Downloaded 17 times

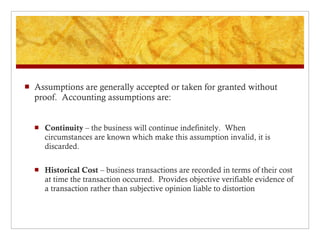

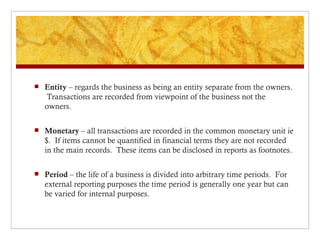

Accounting assumptions provide the foundation for the accounting process and are generally accepted without proof. The key assumptions include: continuity, which assumes a business will continue indefinitely; historical cost, which records transactions based on original cost; the entity assumption, which treats a business as separate from its owners; the monetary assumption, which uses currency to record all transactions; and the period assumption, which divides a business into arbitrary time periods for reporting.