Downloaded 32 times

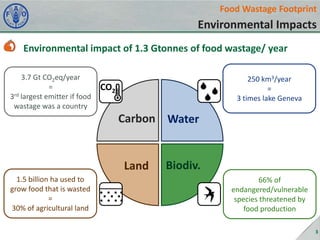

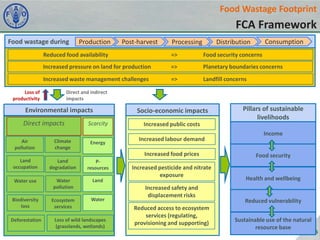

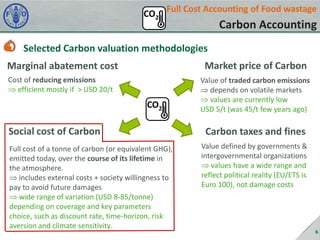

This document summarizes a presentation on full cost accounting of food wastage. It discusses the environmental and economic impacts of the 1.3 gigatons of food wasted annually. Environmentally, it accounts for 3.7 gigatons of greenhouse gas emissions, uses 250 cubic kilometers of water, and occupies 1.5 billion hectares of land. Economically, using producer prices the loss is estimated at $750 billion annually, and using retail prices it is $920 billion. The presentation then outlines frameworks for monetizing some of these environmental costs, such as $55-$900 billion to account for greenhouse gas emissions using social cost of carbon estimates. It acknowledges challenges and limitations but argues full cost accounting can help identify policy priorities

![BC3 Policy Briefings: [2015-02] Modelling ecosystem services trade-offs in ag...](https://cdn.slidesharecdn.com/ss_thumbnails/bc3pb201502en-150513101231-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)