Download as PDF, PPTX

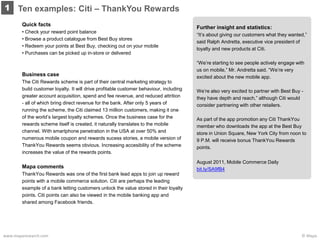

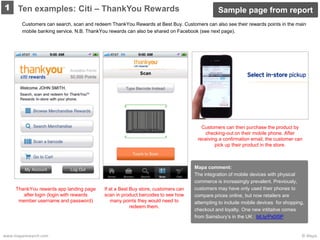

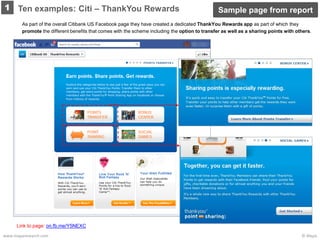

The document is a report from Mapa Research summarizing 10 non-core banking apps and 4 examples from outside financial services. It includes an executive summary highlighting themes like housing/mortgage apps being most common and lack of youth-focused apps. It then outlines the report structure and research approach, which involved analyzing over 80 bank apps from various countries and 40 non-bank apps. One section analyzes the Citi ThankYou Rewards app in detail. The document provides an overview of Mapa Research's services and clients.