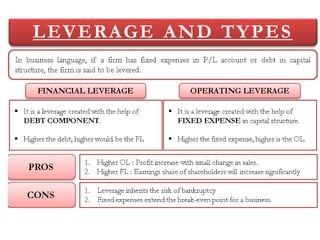

Leverage refers to a firm's use of fixed costs to increase returns to owners. There are two main types of leverage: financial leverage and operating leverage. Financial leverage involves using debt rather than equity to finance assets, which results in fixed interest costs. Operating leverage is using fixed costs in operations that do not vary with production volumes. Combined leverage looks at the relationship between sales variations and taxable income changes, taking into account both financial and operating leverage. Degrees of leverage are calculated to quantify the impact of a sales change on profits.