Downloaded 11 times

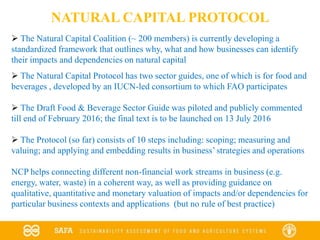

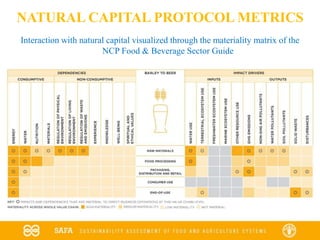

This document discusses methods for assessing sustainability and natural capital accounting. It provides an overview of the Ecosystem-based Business Risk Analysis Tool (EBBRAT) and comments on its approach. It also discusses the Natural Capital Coalition Protocol and its sector guides for assessing impacts on natural capital. Finally, it outlines the Sustainability Assessment of Food and Agriculture (SAFA) framework for evaluating sustainability across environmental, social, economic and governance dimensions.