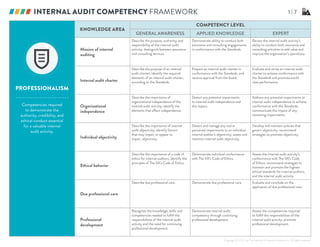

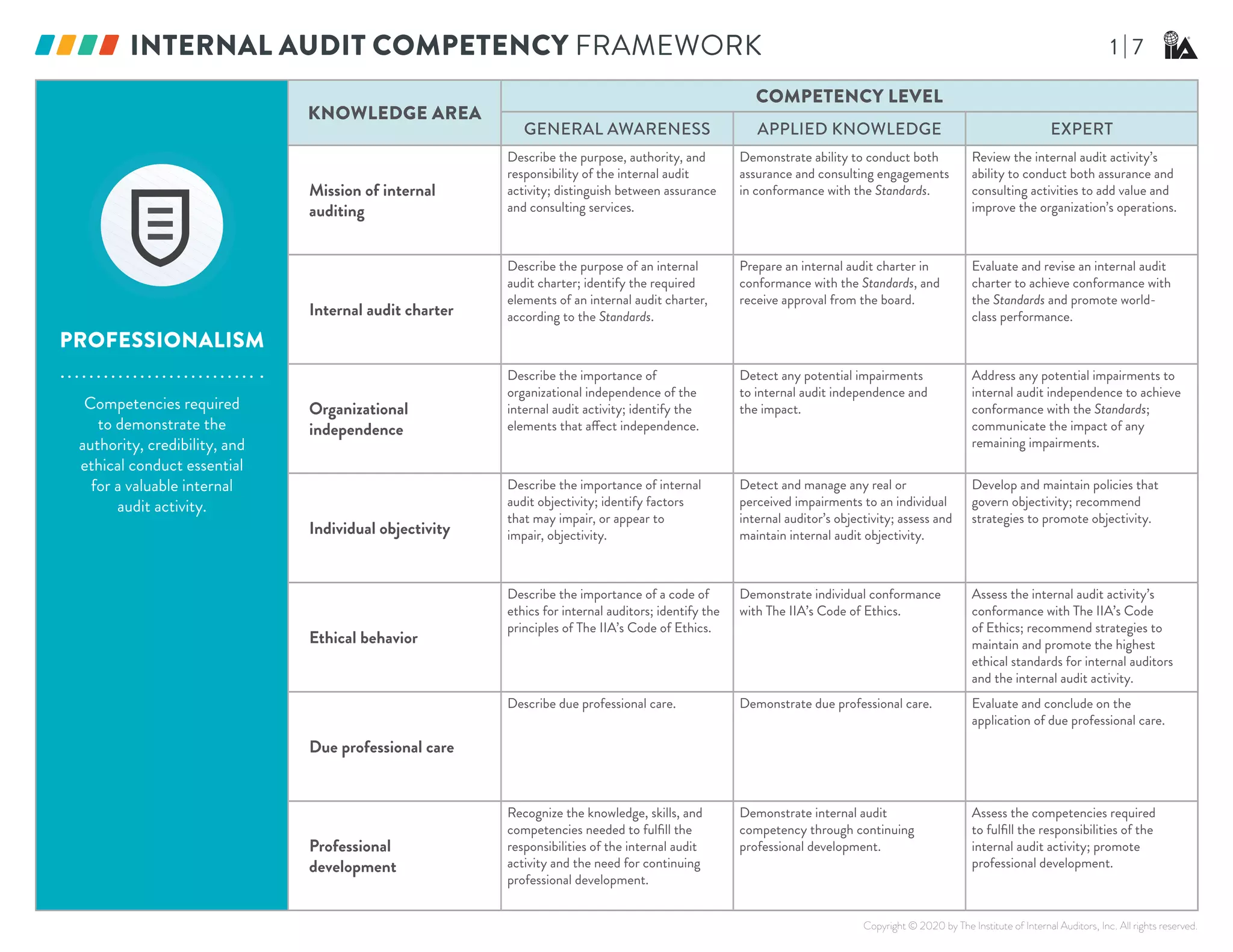

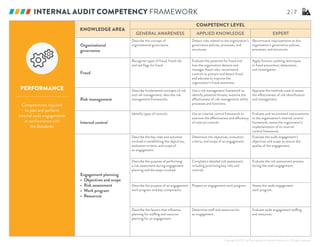

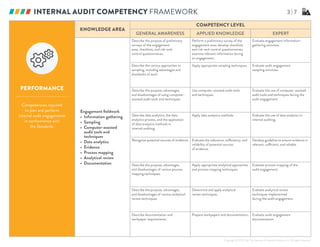

This document outlines a competency framework for internal auditors organized into two main knowledge areas: professionalism and performance. For each knowledge area, competencies are defined at three levels - general awareness, applied knowledge, and expert. For professionalism competencies like mission of internal auditing, independence, ethics, and professional development are described. For performance competencies like governance, risk, controls, engagement planning, fieldwork, and outcomes are outlined. The framework provides definitions of each competency at the increasing levels of expertise to guide internal auditors in developing skills.