The document provides an overview of the Indian cement industry, including its structure, key players, production levels, demand drivers, major projects, pricing, and costs. Some of the key points summarized are:

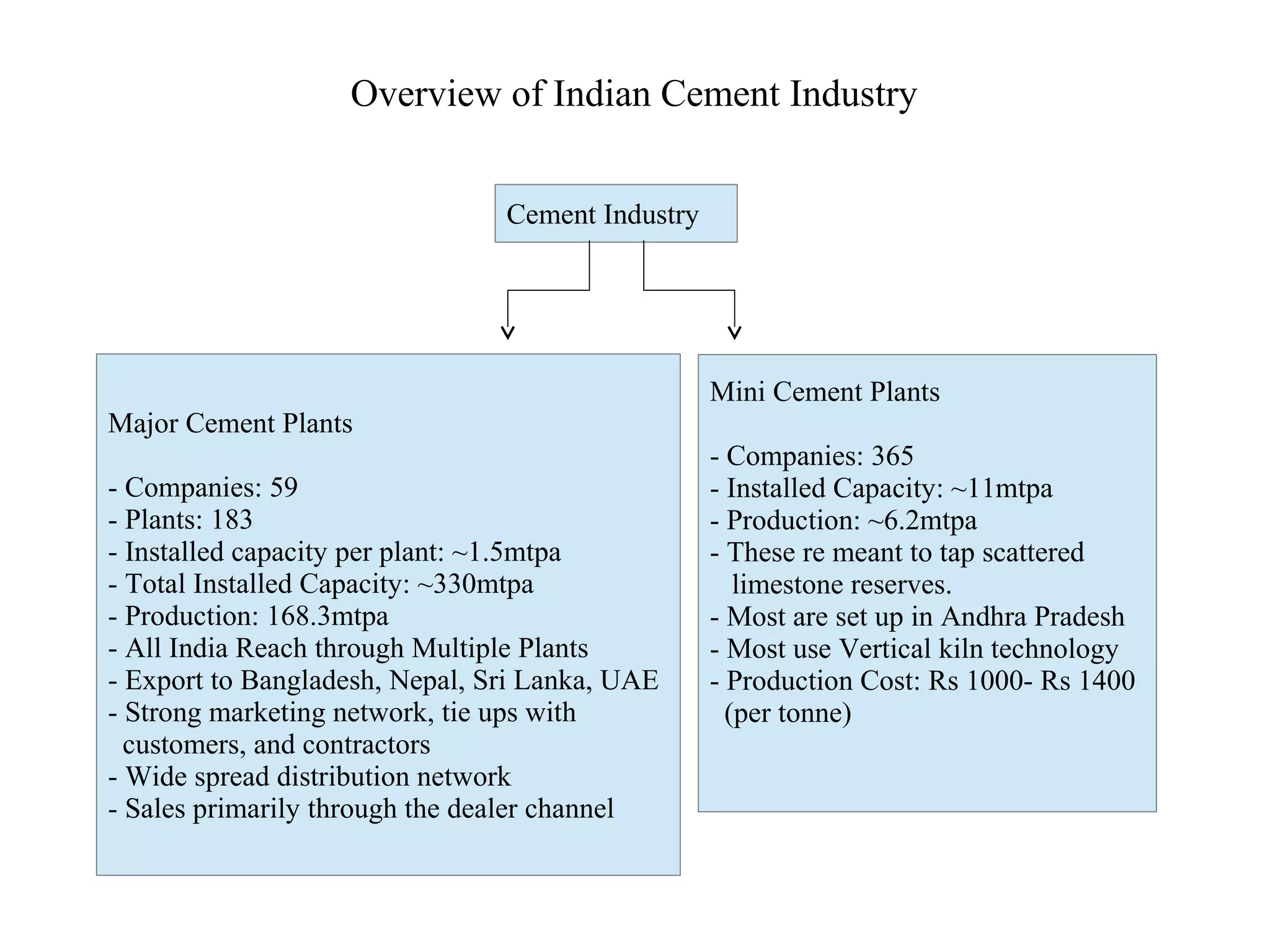

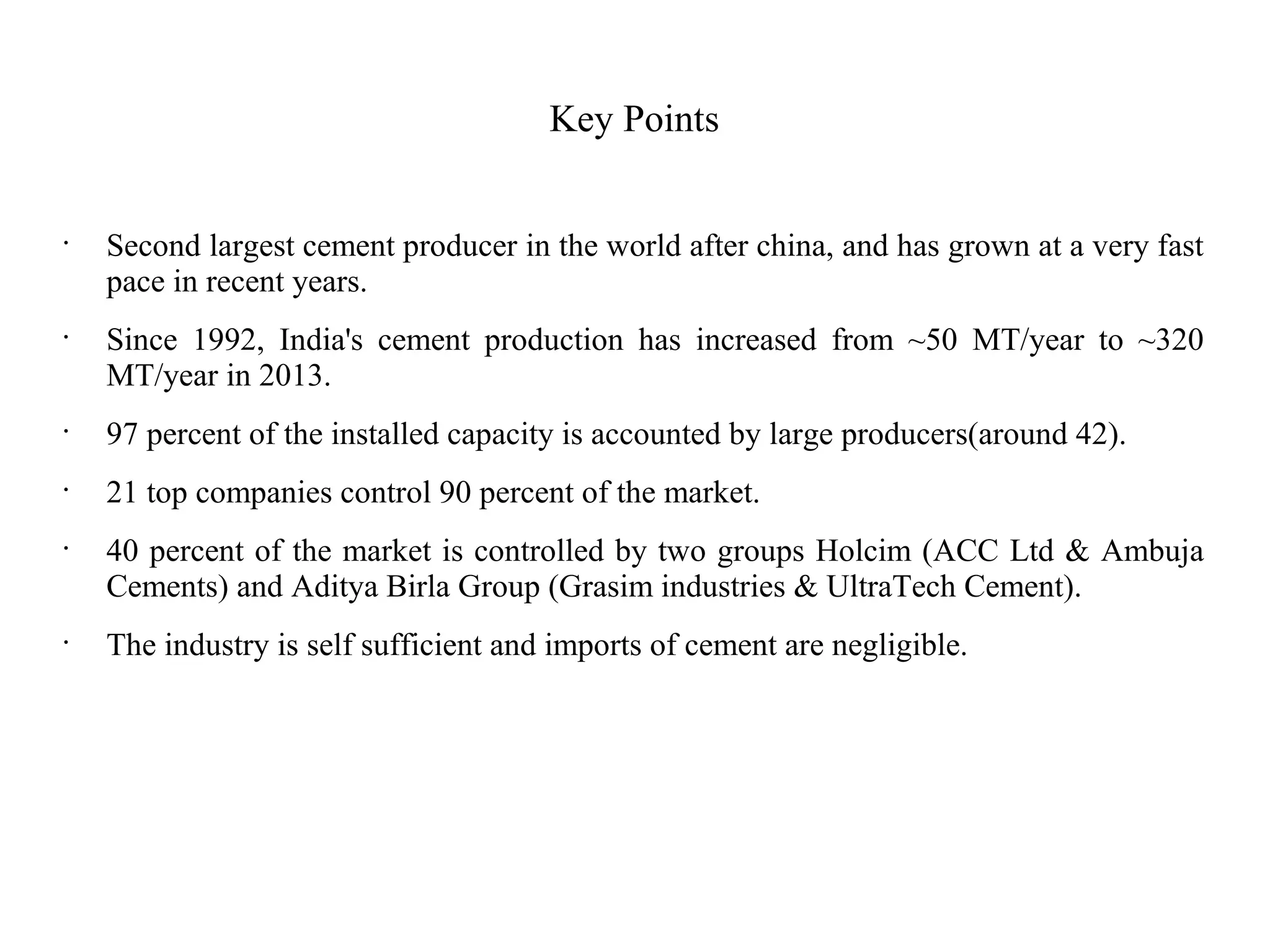

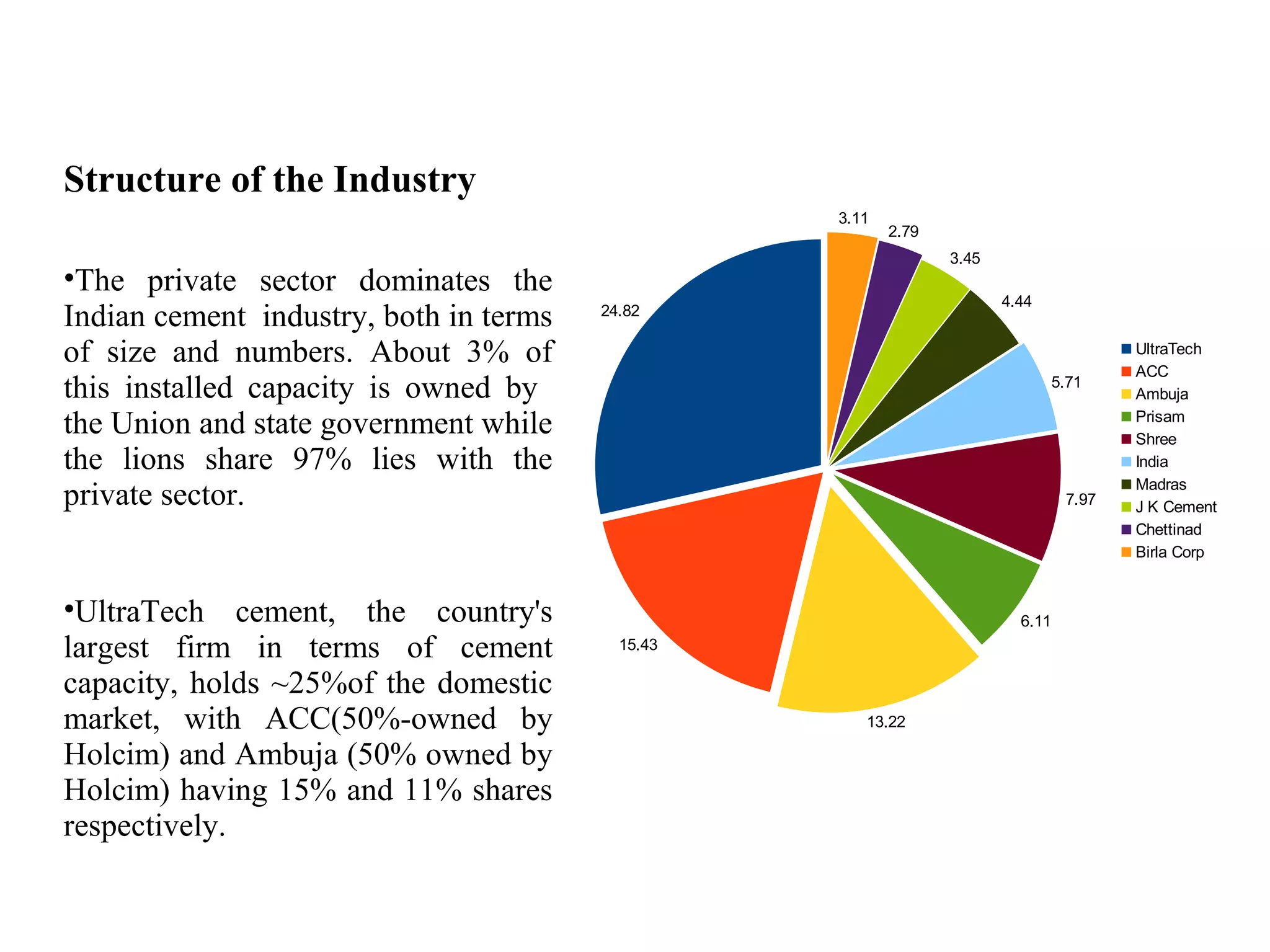

- The Indian cement industry is dominated by large private players and is one of the largest in the world. Production has grown significantly from 50 MT/year in 1992 to over 320 MT/year currently.

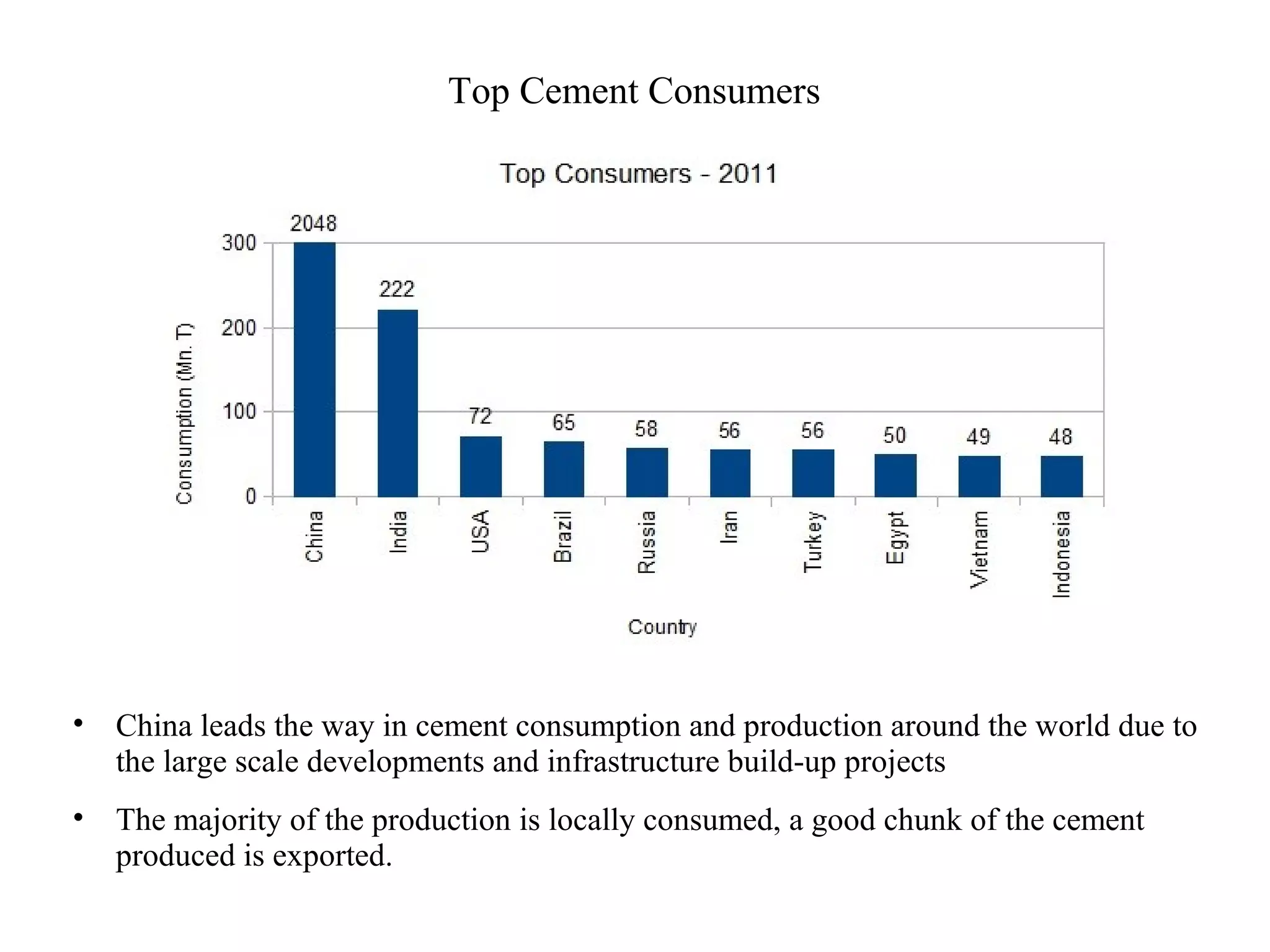

- Demand is driven by infrastructure development, the housing sector, and economic growth. The government plans to invest $1 trillion in infrastructure over the next five years.

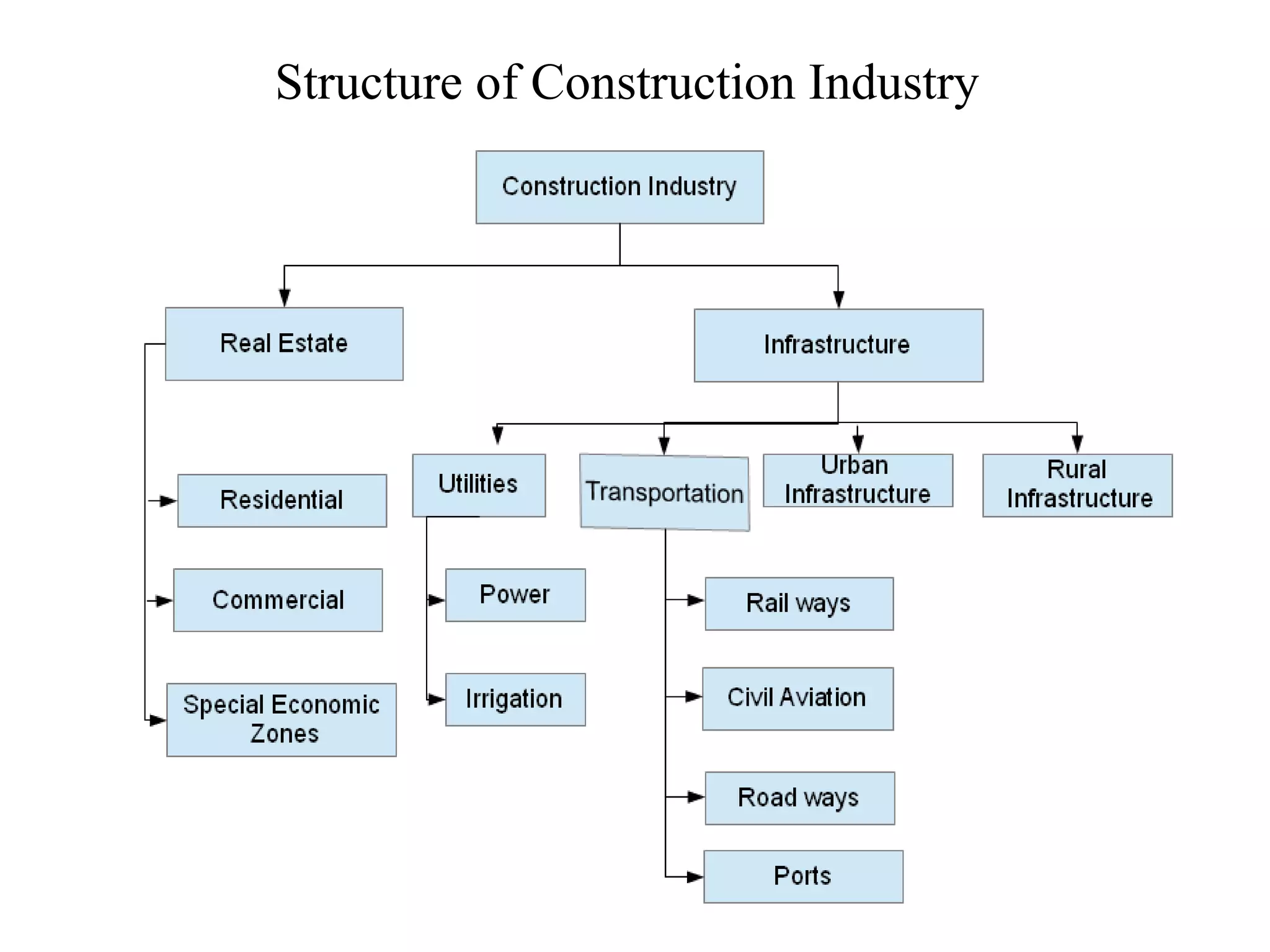

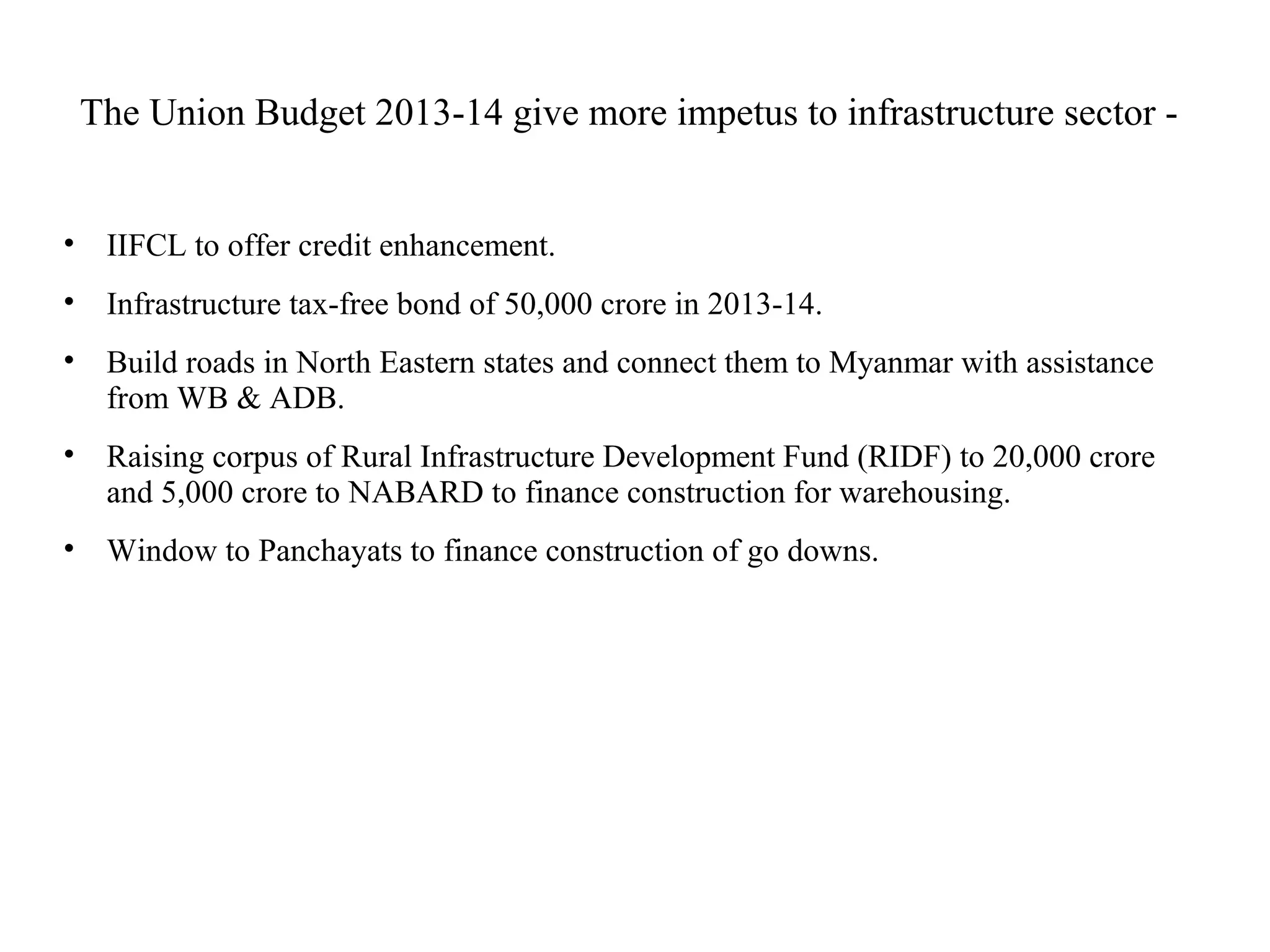

- Major projects underway include roads, ports, airports, railways, and power. The 2013-14 budget also aims to boost infrastructure