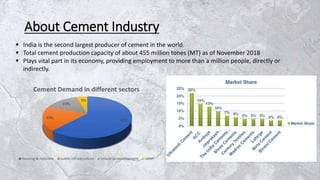

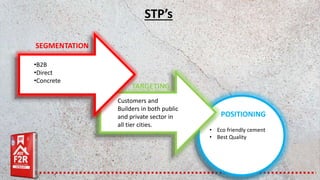

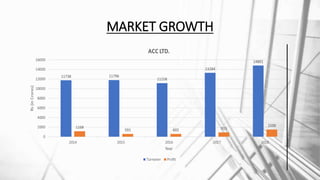

The document outlines a survey conducted by Group 10 on the cement industry in India, focusing on ACC Ltd., a leading cement manufacturer with 15 plants and a substantial market presence. Key findings emphasize the industry's significance, production capacity, and competitive dynamics, alongside the company’s strengths, weaknesses, and opportunities within the market. Recommendations for improvement include adjusting pricing strategies and enhancing promotional efforts to increase brand visibility and customer engagement.