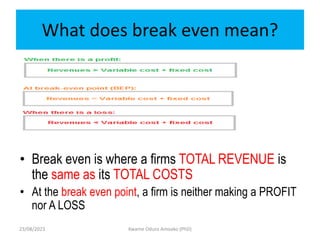

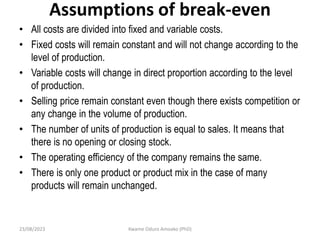

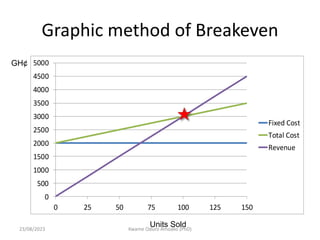

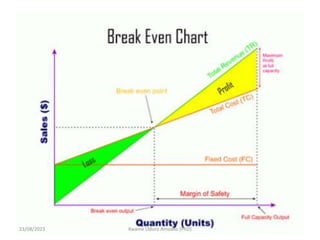

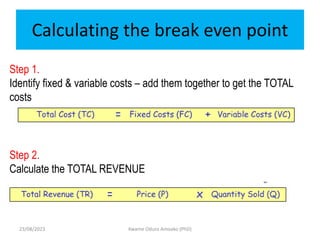

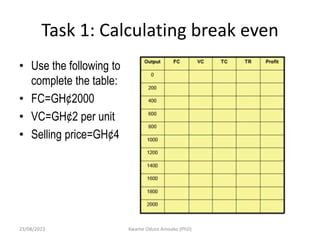

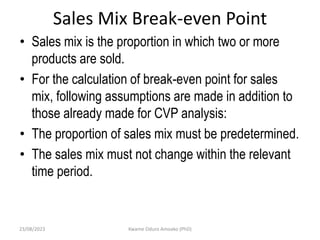

This document provides an overview of cost-volume-profit (CVP) analysis and break-even analysis. It defines break-even as the point where total revenue equals total costs, and neither profit nor loss is made. Break-even analysis determines the sales volume needed for a product or service to cover its costs. The document discusses using break-even analysis to measure profit and losses at different production levels, and to predict the effects of changes in sales price, costs, and efficiency. It also covers the assumptions, uses, and limitations of break-even analysis, as well as different methods for conducting the analysis.