Downloaded 18 times

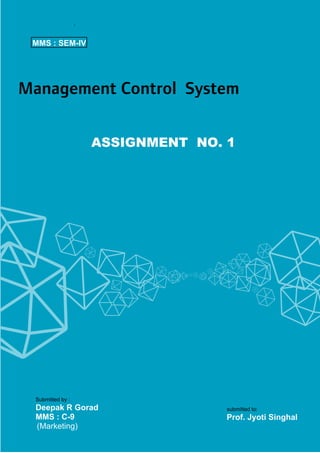

![Q.1 How is RI (EVA) analysis carried out? Explain advantages and disadvantages.

Ans. The EVA method is based on the past performance of the corporate enterprise. The

underlying economic principle in this method is to determine whether the firm is earning a

higher rate of return on the entire invested funds than the cost of such funds (measured in terms

of weighted average cost of capital, WACC). If the answer is positive, the firm‟s management is

adding to the shareholders value by earning extra for them. On the contrary, if the WACC is

higher than the corporate earning rate, the firm‟s operations have eroded the existing wealth of

its equity shareholders. In operational terms, the method attempts to measure economic value

added (or destroyed) for equity shareholders, by the firm‟s operations, in a given year.

Since WACC takes care of the financial costs of all sources of providers of invested

funds in a corporate enterprise, it is imperative that operating profits after taxes (and not net

profits after taxes) should be considered to measure EVA. The accounting profits after taxes, as

reported by the income statement, need adjustments for interest costs. The profit should be the

net operating profit after taxes and the cost of funds will be the product of the total capital

supplied (including retained earnings) and WACC

EVA= [Net operating profits after taxes – [Total Capital * WACC]

Example; Following is the condensed income statement of a firm for the current year;

Particulars

Amt (in lakhs)

Sales Revenue

500

Less: Operating costs

300

Less: Interest costs

12

Earnings before taxes

188

Less: Taxes (0.40)

75.2

Earnings after taxes

112.8

The firm‟s existing capital consists of Rs 150 lakhs Equity funds, having 15% cost and of

Rs 100 lakh 12% debt. Determine the economic value added during the year.

Solution

(I)

Determination of Net Operating Profit After Taxes

Particulars

Amt (in lakhs)

Sales revenue

500

Less: Operating Costs

300

Operating profit (EBIT)

200

Less: Taxes (0.40)

80

Net operating profit after taxes (NOPAT)

120

(II)

Determination of WACC

Particulars

Equity (150 lakh * 15%)

12% Debt (100 lakh * 7.2%)

Total Cost

Amt (in lakhs)

22.5

7.2

29.7](https://image.slidesharecdn.com/mcsassignment-drgorad-140302021235-phpapp01/85/Mcs-DRGORAD-2-320.jpg)

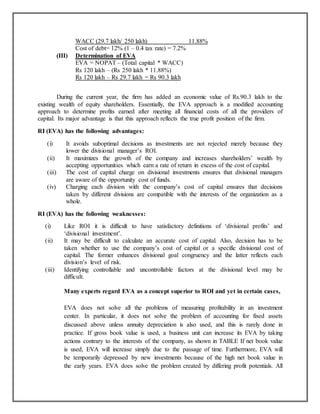

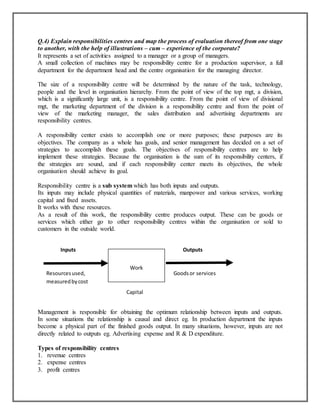

This document contains an assignment response that discusses and provides examples of Economic Value Added (EVA) analysis and different types of expense centers. For EVA analysis, it explains how EVA is calculated by determining net operating profit after taxes and subtracting the cost of capital. It provides an example calculation. The response also outlines advantages and disadvantages of EVA analysis. Regarding expense centers, it distinguishes between engineered and discretionary expense centers. Engineered centers have outputs that can be estimated, while discretionary centers rely more on management judgment. It provides a diagram to illustrate the relationship between inputs and outputs for an engineered center.