group, the main risks that threaten the continued growth of the U.S. economy are inflation, unsettled trade relations, and another wave of Covid-19 mutations that could shut down the world again. Have we learned from the past year of COVID-19 and adapted our economy accordingly?

“In order for the U.S. economy to continue growing, whether there is another wave or not, the U.S. needs to focus on diversifying supply chains, supporting business investment, and maintaining consumer spending,” says Grace Feeley, a research analyst at M Capital Group.

While the economic indicators are positive, the risks are coming closer to manifesting and threatening such growth. The new variants spreading throughout the world, Delta, Lambda, and Gamma, are vaccine-resistant and muddy the predictions made about the economy and health of the country. These variants bring back the feeling of uncertainty that has wreaked havoc not only on the stock market but the mindset of people around the world. MCG provides unique insight on how to mitigate these risks to possibly ensure a bright economic future.

when will pi network coin be available on crypto exchange.DOT TECH

There is no set date for when Pi coins will enter the market.

However, the developers are working hard to get them released as soon as possible.

Once they are available, users will be able to exchange other cryptocurrencies for Pi coins on designated exchanges.

But for now the only way to sell your pi coins is through verified pi vendor.

Here is the telegram contact of my personal pi vendor

@Pi_vendor_247

how to swap pi coins to foreign currency withdrawable.DOT TECH

As of my last update, Pi is still in the testing phase and is not tradable on any exchanges.

However, Pi Network has announced plans to launch its Testnet and Mainnet in the future, which may include listing Pi on exchanges.

The current method for selling pi coins involves exchanging them with a pi vendor who purchases pi coins for investment reasons.

If you want to sell your pi coins, reach out to a pi vendor and sell them to anyone looking to sell pi coins from any country around the globe.

Below is the contact information for my personal pi vendor.

Telegram: @Pi_vendor_247

how can i use my minded pi coins I need some funds.DOT TECH

If you are interested in selling your pi coins, i have a verified pi merchant, who buys pi coins and resell them to exchanges looking forward to hold till mainnet launch.

Because the core team has announced that pi network will not be doing any pre-sale. The only way exchanges like huobi, bitmart and hotbit can get pi is by buying from miners.

Now a merchant stands in between these exchanges and the miners. As a link to make transactions smooth. Because right now in the enclosed mainnet you can't sell pi coins your self. You need the help of a merchant,

i will leave the telegram contact of my personal pi merchant below. 👇 I and my friends has traded more than 3000pi coins with him successfully.

@Pi_vendor_247

The European Unemployment Puzzle: implications from population agingGRAPE

We study the link between the evolving age structure of the working population and unemployment. We build a large new Keynesian OLG model with a realistic age structure, labor market frictions, sticky prices, and aggregate shocks. Once calibrated to the European economy, we quantify the extent to which demographic changes over the last three decades have contributed to the decline of the unemployment rate. Our findings yield important implications for the future evolution of unemployment given the anticipated further aging of the working population in Europe. We also quantify the implications for optimal monetary policy: lowering inflation volatility becomes less costly in terms of GDP and unemployment volatility, which hints that optimal monetary policy may be more hawkish in an aging society. Finally, our results also propose a partial reversal of the European-US unemployment puzzle due to the fact that the share of young workers is expected to remain robust in the US.

how to sell pi coins in all Africa Countries.DOT TECH

Yes. You can sell your pi network for other cryptocurrencies like Bitcoin, usdt , Ethereum and other currencies And this is done easily with the help from a pi merchant.

What is a pi merchant ?

Since pi is not launched yet in any exchange. The only way you can sell right now is through merchants.

A verified Pi merchant is someone who buys pi network coins from miners and resell them to investors looking forward to hold massive quantities of pi coins before mainnet launch in 2026.

I will leave the telegram contact of my personal pi merchant to trade with.

@Pi_vendor_247

how can I sell my pi coins for cash in a pi APPDOT TECH

You can't sell your pi coins in the pi network app. because it is not listed yet on any exchange.

The only way you can sell is by trading your pi coins with an investor (a person looking forward to hold massive amounts of pi coins before mainnet launch) .

You don't need to meet the investor directly all the trades are done with a pi vendor/merchant (a person that buys the pi coins from miners and resell it to investors)

I Will leave The telegram contact of my personal pi vendor, if you are finding a legitimate one.

@Pi_vendor_247

#pi network

#pi coins

#money

how to sell pi coins in South Korea profitably.DOT TECH

Yes. You can sell your pi network coins in South Korea or any other country, by finding a verified pi merchant

What is a verified pi merchant?

Since pi network is not launched yet on any exchange, the only way you can sell pi coins is by selling to a verified pi merchant, and this is because pi network is not launched yet on any exchange and no pre-sale or ico offerings Is done on pi.

Since there is no pre-sale, the only way exchanges can get pi is by buying from miners. So a pi merchant facilitates these transactions by acting as a bridge for both transactions.

How can i find a pi vendor/merchant?

Well for those who haven't traded with a pi merchant or who don't already have one. I will leave the telegram id of my personal pi merchant who i trade pi with.

Tele gram: @Pi_vendor_247

#pi #sell #nigeria #pinetwork #picoins #sellpi #Nigerian #tradepi #pinetworkcoins #sellmypi