Downloaded 106 times

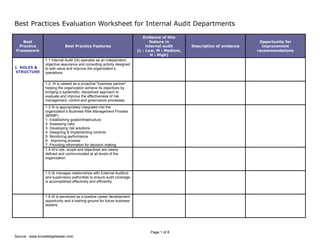

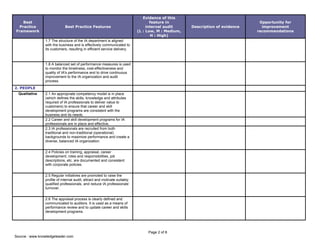

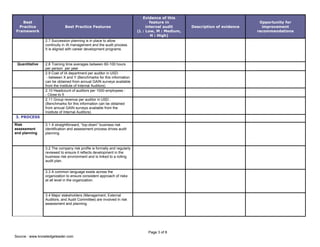

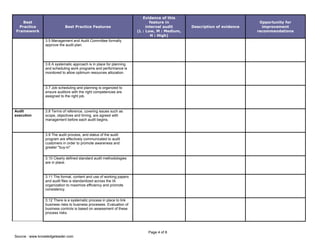

The document outlines best practices for internal audit departments across five key areas: roles and structure, people, process, technology, and knowledge. It provides examples of best practice features for each area and a template for departments to evaluate the evidence of these features in their own practices. The template can be used to assess areas as low, medium, or high and identify opportunities for improvement. The document aims to help internal audit departments evaluate their practices against industry standards and enhance their ability to add value through continuous improvement.