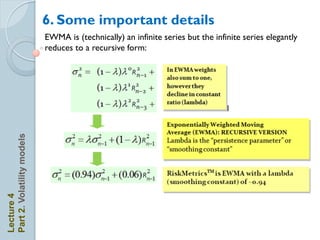

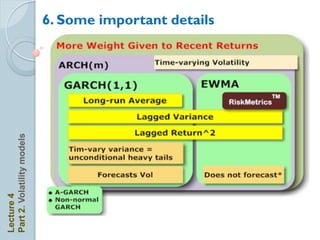

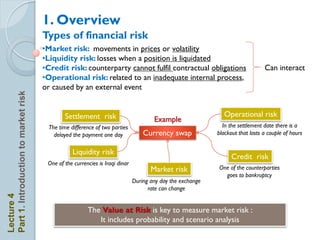

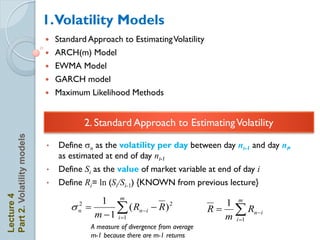

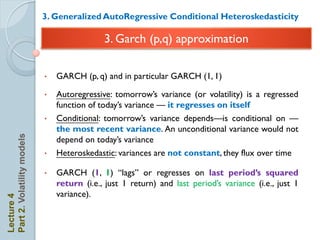

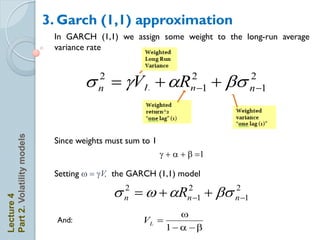

The document summarizes key concepts from Lecture 4, which covered introduction to market risk, modelling volatility, and VaR models. It began with an overview of market risk and risk measurement, including the classification of various financial risks. It then discussed modelling volatility using standard approaches, GARCH models, and exponentially weighted moving average (EWMA) models. The lecture concluded with an introduction to VaR models for measuring market risk.

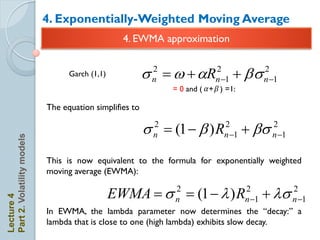

![3. EWMA approach

EWMA s n s n 1 + (1 ) Rn 1

2 2 2

replace s n 1

2

s [s

2

n

2

n2 + (1 ) R 2

n2 ] + (1 ) R 2

n 1

(1 )( R 2

n 1 + R

2

n2 )+ s

2 2

n2

substitute s 2

Part 2. Volatility models

n2

s (1 )( R

2

n

2

n 1 + R 2

n2 + R

2 2

n 3 )+s3 2

n 3

continuing the way gives

Lecture 4

m

s n (1 ) i 1 Rn2i + ms n m

2 2

i 1](https://image.slidesharecdn.com/lecture4-121030062536-phpapp02/85/Lecture-4-17-320.jpg)