This document outlines a lecture on managing financial risk given by Arben Kita. It introduces concepts like mean-variance analysis, the Capital Asset Pricing Model (CAPM), and the Arbitrage Pricing Theory (APT). The lecture aims to analyze credit, market, liquidity, interest rate, and operational risk and how they can be measured and managed. It also discusses using models like CAPM to determine the required rate of return for assets based on their systematic risk (beta).

![Diversification of risk within a portfolio

Example: you can invest in any combination of GM, Intel and Coca-Cola.

What portfolio would you choose?

E[Rp] = (wGM x 1.08) + (wIntel x 1.32) + (wCoca-Cola x 1.75)

Var(Rp) = (wGM x 38.8) + (wIntel x 40.21) + (wCoca-Cola x 94.63) +

(2x wGM x wIntel x 16.13) + (2x wGM x wCoca-Cola x 22.43) +

(2x wIntel x wCoca-Cola x 23.99)

Variance Covariance Matrix

Stock Mean Std dev GM Intel Coca-Cola

GM 1.08 6.23 38.8 16.13 22.43

Intel 1.32 6.34 16.13 40.21 23.99

Coca-Cola 1.75 9.73 22.42 23.99 94.63

Arben Kita, Management of Financial Risk, 2017](https://image.slidesharecdn.com/lecture1-231226062004-e4314b15/75/Lecture-1-Financial-risk-management-lecture-1-11-2048.jpg)

![Now consider the combination (C) of a risky

portfolio (P) and a risk-free asset (with expected

return Rf), with weights w and 1-w, respectively:

)

]

[

(

)

1

(

]

[

]

[

f

P

f

f

P

C

R

R

E

w

R

R

w

R

wE

R

E

−

+

=

−

+

=

f

f R

P

2

R

2

2

P

C w

2w

+

w

+

w

= ,

2

2

)

1

(

)

1

( σ

σ

σ

σ −

−

where subscript Rf refers to the risk-free asset.

Diversifiable (unpriced, idiosyncratic) risk and

undiversifiable (priced, market) risk

and

Arben Kita, Management of Financial Risk, 2017](https://image.slidesharecdn.com/lecture1-231226062004-e4314b15/75/Lecture-1-Financial-risk-management-lecture-1-17-2048.jpg)

![w

=

w

=

P

C

2

P

C

σ

σ

σ

σ

⇒

2

2

w P

C σ

σ /

=

)

]

[

(

]

[ f

P

f

C R

R

E

w

R

R

E −

+

=

Since a risk-free asset has no variance and has zero covariance with

everything else, the formula for the variance collapses to:

Substitution of w into previous return expression

gives

C

P

f

P

f

C

R

R

E

R

R

E σ

σ

)

]

[

(

]

[

−

+

=

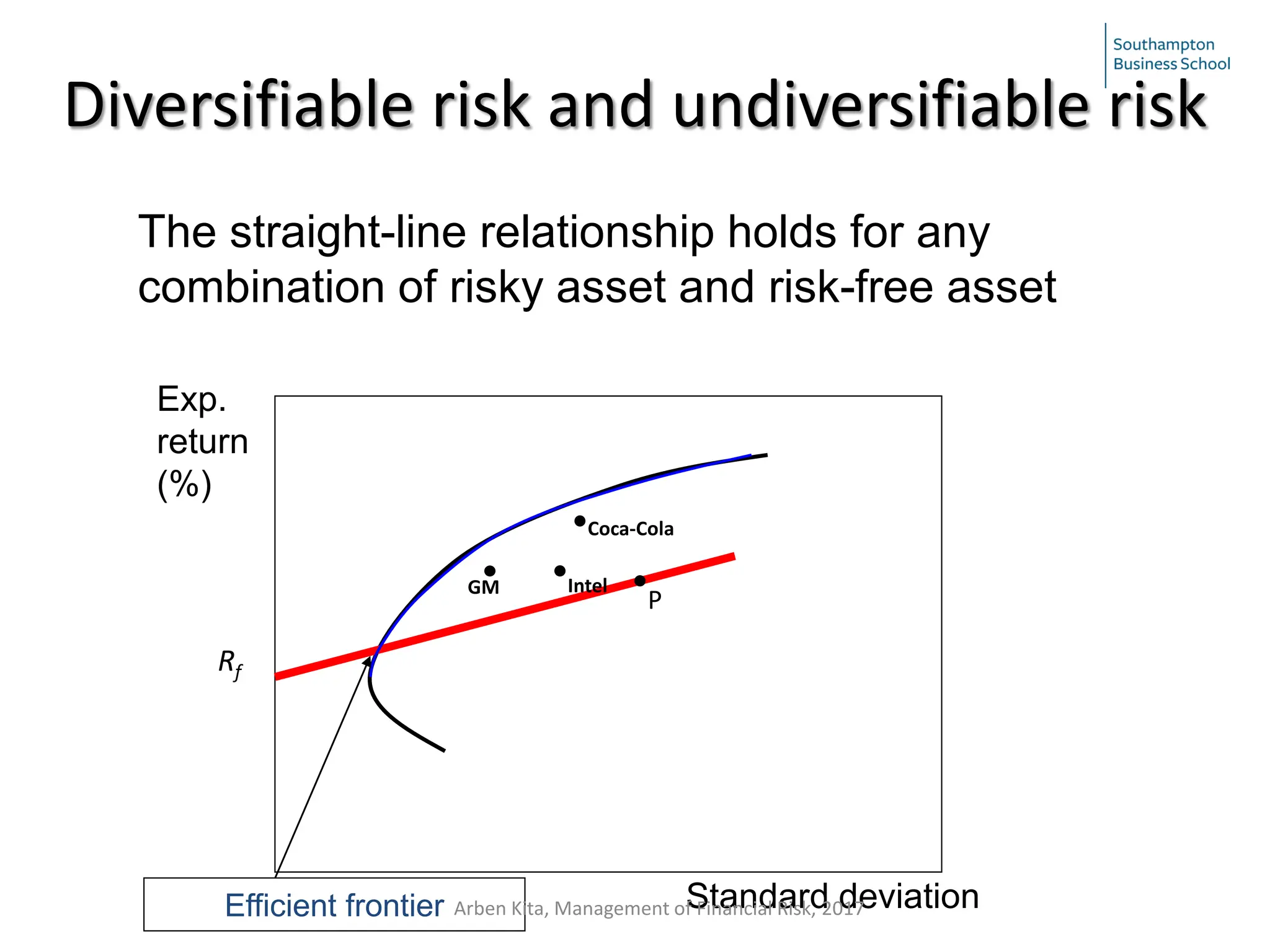

A straight-line relationship Slope

, so .

Diversifiable risk and undiversifiable risk

Arben Kita, Management of Financial Risk, 2017](https://image.slidesharecdn.com/lecture1-231226062004-e4314b15/75/Lecture-1-Financial-risk-management-lecture-1-18-2048.jpg)

![• The tangential portfolio of risky shares that (in

combination with the risk-free asset) gives the

highest rate of the trade-off between the risk and

return

• ‘Market portfolio’ (with expected return E[Rm]).

Diversifiable risk and undiversifiable risk

Arben Kita, Management of Financial Risk, 2017](https://image.slidesharecdn.com/lecture1-231226062004-e4314b15/75/Lecture-1-Financial-risk-management-lecture-1-19-2048.jpg)

![• The straight-line relationship between the risk and

return of the market portfolio and the risk-free asset

is termed the Capital Market Line

• The slope of the Capital Market Line, (E[Rm]-Rf)/σm,

gives the market price of systematic risk (i.e. what

investors need to be offered in order to take on this

risk).

C

m

f

m

f

C

R

R

E

R

R

E σ

σ

)

]

[

(

]

[

−

+

=

Capital Asset Pricing Model (CAPM)

Arben Kita, Management of Financial Risk, 2017](https://image.slidesharecdn.com/lecture1-231226062004-e4314b15/75/Lecture-1-Financial-risk-management-lecture-1-21-2048.jpg)

![Capital Asset Pricing Model (CAPM)

• Sharpe Ratio: a measure of portfolio’s risk-return trade-off,

equal to the portfolio’s risk premium divided by its volatility

• The tangency portfolio has the highest possible Sharpe ratio

of any portfolio

• Aside: Alpha is a measure of a mutual fund’s risk-adjusted

performance. The tangency portfolio also maximises the

fund’s alpha

p

f

p R

R

E

o

SharpeRati

σ

−

=

]

[

Arben Kita, Management of Financial Risk, 2017](https://image.slidesharecdn.com/lecture1-231226062004-e4314b15/75/Lecture-1-Financial-risk-management-lecture-1-23-2048.jpg)

![Implications of the Market Portfolio

• Efficient portfolios are combinations of the market portfolio and riskless asset

• Expected returns of efficient portfolios satisfy:

• This yields the required rate of return or cost of capital for efficient portfolios!

• Trade-off between risk and expected return

• Multiplier is the ratio of portfolio risk to market risk

• What about other (non-efficient) portfolios?

Capital Asset Pricing Model (CAPM)

[ ] [ ]

( )

f

p

m

p

f

p R

R

E

R

R

E −

+

=

σ

σ

Arben Kita, Management of Financial Risk, 2017](https://image.slidesharecdn.com/lecture1-231226062004-e4314b15/75/Lecture-1-Financial-risk-management-lecture-1-24-2048.jpg)

![• Expressing the market-related (undiversifiable) risk in terms of standard

deviation

where ρjm is the correlation between returns of j and m,

• multiplying this by the market price of undiversifiable risk,

• and adding the result to the risk-free rate, gives the following expression

for the required return on share j:

jm

j

j

DIV

NON = ρ

σ

σ )

(

−

m

f

m R

R

E σ

/

)

]

[

( −

jm

j

m

f

m

f

j

R

R

E

R

R

E ρ

σ

σ

)

]

[

(

]

[

−

+

=

Capital Asset Pricing Model (CAPM)

Arben Kita, Management of Financial Risk, 2017](https://image.slidesharecdn.com/lecture1-231226062004-e4314b15/75/Lecture-1-Financial-risk-management-lecture-1-26-2048.jpg)

![j

m

jm

m

jm

m

j

m

jm

j

β

σ

σ

σ

ρ

σ

σ

σ

ρ

σ

=

=

= 2

2

j

f

m

f

j R

R

E

R

R

E β

)

]

[

(

]

[ −

+

=

Covariance (j,m)

Variance (m)

This ratio is termed beta

The Capital Asset Pricing Model

Capital Asset Pricing Model (CAPM)

jm

j

m

f

m

f

j

R

R

E

R

R

E ρ

σ

σ

)

]

[

(

]

[

−

+

=

Arben Kita, Management of Financial Risk, 2017](https://image.slidesharecdn.com/lecture1-231226062004-e4314b15/75/Lecture-1-Financial-risk-management-lecture-1-27-2048.jpg)

![Graphical representation of CAPM: Security

Market Line

Risk-free return =

Beta of market portfolio = 1.0

Exp. Return

Beta

.

Rf

‘Market portfolio’

1.0

Rm

Market return =

‘Security Market

Line’

m

jm

j

σ

ρ

σ

Systematic risk

j

f

m

f

j R

R

E

R

R

E β

)

]

[

(

]

[ −

+

=

Arben Kita, Management of Financial Risk, 2017](https://image.slidesharecdn.com/lecture1-231226062004-e4314b15/75/Lecture-1-Financial-risk-management-lecture-1-29-2048.jpg)

![Capital Asset Pricing Model (CAPM):

SML

• E[Ri] = Rf + βi(E[Rm] - Rf)

• Implications:

• βi = 1 => E[Ri] = E[Rm]

• βi = 0 => E[Ri] = E[Rf]

• βi < 0 => E[Ri] < E[Rf] (Why?)

Security Market Line

Arben Kita, Management of Financial Risk, 2017](https://image.slidesharecdn.com/lecture1-231226062004-e4314b15/75/Lecture-1-Financial-risk-management-lecture-1-30-2048.jpg)